- United States

- /

- Banks

- /

- NasdaqGM:AMAL

Amalgamated Financial (AMAL) Net Margins Hold Steady, Underscoring Quality Narrative

Reviewed by Simply Wall St

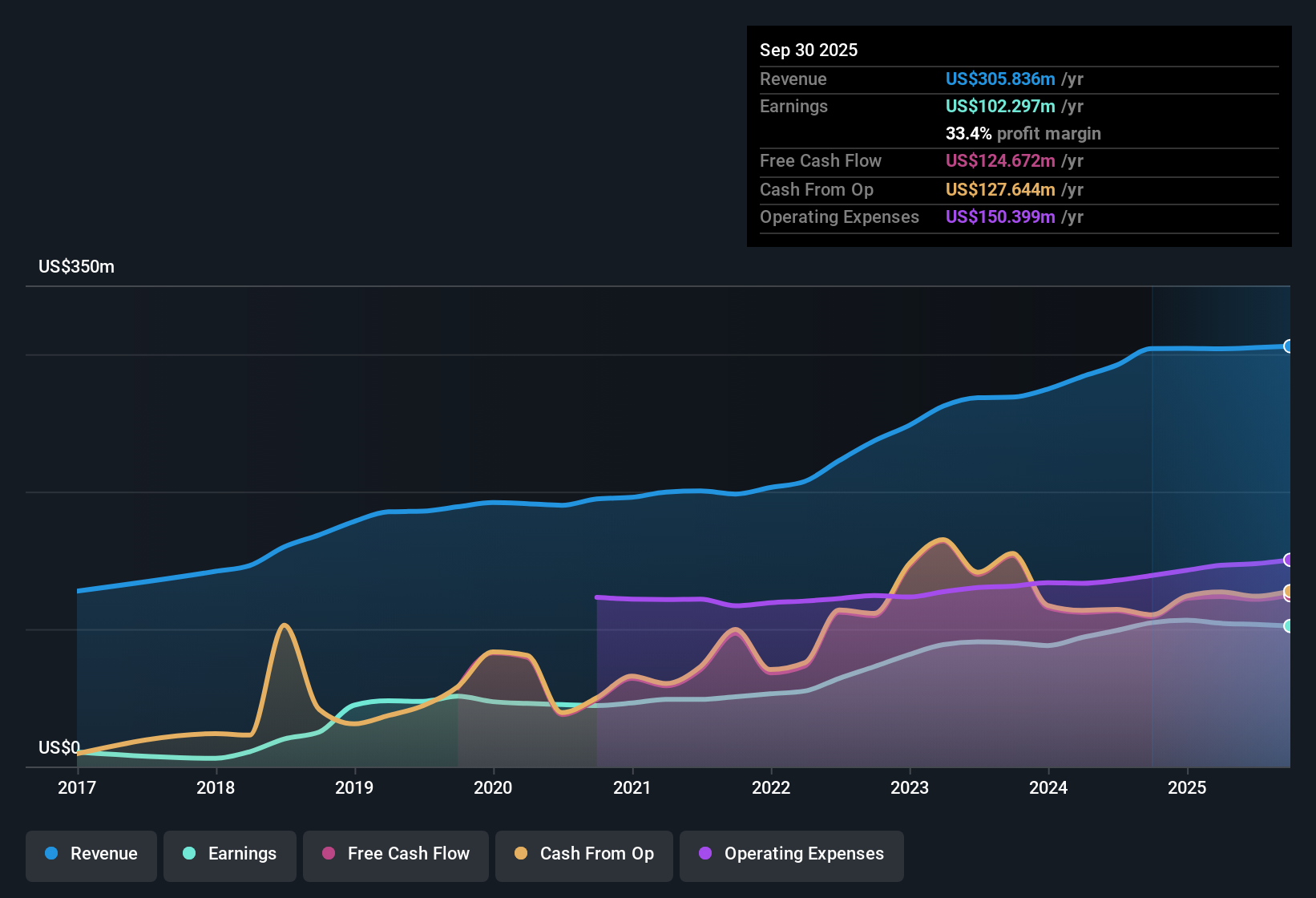

Amalgamated Financial (AMAL) reported net profit margins of 33.9%, in line with last year. Over the past five years, the company’s earnings have grown 19.7% per year; however, growth in the past year slowed to 4.5%. Shares currently trade at a Price-to-Earnings ratio of 8x, which is well below the US Banks industry average of 11.3x and the peer average of 10.2x. The share price also remains below an estimated fair value of $65.49. The combination of strong multi-year profit growth, resilient margins, and below-average valuation multiples may give investors reason to look at the latest results constructively.

See our full analysis for Amalgamated Financial.Next, we will see how these headline numbers measure up against the narratives investors are following on Simply Wall St, and where the real surprises might emerge.

See what the community is saying about Amalgamated Financial

Digital Modernization Lifts Efficiency Metrics

- Analysts expect Amalgamated Financial’s profit margins to grow from 33.9% today to 34.8% within three years, highlighting optimism around operational upgrades and streamlined digital platforms.

- Analysts' consensus view is that the rollout of an integrated digital monetization platform, along with expanded digital banking capabilities, will boost operational efficiency and accelerate cross-sell opportunities for the bank’s clients.

- Consensus expects these changes to improve future net margin and earnings growth, given the focus on automation and customer acquisition through technology.

- Analysts point to scalable infrastructure investments as the backbone for supporting growth and improving the efficiency ratio, especially as the bank expands into high-potential markets.

- What is especially notable is the emphasis on digital transformation as a driver of both efficiency and revenue stability, rather than just keeping up with industry norms.

To discover how digital strategies are shaping the bank's growth narrative and whether these investments are enough to stay ahead, read the full consensus view for Amalgamated Financial. 📊 Read the full Amalgamated Financial Consensus Narrative.

Balance Sheet Growth Faces Sector Headwinds

- The company’s growing exposure to commercial real estate (CRE) and multifamily loans is flagged as a risk, with industry headwinds creating potential for higher credit deterioration and increased reserves.

- Analysts' consensus view underscores concern that rising credit and concentration risks, combined with a shift toward interest-bearing deposits, may compress net interest margins if asset yields do not rise accordingly.

- Consensus highlights that expansion into sectors facing secular challenges could threaten asset quality and require higher capitalization buffers, potentially eating into forecasted profit improvements.

- The trend of declining noninterest-bearing deposits, driven by ongoing high rates and deposit composition, adds to the risk of higher funding costs and margin pressure.

Valuation Gap Signals Opportunity and Caution

- Amalgamated Financial trades at a Price-to-Earnings ratio of 8x based on the current share price of $27.45, which is below both the US Banks industry average (11.3x) and the peer average (10.2x), and also well below the DCF fair value of $65.49.

- Analysts' consensus narrative notes that to reach the consensus price target of $31.5, which is approximately 14.8% above the current share price, the market must believe in both margin improvement and sustained revenue expansion.

- Consensus argues that this discount may reflect skepticism around sector risks and execution on growth initiatives, leaving room for upside if performance meets or beats expectations.

- At the same time, the relatively low valuation provides a margin of safety for investors who are comfortable with the bank’s unique risk profile and business mix.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Amalgamated Financial on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a unique view on the data? Take a few moments to shape your own story and add your perspective: Do it your way

A great starting point for your Amalgamated Financial research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Amalgamated Financial’s increasing exposure to commercial real estate and shifting deposit mix raise concerns about credit risk and potential balance sheet stress in the future.

Looking for stronger financial resilience? Use our solid balance sheet and fundamentals stocks screener (1984 results) to target companies built on robust balance sheets and lower risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:AMAL

Amalgamated Financial

Operates as the bank holding company for Amalgamated Bank that provides commercial and retail banking, investment management, and trust and custody services in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion