- Taiwan

- /

- Infrastructure

- /

- TWSE:2633

Taiwan High Speed Rail Corporation's (TWSE:2633) Popularity With Investors Is Under Threat From Overpricing

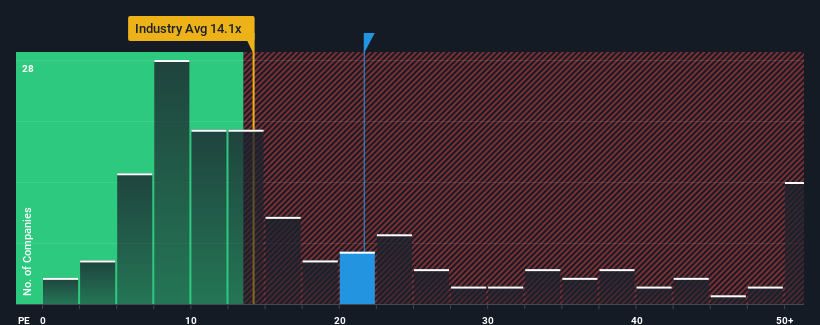

It's not a stretch to say that Taiwan High Speed Rail Corporation's (TWSE:2633) price-to-earnings (or "P/E") ratio of 21.6x right now seems quite "middle-of-the-road" compared to the market in Taiwan, where the median P/E ratio is around 23x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

With earnings growth that's exceedingly strong of late, Taiwan High Speed Rail has been doing very well. The P/E is probably moderate because investors think this strong earnings growth might not be enough to outperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Check out our latest analysis for Taiwan High Speed Rail

Is There Some Growth For Taiwan High Speed Rail?

In order to justify its P/E ratio, Taiwan High Speed Rail would need to produce growth that's similar to the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 108% last year. Pleasingly, EPS has also lifted 34% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 26% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we find it interesting that Taiwan High Speed Rail is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited recent growth rates and are willing to pay up for exposure to the stock. They may be setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

What We Can Learn From Taiwan High Speed Rail's P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Taiwan High Speed Rail currently trades on a higher than expected P/E since its recent three-year growth is lower than the wider market forecast. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless the recent medium-term conditions improve, it's challenging to accept these prices as being reasonable.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Taiwan High Speed Rail (at least 2 which are a bit concerning), and understanding them should be part of your investment process.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Taiwan High Speed Rail might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2633

Taiwan High Speed Rail

Taiwan High Speed Rail Corporation constructs, operates, and manages a high-speed railway system and related facilities in Taiwan.

Second-rate dividend payer and slightly overvalued.

Market Insights

Community Narratives