- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:3049

Our Take On The Returns On Capital At HannsTouch Solution (TPE:3049)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Although, when we looked at HannsTouch Solution (TPE:3049), it didn't seem to tick all of these boxes.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on HannsTouch Solution is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.029 = NT$447m ÷ (NT$16b - NT$647m) (Based on the trailing twelve months to September 2020).

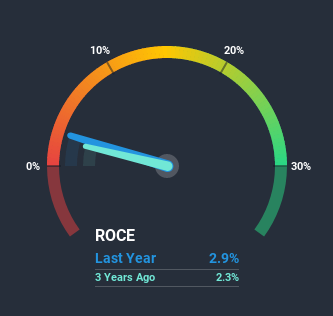

Therefore, HannsTouch Solution has an ROCE of 2.9%. In absolute terms, that's a low return and it also under-performs the Electronic industry average of 11%.

Check out our latest analysis for HannsTouch Solution

Historical performance is a great place to start when researching a stock so above you can see the gauge for HannsTouch Solution's ROCE against it's prior returns. If you're interested in investigating HannsTouch Solution's past further, check out this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For HannsTouch Solution Tell Us?

When we looked at the ROCE trend at HannsTouch Solution, we didn't gain much confidence. Over the last five years, returns on capital have decreased to 2.9% from 6.7% five years ago. And considering revenue has dropped while employing more capital, we'd be cautious. This could mean that the business is losing its competitive advantage or market share, because while more money is being put into ventures, it's actually producing a lower return - "less bang for their buck" per se.

On a related note, HannsTouch Solution has decreased its current liabilities to 4.0% of total assets. So we could link some of this to the decrease in ROCE. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

The Key Takeaway

From the above analysis, we find it rather worrisome that returns on capital and sales for HannsTouch Solution have fallen, meanwhile the business is employing more capital than it was five years ago. Investors must expect better things on the horizon though because the stock has risen 24% in the last five years. Regardless, we don't like the trends as they are and if they persist, we think you might find better investments elsewhere.

On a separate note, we've found 3 warning signs for HannsTouch Solution you'll probably want to know about.

While HannsTouch Solution isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading HannsTouch Solution or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if HannsTouch Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:3049

HannsTouch Holdings

Manufactures and sells touch sensors in Taiwan, South Korea, China, and Europe.

Imperfect balance sheet and overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion