Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:2455

Calculating The Intrinsic Value Of Visual Photonics Epitaxy Co., Ltd. (TWSE:2455)

Key Insights

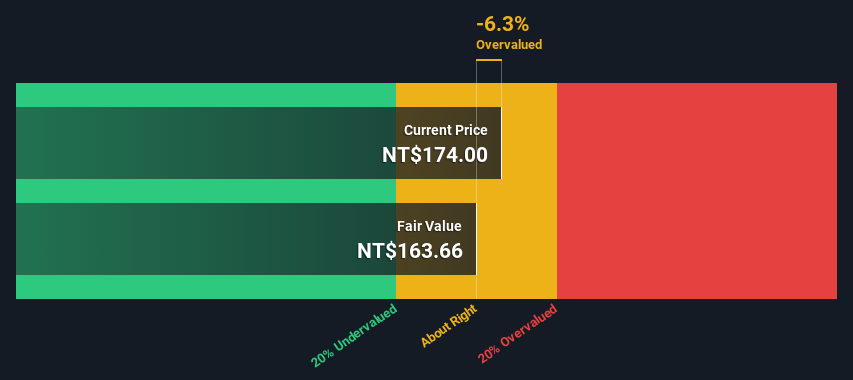

- The projected fair value for Visual Photonics Epitaxy is NT$164 based on 2 Stage Free Cash Flow to Equity

- Current share price of NT$174 suggests Visual Photonics Epitaxy is potentially trading close to its fair value

- Analyst price target for 2455 is NT$183, which is 12% above our fair value estimate

In this article we are going to estimate the intrinsic value of Visual Photonics Epitaxy Co., Ltd. (TWSE:2455) by estimating the company's future cash flows and discounting them to their present value. We will take advantage of the Discounted Cash Flow (DCF) model for this purpose. Before you think you won't be able to understand it, just read on! It's actually much less complex than you'd imagine.

We generally believe that a company's value is the present value of all of the cash it will generate in the future. However, a DCF is just one valuation metric among many, and it is not without flaws. For those who are keen learners of equity analysis, the Simply Wall St analysis model here may be something of interest to you.

Check out our latest analysis for Visual Photonics Epitaxy

The Model

We are going to use a two-stage DCF model, which, as the name states, takes into account two stages of growth. The first stage is generally a higher growth period which levels off heading towards the terminal value, captured in the second 'steady growth' period. To begin with, we have to get estimates of the next ten years of cash flows. Where possible we use analyst estimates, but when these aren't available we extrapolate the previous free cash flow (FCF) from the last estimate or reported value. We assume companies with shrinking free cash flow will slow their rate of shrinkage, and that companies with growing free cash flow will see their growth rate slow, over this period. We do this to reflect that growth tends to slow more in the early years than it does in later years.

A DCF is all about the idea that a dollar in the future is less valuable than a dollar today, so we discount the value of these future cash flows to their estimated value in today's dollars:

10-year free cash flow (FCF) estimate

| 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | |

| Levered FCF (NT$, Millions) | NT$1.07b | NT$1.45b | NT$1.74b | NT$1.98b | NT$2.18b | NT$2.35b | NT$2.47b | NT$2.58b | NT$2.66b | NT$2.72b |

| Growth Rate Estimate Source | Analyst x3 | Analyst x2 | Est @ 19.66% | Est @ 14.05% | Est @ 10.13% | Est @ 7.38% | Est @ 5.46% | Est @ 4.11% | Est @ 3.17% | Est @ 2.51% |

| Present Value (NT$, Millions) Discounted @ 8.3% | NT$992 | NT$1.2k | NT$1.4k | NT$1.4k | NT$1.5k | NT$1.5k | NT$1.4k | NT$1.4k | NT$1.3k | NT$1.2k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = NT$13b

The second stage is also known as Terminal Value, this is the business's cash flow after the first stage. The Gordon Growth formula is used to calculate Terminal Value at a future annual growth rate equal to the 5-year average of the 10-year government bond yield of 1.0%. We discount the terminal cash flows to today's value at a cost of equity of 8.3%.

Terminal Value (TV)= FCF2034 × (1 + g) ÷ (r – g) = NT$2.7b× (1 + 1.0%) ÷ (8.3%– 1.0%) = NT$38b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= NT$38b÷ ( 1 + 8.3%)10= NT$17b

The total value, or equity value, is then the sum of the present value of the future cash flows, which in this case is NT$30b. In the final step we divide the equity value by the number of shares outstanding. Relative to the current share price of NT$174, the company appears around fair value at the time of writing. Remember though, that this is just an approximate valuation, and like any complex formula - garbage in, garbage out.

The Assumptions

The calculation above is very dependent on two assumptions. The first is the discount rate and the other is the cash flows. Part of investing is coming up with your own evaluation of a company's future performance, so try the calculation yourself and check your own assumptions. The DCF also does not consider the possible cyclicality of an industry, or a company's future capital requirements, so it does not give a full picture of a company's potential performance. Given that we are looking at Visual Photonics Epitaxy as potential shareholders, the cost of equity is used as the discount rate, rather than the cost of capital (or weighted average cost of capital, WACC) which accounts for debt. In this calculation we've used 8.3%, which is based on a levered beta of 1.334. Beta is a measure of a stock's volatility, compared to the market as a whole. We get our beta from the industry average beta of globally comparable companies, with an imposed limit between 0.8 and 2.0, which is a reasonable range for a stable business.

SWOT Analysis for Visual Photonics Epitaxy

Strength

- Earnings growth over the past year exceeded the industry.

- Debt is not viewed as a risk.

- Dividends are covered by earnings and cash flows.

Weakness

- Dividend is low compared to the top 25% of dividend payers in the Semiconductor market.

- Expensive based on P/E ratio and estimated fair value.

Opportunity

- Annual earnings are forecast to grow faster than the Taiwanese market.

Threat

- Revenue is forecast to grow slower than 20% per year.

Next Steps:

Although the valuation of a company is important, it is only one of many factors that you need to assess for a company. It's not possible to obtain a foolproof valuation with a DCF model. Instead the best use for a DCF model is to test certain assumptions and theories to see if they would lead to the company being undervalued or overvalued. For instance, if the terminal value growth rate is adjusted slightly, it can dramatically alter the overall result. For Visual Photonics Epitaxy, we've compiled three further aspects you should explore:

- Financial Health: Does 2455 have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Future Earnings: How does 2455's growth rate compare to its peers and the wider market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

- Other Solid Businesses: Low debt, high returns on equity and good past performance are fundamental to a strong business. Why not explore our interactive list of stocks with solid business fundamentals to see if there are other companies you may not have considered!

PS. Simply Wall St updates its DCF calculation for every Taiwanese stock every day, so if you want to find the intrinsic value of any other stock just search here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2455

Visual Photonics Epitaxy

Engages in the research and development, manufacture, and sale of optoelectronic semiconductors and optoelectronic components products in Taiwan, the United States, China, and internationally.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8684.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

WA

Wane_Investment_House on FCMB Group ·

This aligns FCMB with global green finance standards and strengthens its attractiveness to impact investors. 4. Deepens Strategic Partnerships and International Collaboration The collaboration with FMO and HeaveVentures broadens FCMB’s relationship with: Development finance institutions (DFIs), Venture capital and innovation hubs, Global agri-value chain partners. These partnerships provide FCMB with: Access to co-financing opportunities, Technical expertise, Future pipeline collaboration, which collectively expands FCMB’s capacity to support complex and scalable agribusiness projects. 5. Builds a Pipeline for Future Lending, Investment, and Market Expansion The Hackathon serves as a feeder mechanism into FCMB’s broader agribusiness strategy by: Identifying innovative startups that can evolve into long-term borrowers or partners. Creating opportunities for structured financing, contract farming solutions, and supply-chain digitization. Enhancing FCMB’s advisory and merchant banking relevance in the agritech investment landscape. This creates a sustainable pipeline of bankable opportunities in a sector with high long-term growth potential. 6. Strengthens FCMB’s Brand Positioning and Competitive Advantage The initiative differentiates FCMB from peer institutions by: Showcasing its commitment to innovation-led economic transformation. Demonstrating leadership in supporting Nigeria’s food security agenda. Reinforcing customer loyalty in the SME and agribusiness segments. This positions FCMB as a future-ready financial partner with strong sectoral expertise and deep development impact. Strategic Outlook The FCMB AgriTech Hackathon 2025 is expected to deliver medium-to-long-term value by: Deepening FCMB’s market share in agribusiness finance, Enabling new digital lending frameworks, Strengthening ESG positioning, Expanding cross-border innovation partnerships, Supporting scalable agritech solutions capable of transforming Nigeria’s food system.

0

|0