Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:INDB

Independent Bank (INDB): Revisiting Valuation After Recent Share Price Dip

Simply Wall St

Reviewed by Kshitija Bhandaru

Independent Bank (INDB) shares have moved a bit lower this week, dipping around 2% over the past week and 3% in the past month. Investors are keeping an eye on trading activity, looking for fresh signals that might clarify the current trend.

See our latest analysis for Independent Bank.

Independent Bank’s share price performance has been fairly subdued when viewed over the past year, with the 1-year total shareholder return at just 0.25%. Despite a modest edge in the 90-day share price return, any recent momentum seems patchy, and the stock remains sensitive to shifts in sentiment and the broader economic outlook.

If you’re testing the waters beyond banks, this could be the perfect moment to discover fast growing stocks with high insider ownership.

But with a solid recent earnings performance and the stock still trading below analyst price targets, the big question remains: is Independent Bank undervalued, or has the market already priced in the company’s future growth?

Most Popular Narrative: 13% Undervalued

Independent Bank's most followed narrative suggests there's meaningful upside from the current price of $68.89, as the fair value calculation implies a higher target. Analysts are weighing recent growth catalysts and business expansion, making this narrative especially relevant at today's levels.

Ongoing U.S. population migration to secondary and smaller metropolitan areas, alongside strong small business formation in core markets, positions Independent Bank to benefit from outsized loan and deposit growth from community banking and small business lending, positively impacting long-term revenue and fee income.

What’s at the heart of this valuation? Bold assumptions about expansion outside major metros and a new growth formula for loan and deposit volumes. Wondering how these ambitious projections translate into real value? The surprising combination of market shifts and banking tech investments could be a game changer. Discover the numbers fueling this fair value call.

Result: Fair Value of $79.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent commercial real estate exposure and uncertainty in integrating recent acquisitions could still challenge Independent Bank's path to sustained profit growth.

Find out about the key risks to this Independent Bank narrative.

Another View: What Do the Price Ratios Say?

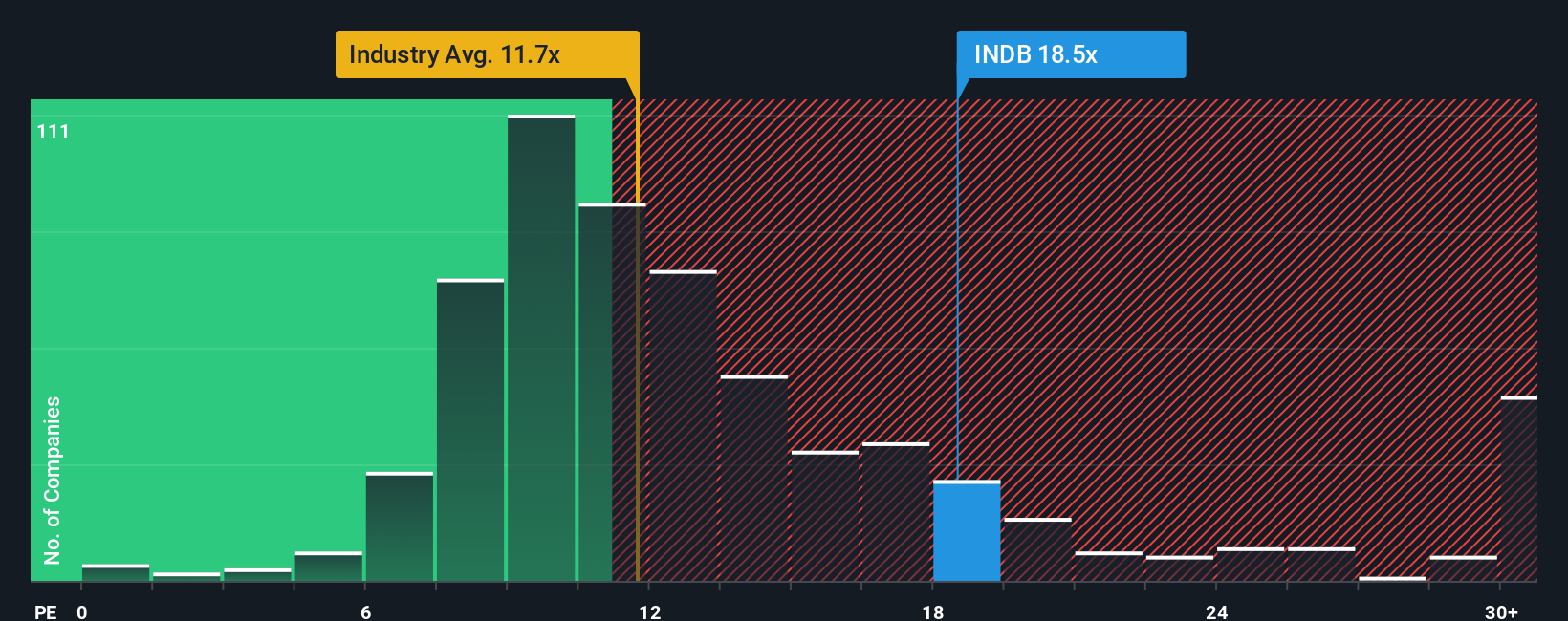

Looking at Independent Bank through the lens of its price-to-earnings ratio, the valuation picture changes. While its P/E stands at 18.2x, higher than the US Banks industry average of 11.8x, it is more attractive compared to peers at 20.6x and below the fair ratio of 21.6x. This means the market is pricing in some growth but leaves room for debate about just how much is already reflected in the price. Does this smaller gap signal opportunity, or a risk if expectations shift?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Independent Bank Narrative

If you'd rather draw your own conclusions or test out different scenarios, it's quick and easy to craft a personal take in just a few minutes. Do it your way.

A great starting point for your Independent Bank research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Moves?

Capitalize on the latest market trends and sharpen your investment strategy. Don’t miss the chance to find stocks that match your unique financial goals.

- Unlock potential income streams by tracking these 19 dividend stocks with yields > 3%, which offer strong yields and reliable payout histories for steady growth in your portfolio.

- Tap into breakthrough innovation with these 24 AI penny stocks, driving real-world applications in automation, data analytics, and artificial intelligence solutions.

- Seize opportunities others overlook by screening these 3568 penny stocks with strong financials, positioned for rapid growth and strong fundamentals amid evolving markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:INDB

Independent Bank

Operates as the bank holding company for Rockland Trust Company that provides commercial banking products and services to individuals and small-to-medium sized businesses in the United States.

Flawless balance sheet with high growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor