Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Quanta Computer Inc. (TWSE:2382) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Quanta Computer

How Much Debt Does Quanta Computer Carry?

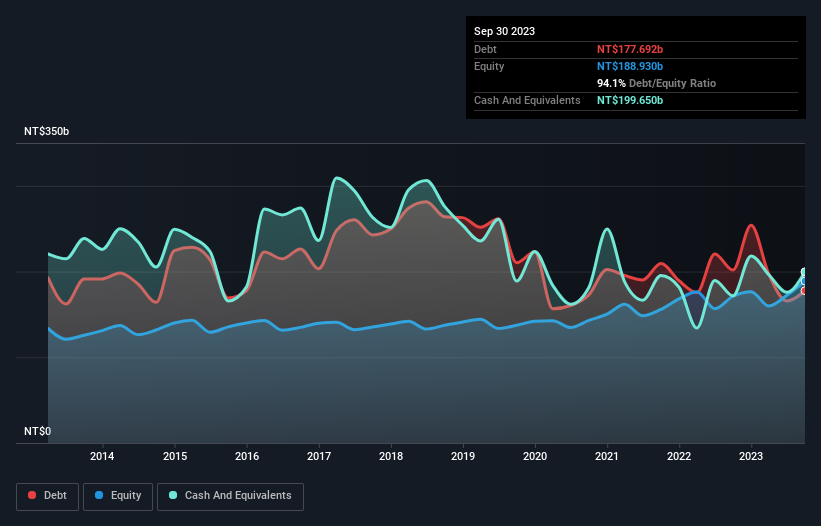

The image below, which you can click on for greater detail, shows that Quanta Computer had debt of NT$177.7b at the end of September 2023, a reduction from NT$201.7b over a year. But it also has NT$199.7b in cash to offset that, meaning it has NT$22.0b net cash.

How Healthy Is Quanta Computer's Balance Sheet?

We can see from the most recent balance sheet that Quanta Computer had liabilities of NT$525.2b falling due within a year, and liabilities of NT$9.92b due beyond that. Offsetting these obligations, it had cash of NT$199.7b as well as receivables valued at NT$292.7b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by NT$42.7b.

Since publicly traded Quanta Computer shares are worth a very impressive total of NT$896.2b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Quanta Computer also has more cash than debt, so we're pretty confident it can manage its debt safely.

In addition to that, we're happy to report that Quanta Computer has boosted its EBIT by 32%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Quanta Computer can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Quanta Computer may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Quanta Computer produced sturdy free cash flow equating to 69% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

We could understand if investors are concerned about Quanta Computer's liabilities, but we can be reassured by the fact it has has net cash of NT$22.0b. And we liked the look of last year's 32% year-on-year EBIT growth. So we don't think Quanta Computer's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with Quanta Computer , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Quanta Computer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2382

Quanta Computer

Manufactures and sells notebook computers in Asia, the Americas, Europe, and internationally.

Very undervalued with exceptional growth potential and pays a dividend.

Similar Companies

Market Insights

Community Narratives