- Taiwan

- /

- Tech Hardware

- /

- TWSE:2357

Declining Stock and Decent Financials: Is The Market Wrong About ASUSTeK Computer Inc. (TWSE:2357)?

With its stock down 8.0% over the past month, it is easy to disregard ASUSTeK Computer (TWSE:2357). However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Specifically, we decided to study ASUSTeK Computer's ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for ASUSTeK Computer is:

12% = NT$34b ÷ NT$297b (Based on the trailing twelve months to December 2024).

The 'return' is the yearly profit. So, this means that for every NT$1 of its shareholder's investments, the company generates a profit of NT$0.12.

View our latest analysis for ASUSTeK Computer

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

ASUSTeK Computer's Earnings Growth And 12% ROE

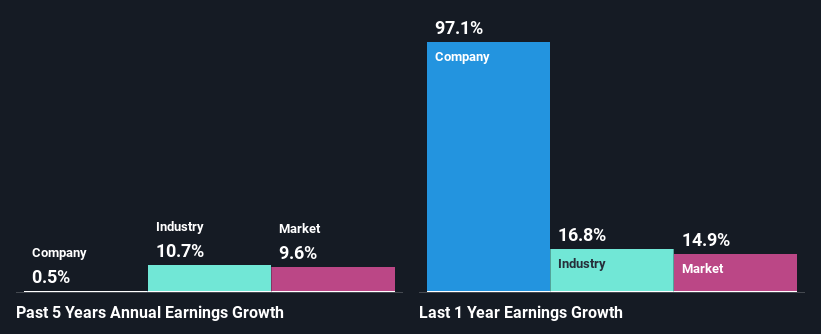

To begin with, ASUSTeK Computer seems to have a respectable ROE. Even when compared to the industry average of 13% the company's ROE looks quite decent. However, we are curious as to how ASUSTeK Computer's decent returns still resulted in flat growth for ASUSTeK Computer in the past five years. Based on this, we feel that there might be other reasons which haven't been discussed so far in this article that could be hampering the company's growth. These include low earnings retention or poor allocation of capital.

We then compared ASUSTeK Computer's net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 11% in the same 5-year period, which is a bit concerning.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is ASUSTeK Computer fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is ASUSTeK Computer Using Its Retained Earnings Effectively?

ASUSTeK Computer has a high three-year median payout ratio of 79% (or a retention ratio of 21%), meaning that the company is paying most of its profits as dividends to its shareholders. This does go some way in explaining why there's been no growth in its earnings.

Moreover, ASUSTeK Computer has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 76%. However, ASUSTeK Computer's ROE is predicted to rise to 15% despite there being no anticipated change in its payout ratio.

Conclusion

On the whole, we do feel that ASUSTeK Computer has some positive attributes. However, while the company does have a high ROE, its earnings growth number is quite disappointing. This can be blamed on the fact that it reinvests only a small portion of its profits and pays out the rest as dividends. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2357

ASUSTeK Computer

Researches and develops, designs, manufactures, sells, and repairs computers, communications, and consumer electronic products in Taiwan, China, Singapore, Europe, the United States, and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives