- United States

- /

- Banks

- /

- NasdaqCM:FNCB

Is Now The Time To Put FNCB Bancorp (NASDAQ:FNCB) On Your Watchlist?

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like FNCB Bancorp (NASDAQ:FNCB). Even if the shares are fully valued today, most capitalists would recognize its profits as the demonstration of steady value generation. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

View our latest analysis for FNCB Bancorp

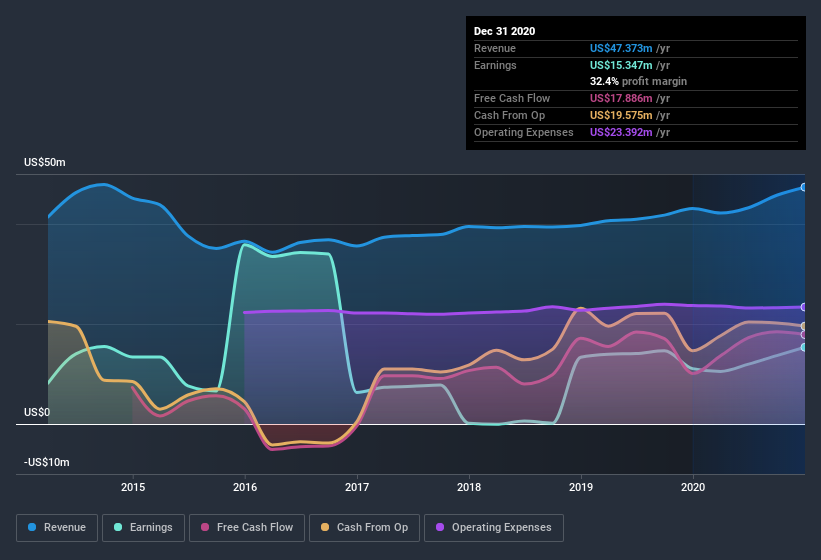

FNCB Bancorp's Improving Profits

In the last three years FNCB Bancorp's earnings per share took off like a rocket; fast, and from a low base. So the actual rate of growth doesn't tell us much. As a result, I'll zoom in on growth over the last year, instead. Like a wedge-tailed eagle on the wind, FNCB Bancorp's EPS soared from US$0.56 to US$0.76, in just one year. That's a commendable gain of 36%.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. I note that FNCB Bancorp's revenue from operations was lower than its revenue in the last twelve months, so that could distort my analysis of its margins. FNCB Bancorp maintained stable EBIT margins over the last year, all while growing revenue 10.0% to US$47m. That's a real positive.

In the chart below, you can see how the company has grown earnings, and revenue, over time. To see the actual numbers, click on the chart.

Since FNCB Bancorp is no giant, with a market capitalization of US$155m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are FNCB Bancorp Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Insiders both bought and sold FNCB Bancorp shares in the last year, but the good news is they spent US$32k more buying than they netted selling. When you weigh that up, it is a mild positive, indicating increased alignment between shareholders and management. We also note that it was the Independent Director, Vithalbhai Dhaduk, who made the biggest single acquisition, paying US$37k for shares at about US$5.50 each.

Along with the insider buying, another encouraging sign for FNCB Bancorp is that insiders, as a group, have a considerable shareholding. Indeed, they hold US$27m worth of its stock. That's a lot of money, and no small incentive to work hard. Those holdings account for over 17% of the company; visible skin in the game.

While insiders are apparently happy to hold and accumulate shares, that is just part of the pretty picture. The cherry on top is that the CEO, Jerry Champi is paid comparatively modestly to CEOs at similar sized companies. I discovered that the median total compensation for the CEOs of companies like FNCB Bancorp with market caps between US$100m and US$400m is about US$935k.

FNCB Bancorp offered total compensation worth US$657k to its CEO in the year to . That seems pretty reasonable, especially given its below the median for similar sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when its reasonable that does give me a little more confidence that leadership are looking out for shareholder interests. I'd also argue reasonable pay levels attest to good decision making more generally.

Should You Add FNCB Bancorp To Your Watchlist?

You can't deny that FNCB Bancorp has grown its earnings per share at a very impressive rate. That's attractive. On top of that, insiders own a significant stake in the company and have been buying more shares. So I do think this is one stock worth watching. You should always think about risks though. Case in point, we've spotted 2 warning signs for FNCB Bancorp you should be aware of, and 1 of them shouldn't be ignored.

As a growth investor I do like to see insider buying. But FNCB Bancorp isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you decide to trade FNCB Bancorp, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:FNCB

FNCB Bancorp

Operates as the bank holding company for FNCB Bank that provides retail and commercial banking services to individuals, businesses, local governments, and municipalities in the United States.

Flawless balance sheet and good value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion