Advertisement

- United States

- /

- Banks

- /

- NasdaqGM:EBMT

Should You Buy Eagle Bancorp Montana, Inc. (NASDAQ:EBMT) For Its Upcoming Dividend?

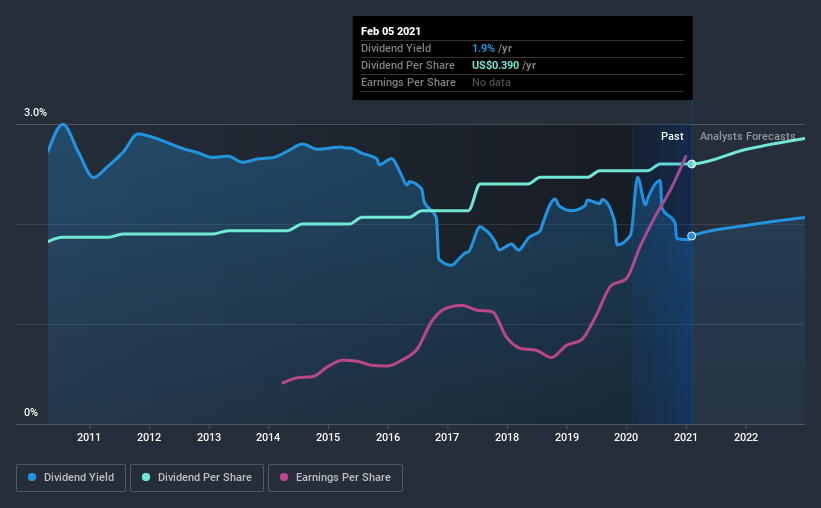

It looks like Eagle Bancorp Montana, Inc. (NASDAQ:EBMT) is about to go ex-dividend in the next 4 days. Ex-dividend means that investors that purchase the stock on or after the 11th of February will not receive this dividend, which will be paid on the 5th of March.

Eagle Bancorp Montana's next dividend payment will be US$0.098 per share, and in the last 12 months, the company paid a total of US$0.39 per share. Last year's total dividend payments show that Eagle Bancorp Montana has a trailing yield of 1.9% on the current share price of $20.74. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

View our latest analysis for Eagle Bancorp Montana

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Eagle Bancorp Montana has a low and conservative payout ratio of just 12% of its income after tax.

Companies that pay out less in dividends than they earn in profits generally have more sustainable dividends. The lower the payout ratio, the more wiggle room the business has before it could be forced to cut the dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. That's why it's comforting to see Eagle Bancorp Montana's earnings have been skyrocketing, up 36% per annum for the past five years.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Since the start of our data, 10 years ago, Eagle Bancorp Montana has lifted its dividend by approximately 3.6% a year on average. Earnings per share have been growing much quicker than dividends, potentially because Eagle Bancorp Montana is keeping back more of its profits to grow the business.

To Sum It Up

Should investors buy Eagle Bancorp Montana for the upcoming dividend? Typically, companies that are growing rapidly and paying out a low fraction of earnings are keeping the profits for reinvestment in the business. This strategy can add significant value to shareholders over the long term - as long as it's done without issuing too many new shares. In summary, Eagle Bancorp Montana appears to have some promise as a dividend stock, and we'd suggest taking a closer look at it.

So while Eagle Bancorp Montana looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. To that end, you should learn about the 3 warning signs we've spotted with Eagle Bancorp Montana (including 1 which doesn't sit too well with us).

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Eagle Bancorp Montana, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eagle Bancorp Montana might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:EBMT

Eagle Bancorp Montana

Operates as the bank holding company for Opportunity Bank of Montana that provides various retail banking products and services to small businesses and individuals in Montana.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor