Advertisement

The board of Heritage Commerce Corp (NASDAQ:HTBK) has announced that it will pay a dividend of $0.13 per share on the 25th of August. Based on this payment, the dividend yield on the company's stock will be 4.4%, which is an attractive boost to shareholder returns.

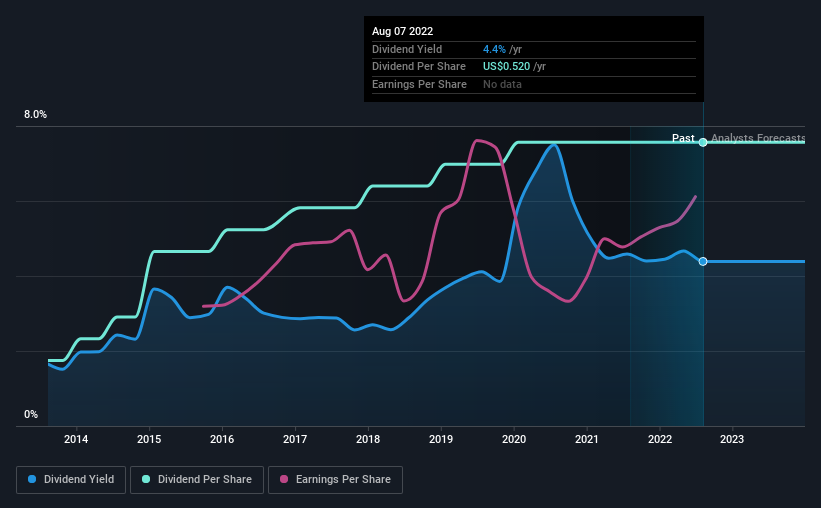

View our latest analysis for Heritage Commerce

Heritage Commerce's Dividend Forecasted To Be Well Covered By Earnings

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained.

Having paid out dividends for 9 years, Heritage Commerce has a good history of paying out a part of its earnings to shareholders. Based on Heritage Commerce's last earnings report, the payout ratio is at a decent 57%, meaning that the company is able to pay out its dividend with a bit of room to spare.

Looking forward, earnings per share is forecast to rise by 56.9% over the next year. If the dividend continues along recent trends, we estimate the future payout ratio will be 39%, which is in the range that makes us comfortable with the sustainability of the dividend.

Heritage Commerce Is Still Building Its Track Record

Even though the company has been paying a consistent dividend for a while, we would like to see a few more years before we feel comfortable relying on it. Since 2013, the annual payment back then was $0.12, compared to the most recent full-year payment of $0.52. This implies that the company grew its distributions at a yearly rate of about 18% over that duration. Heritage Commerce has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

The Dividend's Growth Prospects Are Limited

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Earnings have grown at around 4.4% a year for the past five years, which isn't massive but still better than seeing them shrink. Heritage Commerce is struggling to find viable investments, so it is returning more to shareholders. This isn't necessarily bad, but we wouldn't expect rapid dividend growth in the future.

In Summary

Overall, we think Heritage Commerce is a solid choice as a dividend stock, even though the dividend wasn't raised this year. The payout ratio looks good, but unfortunately the company's dividend track record isn't stellar. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 2 warning signs for Heritage Commerce that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Heritage Commerce might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:HTBK

Heritage Commerce

Operates as the bank holding company for Heritage Bank of Commerce that provides various commercial and personal banking services to residents and the business/professional community in California.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor