Advertisement

- United States

- /

- Auto

- /

- NasdaqGS:TSLA

Investors Are Giving Tesla (NASDAQ:TSLA) A Lot Of Credit For Future Execution

- Tesla is in the early days of its ambitious plans

- Perfect execution is needed to reach its bold targets

- If any doubt arises about its ability to execute, the stock will re-rate downwards significantly

Tesla ( NASDAQ:TSLA ) is easily one of the most controversial companies in the world right now. Most either love it, or hate it. These two groups seem to be split into those who owned it through 2020, and those who watched on the sidelines as the price multiplied 10-fold.

What’s undeniable is the fact that Tesla is working on some exciting innovations in the world’s transition to sustainable energy. The company’s grand ambitions for electric vehicles, autonomous driving, battery design, energy storage and energy generation have contributed to the widely differing opinions on the business’ future. Some believe its plans are possible, while others are skeptical.

Let’s have a look at where Tesla is today versus its future expectations, plus what it needs to do to get there.

Tesla Today Versus Tesla In The Future

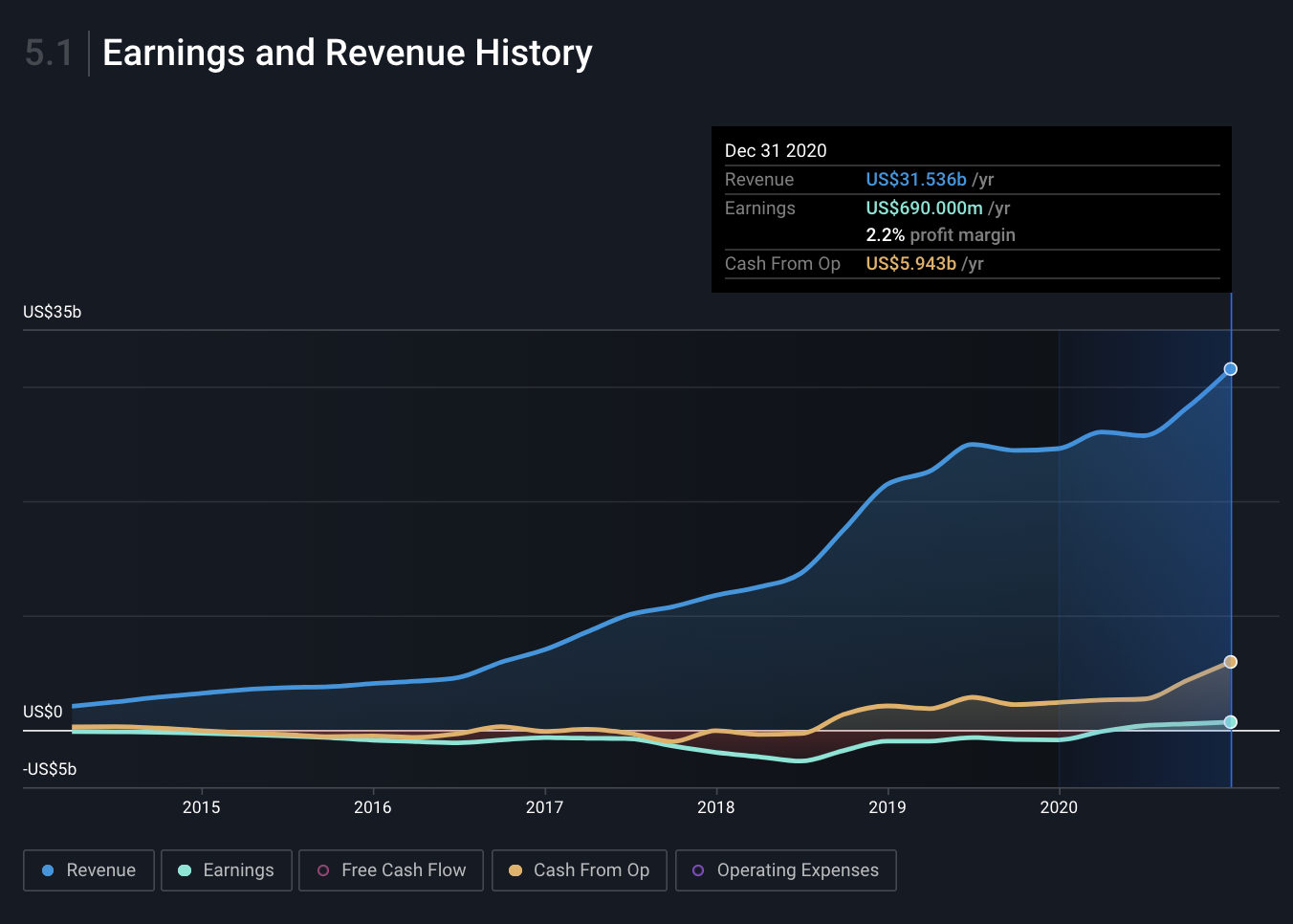

Tesla currently generates revenue through 3 sources: automotive sales and leasing, energy generation and storage, and services. The automotive business generated 86% of total revenue while energy generation and services each contributed 7% during the 2020 financial year.

To understand the expectations related to Tesla’s future, we need to understand where the company is now versus where it is expected to be in say, 10 years time.

In 2020, the company delivered 499,647 vehicles which generated $27.23bn in revenue (sales and leasing combined). That’s a 30% increase over 2019’s automotive revenue. However it should be noted that $1.58bn of this revenue came in the form of tradable regulatory credits. If we exclude these credits for 2019 and 2020, the increase in automotive revenue was 26%.

Source: Earnings and Revenue History - Simply Wall St

The company earns tradable regulatory credits because it operates under regulation related to zero emission vehicles and clean fuel. It sells these credits to other carmakers who want to comply with the regulations and avoid fines, because Tesla doesn’t need them. The CFO stated in an earnings call that demand for these credits will remain strong for the next few years, but as electric vehicles become more mainstream and other manufacturers also begin complying with the regulations through their own operations, earnings from the sales of these credits will decline.

In regards to future expectations for the automotive side, Tesla’s CEO, Elon Musk, stated the company plans to produce 20 million cars per year by 2030. That may sound audacious, and it is. But in 2014 (when it sold around 32k cars) Tesla said that it planned to sell 500k cars by 2020, that also seemed audacious, but it did it.

So to put that 20m into perspective, here’s a few numbers. That means Tesla needs to increase its current production by 40x (a 44% CAGR) and it needs to double what Volksagen and Toyota (the two biggest car makers currently) sold in 2020, which was 9.35 million and 9.5m cars respectively. Plus, market forecasts from the likes of Deloitte and Bloomberg New Energy Finance expect the amount of electric cars sold annually to be around 25m in the year 2030. So if true, this implies that Tesla would have 80% share of the electric vehicle market in 2030, compared to its current 18% in 2020 (it’s the market leader in 2020). Either Tesla is being overly optimistic or the industry forecasts are underestimating the total adoption of electric vehicles in 10 years time.

Considering the company generated 43% YoY growth in cars produced from 2018 to 2020, it will need to continue expanding its production capabilities aggressively to continue this rate of growth. Achieving this growth will rely heavily on three things: first, an improvement in the company’s capital efficiency (continual reduction in production costs), second, the successful creation of many new factories around the world to support production, and third, widespread adoption of Tesla’s Full Self-Driving (FSD) technology (if the software is successful). We will touch more on these points later.

In regards to Tesla’s energy generation and storage business, it deployed 3.02 Gigawatt hours of energy storage products and 205 megawatts of solar energy in 2020.

At Tesla’s recent Battery Day, Musk announced plans to get to 3 Terawatt hours (TWh) per year in batteries by 2030 , which is a 1000x increase from the company’s current installations.

Considering BloombergNEF predicts that energy storage installations around the world will reach 1.1TWh to 2.8TWh by the year 2040 , it appears there are some big discrepancies. Tesla’s forecasted energy installations in 2030 would be more than 100% of what BloombergNEF forecasts for the entire world’s installations.

Again, either Tesla is being optimistic, or industry forecasts are underestimating the growth of global battery installations.

How Does Tesla Reach These Bold Targets

These bold predictions from Tesla seem to be vastly different to what some market research by other firms suggests will occur. Regardless, to achieve what it's claiming is possible, a few things need to occur.

1. Tesla Needs To Spend Big

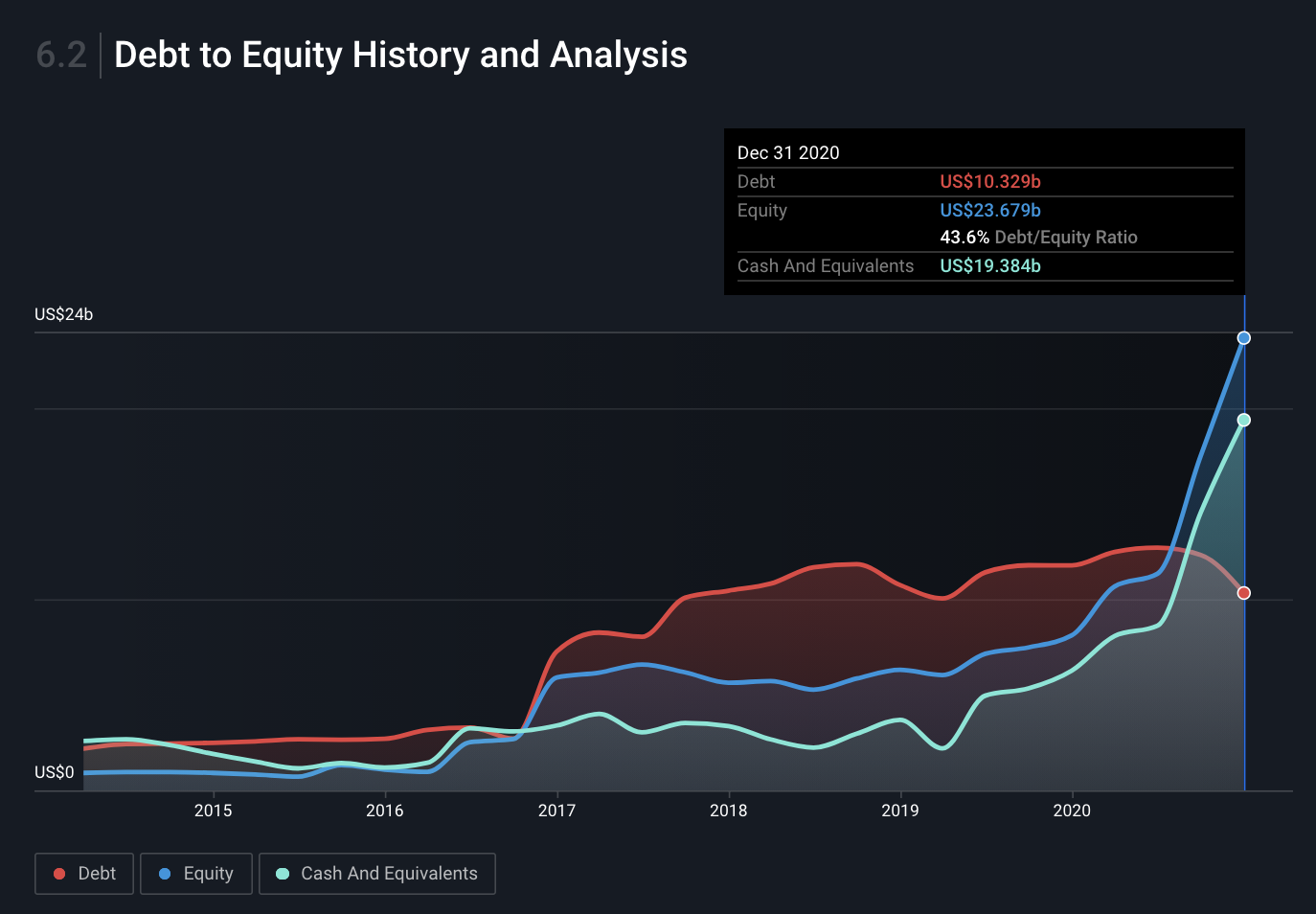

In order to build more factories in its automotive and energy businesses, Tesla will need to spend money, and lots of it. The company had $19.38bn of cash at the end of 2020 (after raising $10bn via equity in the second half of 2020 which was 2% dilutive), generated $5.9bn cash flow from operations, and spent $3.16bn of that on capital expenditures for the year. For 2021, 2022 and 2023, the company expects to spend between $4.5bn and $6bn on capital expenditures per year (page 33 of the 2020 annual report). Some forecasts suggest that Tesla will need somewhere between 20 to 40 new gigafactories to reach its goals by 2030 , which could cost anywhere between $32bn and $64bn over the next 10 years (if we use the $1.6bn cost of the Shanghai factory). On a yearly basis, that would equate to between $3.2bn and $6.4bn of capital expenditure over the next 10 years. Given the current cash flow from operations and the high cash balance, this seems affordable, at least for the next few years.

