Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:HWC

Hancock Whitney (NASDAQ:HWC) Will Pay A Larger Dividend Than Last Year At $0.30

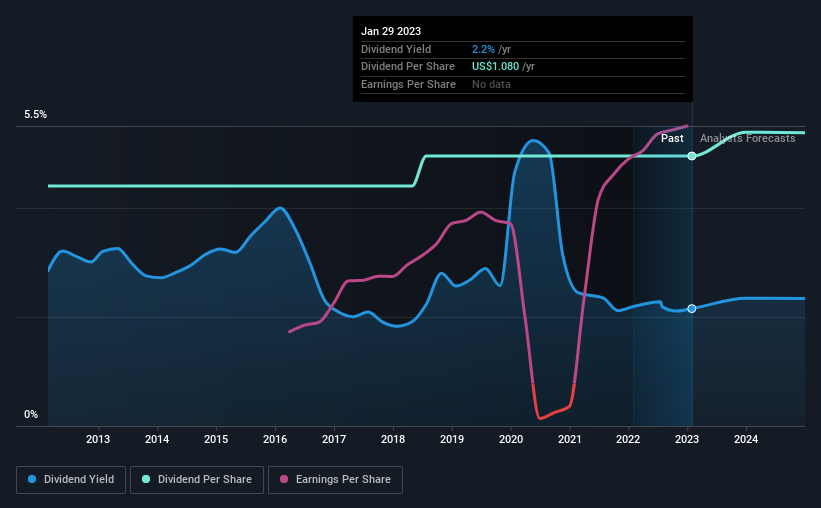

The board of Hancock Whitney Corporation (NASDAQ:HWC) has announced that the dividend on 15th of March will be increased to $0.30, which will be 11% higher than last year's payment of $0.27 which covered the same period. Despite this raise, the dividend yield of 2.2% is only a modest boost to shareholder returns.

See our latest analysis for Hancock Whitney

Hancock Whitney's Earnings Will Easily Cover The Distributions

Even a low dividend yield can be attractive if it is sustained for years on end.

Hancock Whitney has a long history of paying out dividends, with its current track record at a minimum of 10 years. Using data from its latest earnings report, Hancock Whitney's payout ratio sits at 18%, an extremely comfortable number that shows that it can pay its dividend.

Looking forward, EPS is forecast to rise by 0.9% over the next 3 years. Analysts estimate the future payout ratio will be 19% over the same time period, which is in the range that makes us comfortable with the sustainability of the dividend.

Hancock Whitney Has A Solid Track Record

The company has an extended history of paying stable dividends. The dividend has gone from an annual total of $0.96 in 2013 to the most recent total annual payment of $1.08. This implies that the company grew its distributions at a yearly rate of about 1.2% over that duration. While the consistency in the dividend payments is impressive, we think the relatively slow rate of growth is less attractive.

The Dividend Looks Likely To Grow

The company's investors will be pleased to have been receiving dividend income for some time. Hancock Whitney has seen EPS rising for the last five years, at 19% per annum. Hancock Whitney definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

We Really Like Hancock Whitney's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Earnings are easily covering distributions, and the company is generating plenty of cash. All of these factors considered, we think this has solid potential as a dividend stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 1 warning sign for Hancock Whitney that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Hancock Whitney might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:HWC

Hancock Whitney

Operates as the financial holding company for Hancock Whitney Bank that provides traditional and online banking services to commercial, small business, and retail customers in the United States.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor