East West Bancorp (EWBC) has caught investors’ attention following its latest investor update, where the bank showcased strong financial results for the second quarter of 2025. Growth was propelled by both commercial and residential mortgage loans, and the company emphasized a 2% rise in average loans and deposits from the prior quarter. This consistent execution on its core strategies, especially around diversification and deposit management, has kept East West Bancorp at the forefront of the industry and secured recognition as a top performer for three years in a row.

Over the past year, East West Bancorp’s stock has delivered a 38% return, which stands well above what many regional lenders have achieved in recent periods. The momentum has been building this year as well, with an impressive 14% year-to-date gain and a 13% increase in the past three months. While recent quarters have seen solid revenue and net income growth, the company’s approach to balancing risk and opportunity remains a major talking point.

All this naturally raises the big question: after such a strong run, is East West Bancorp’s current share price reflecting all of its growth potential or is there still an opportunity for investors who believe the story is far from over?

Advertisement

Most Popular Narrative: 9.4% Undervalued

The most widely followed narrative views East West Bancorp as undervalued by nearly 10%, largely driven by sustained growth expectations and a robust strategic direction.

Sustained investments in digital banking, automation, and technology in areas such as mobile, cybersecurity, and operational efficiency allow for scalable growth and improve the efficiency ratio. This supports higher net margins and long-term cost containment.

Want to know the playbook that is powering this optimistic view? The narrative hints at bold growth assumptions and a profit outlook that implies big upside potential. What key financial forecasts are putting this premium price tag within reach? If you are curious about the specifics behind these projections and what it all could mean for future returns, keep reading for a closer look at what underpins this bullish consensus.

However, heightened commercial real estate exposure and rising compliance costs could dampen East West Bancorp’s growth and challenge the market’s optimistic outlook.

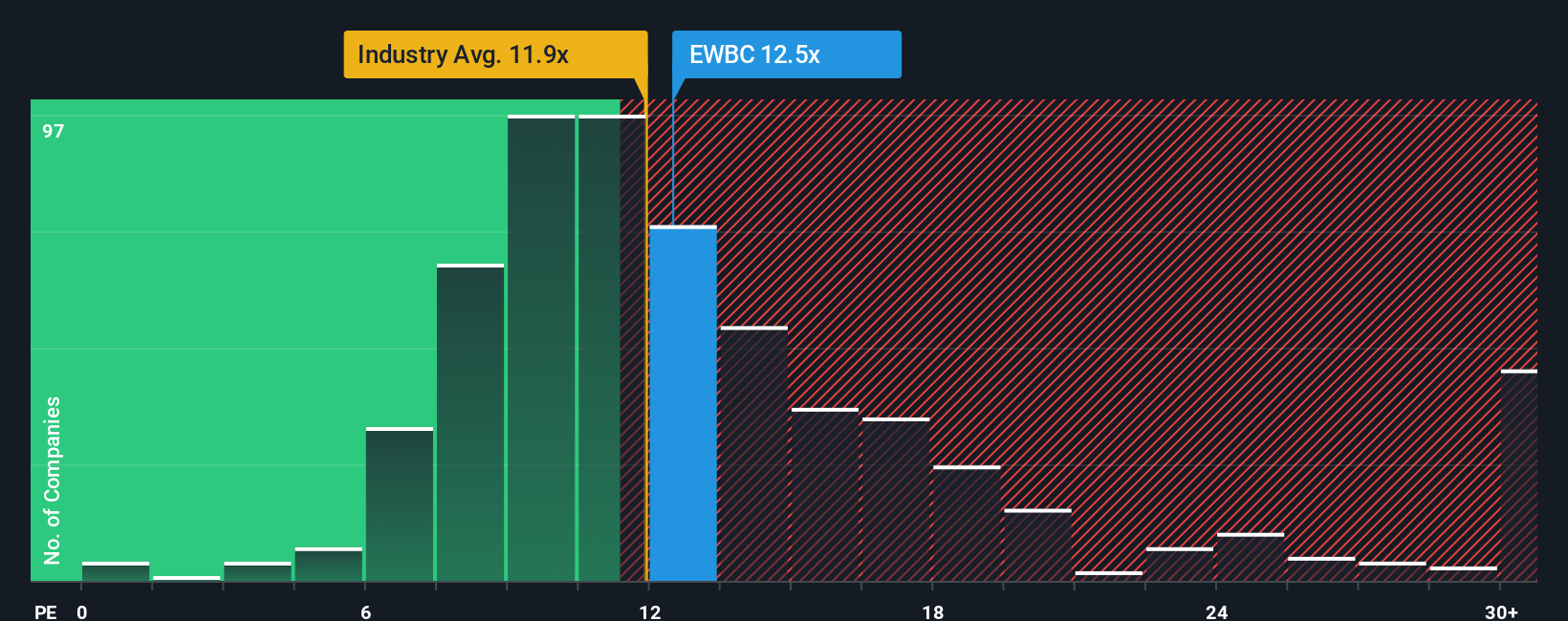

Looking from a different angle, East West Bancorp is actually trading at a higher price compared to the industry’s typical price-to-earnings ratio. Could this mean the share price has raced ahead of fundamentals, or is there a premium for quality here?

If you see things differently or want to draw your own conclusions, you can easily build your own perspective in just a few minutes. Do it your way.

A great starting point for your East West Bancorp research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Why stop with just one opportunity? Give yourself the edge by using the Simply Wall Street Screener to find powerful new stocks and themes that match your investing goals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if East West Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

Operates as the bank holding company for East West Bank that provides a range of personal and commercial banking services to businesses and individuals in the United States.