Here’s an outline of the company debt to equity situation since 2014 from our company report.

Source: Debt to Equity History and Analysis - Simply Wall St

2. Tesla’s FSD needs to win

Tesla FSD software is up against almost every other company in the space (e.g. Waymo, GM, Toyota) which is using LIDAR technology. It’s beyond the scope of this article to outline the technological differences between the two (and they are significant) but what is important to keep in mind is that neither are at full level 5 autonomy just yet. Which means both systems are yet to prove they have the capabilities for full autonomy, without a human driver.

However, while Tesla’s FSD software is reportedly only at level 2 autonomy, it claims it will be at level 5 (i.e. fully autonomous) by the end of 2021. This could be due to the fact that it has accrued somewhere in the range of 3 billion miles of data from its fleet of cars on the road to build its FSD software. This is significantly more data than its competitors. So if that software comes to market successfully at the end of this year like the company plans, that would provide more substantial evidence that supports Tesla’s case for being the market leader in autonomous driving software and driving its potential exponential growth. Not only that, the software would provide a very high margin source of recurring revenue. But again, that’s yet to happen, and if it does experience any hiccups in the process, it could be incredibly damaging. So execution is key.

3. Tesla needs to continue improving capital efficiency to grow

In the manufacturing business, capital efficiency is key to growing production rapidly and affordably. Ark Invest, one of the most widely known bulls on Tesla (Ark owns around $3.7bn of Tesla across its ETFs), believes there is a 50/50 chance Tesla will be more capital efficient than traditional US auto-makers . The Bureau of Economic Analysis showed that traditional US automakers spent $14k per car on fixed assets in 2016. For reference, Tesla Shanghai factory required $1.6bn in financing with an initial capacity of 150,000 cars, meaning it costs $10,700 per car (Shanghai recently reached production of 8k cars per week, and expects to produce 550k cars in 2021 ). In order for production to grow rapidly and affordably and enable this growth required to get to 20m cars by 2030, Tesla needs to continue to improve its efficiencies and productivity even further with its future factories.

The thing here is that it seems a lot of Tesla's current market price is counting on the successful execution of these future events playing out. The CEO even noted this to employees in an internal letter in 2020 . The expectations of exponential growth are reliant on simultaneously expanding production capabilities, increasing productivity, and successfully delivering FSD software to market. The company has a track record of executing, but if any doubt arises from investors about their ability to further execute, it would be incredibly damaging to the stock price.

What This Means For Investors

While Tesla seems to still be in the early days of its ambitious plans, the current market valuation of the stock seems to largely expect that all of these developments occur, even though they’re likely years away and also not guaranteed. The huge share price increase in 2020 versus more conservative growth in the actual business, indicates that a lot of the rise was due to increasing expectations that the company would successfully execute. As investors, we need to assess a range of possible future outcomes, assess the probability of each outcome occurring, and estimate the potential risk-reward that comes with each outcome playing out.

There’s a saying from Charlie Munger that goes, “No matter how wonderful a business is, it’s not worth an infinite price”. It’s up to us as investors to determine what an appropriate price is.

For our full analysis on Tesla’s future, past, financial health, management and more, you can check out our company report .

Valuation is complex, but we're here to simplify it.

Discover if Tesla might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Michael Paige and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Michael Paige

Michael is the Content Lead at Simply Wall St. With over 9 years of experience analysing and researching companies, Michael contributes to the creation of our analytical content and has done so as an equity analyst since 2020. He previously worked as an Associate Adviser at Ord Minnett, helping build and manage clients' portfolios, and has been investing personally since 2015.

About NasdaqGS:TSLA

Tesla

Designs, develops, manufactures, leases, and sells electric vehicles, and energy generation and storage systems in the United States, China, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor