- United States

- /

- Banks

- /

- NasdaqCM:EMCF

Don't Buy Emclaire Financial Corp (NASDAQ:EMCF) For Its Next Dividend Without Doing These Checks

Readers hoping to buy Emclaire Financial Corp (NASDAQ:EMCF) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. This means that investors who purchase shares on or after the 30th of November will not receive the dividend, which will be paid on the 18th of December.

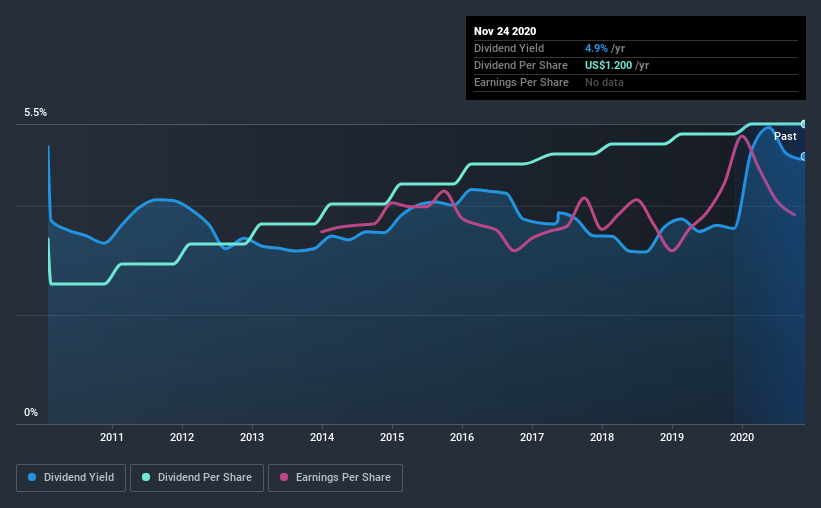

Emclaire Financial's next dividend payment will be US$0.30 per share, and in the last 12 months, the company paid a total of US$1.20 per share. Based on the last year's worth of payments, Emclaire Financial stock has a trailing yield of around 4.9% on the current share price of $24.45. If you buy this business for its dividend, you should have an idea of whether Emclaire Financial's dividend is reliable and sustainable. So we need to investigate whether Emclaire Financial can afford its dividend, and if the dividend could grow.

See our latest analysis for Emclaire Financial

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Emclaire Financial paid out 57% of its earnings to investors last year, a normal payout level for most businesses.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

Click here to see how much of its profit Emclaire Financial paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks with flat earnings can still be attractive dividend payers, but it is important to be more conservative with your approach and demand a greater margin for safety when it comes to dividend sustainability. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. That explains why we're not overly excited about Emclaire Financial's flat earnings over the past five years. It's better than seeing them drop, certainly, but over the long term, all of the best dividend stocks are able to meaningfully grow their earnings per share.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the last 10 years, Emclaire Financial has lifted its dividend by approximately 5.0% a year on average.

To Sum It Up

From a dividend perspective, should investors buy or avoid Emclaire Financial? Emclaire Financial's earnings per share have been essentially flat, and the company is paying out more than half of its earnings as dividends to shareholders. Emclaire Financial doesn't appear to have a lot going for it, and we're not inclined to take a risk on owning it for the dividend.

Although, if you're still interested in Emclaire Financial and want to know more, you'll find it very useful to know what risks this stock faces. Case in point: We've spotted 1 warning sign for Emclaire Financial you should be aware of.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Emclaire Financial, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Emclaire Financial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqCM:EMCF

Emclaire Financial

Emclaire Financial Corp operates as the bank holding company for The Farmers National Bank of Emlenton that provides retail and commercial financial products and services to individuals and businesses in western Pennsylvania.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives