Advertisement

- Taiwan

- /

- Tech Hardware

- /

- TWSE:2377

Global Market Highlights 3 Stocks That May Be Trading Below Their Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a challenging landscape marked by easing U.S. inflation, ongoing trade policy uncertainties, and recession fears, investors are keenly observing the performance of major indices like the S&P 500 and Nasdaq Composite, which have recently faced consecutive weeks of negative returns. In this environment where economic indicators fluctuate and sentiment is cautious, identifying undervalued stocks can offer potential opportunities for investors seeking value.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Guizhou Space Appliance (SZSE:002025) | CN¥58.35 | CN¥115.74 | 49.6% |

| Storytel (OM:STORY B) | SEK90.85 | SEK180.37 | 49.6% |

| Takara Bio (TSE:4974) | ¥853.00 | ¥1696.74 | 49.7% |

| APAC Realty (SGX:CLN) | SGD0.43 | SGD0.85 | 49.6% |

| JSHLtd (TSE:150A) | ¥558.00 | ¥1106.93 | 49.6% |

| Nan Ya Printed Circuit Board (TWSE:8046) | NT$132.00 | NT$262.13 | 49.6% |

| Sunny Optical Technology (Group) (SEHK:2382) | HK$88.50 | HK$175.51 | 49.6% |

| Jiangsu Chuanzhiboke Education Technology (SZSE:003032) | CN¥8.53 | CN¥16.91 | 49.6% |

| Shenzhen Anche Technologies (SZSE:300572) | CN¥18.60 | CN¥37.18 | 50% |

| Doosan Fuel Cell (KOSE:A336260) | ₩15880.00 | ₩31544.03 | 49.7% |

Here's a peek at a few of the choices from the screener.

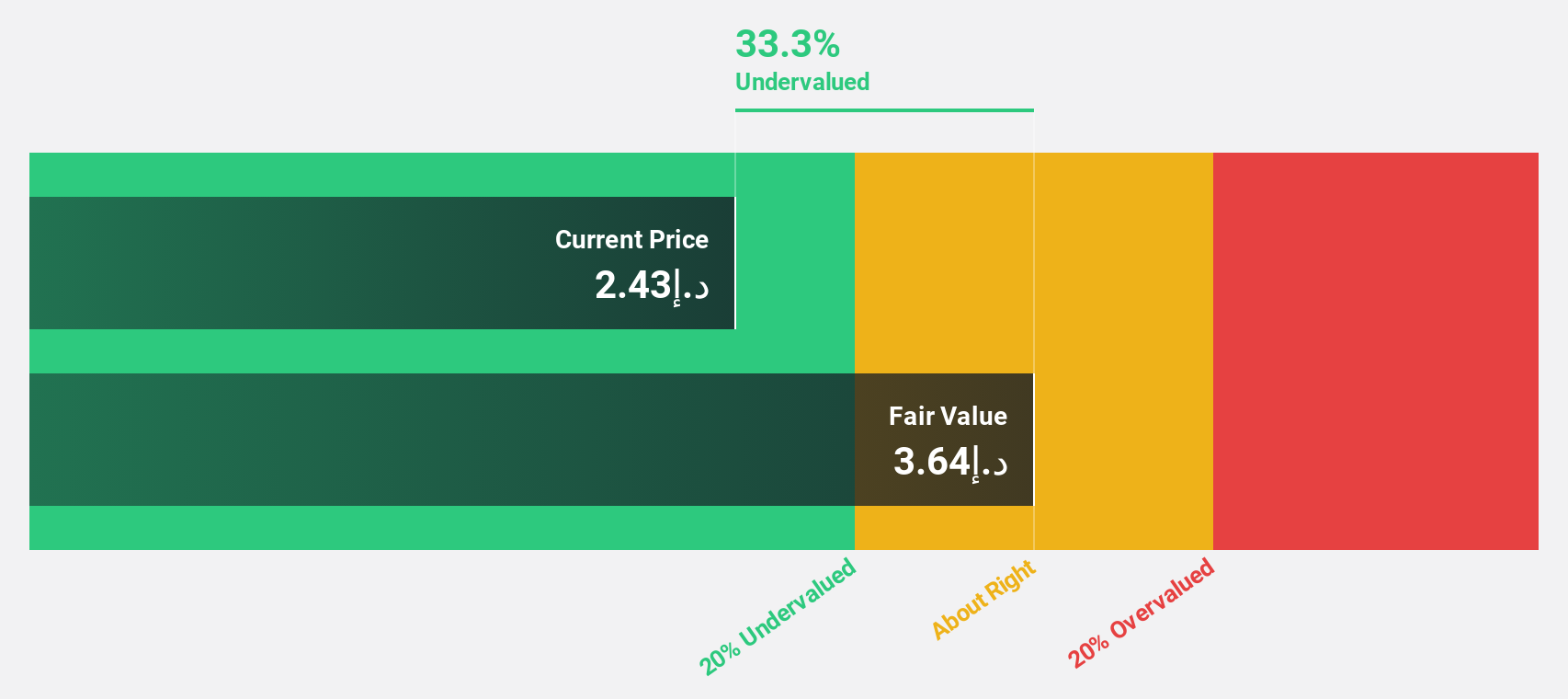

Pure Health Holding PJSC (ADX:PUREHEALTH)

Overview: Pure Health Holding PJSC operates in the healthcare services sector in the United Arab Emirates, with a market capitalization of approximately AED32.67 billion.

Operations: The company generates revenue through various segments including Diagnostic Services (AED1.06 billion), Technology and Others (AED468.57 million), Health Insurance Services (AED6.84 billion), Hospital and Other Healthcare Related Services (AED19.65 billion), and Procurement and Supply of Medical Related Products (AED5.20 billion).

Estimated Discount To Fair Value: 10.3%

Pure Health Holding PJSC is trading at AED2.94, slightly below its fair value of AED3.28, suggesting it may be undervalued based on cash flows. Despite a modest revenue growth forecast of 9% annually, earnings are expected to grow significantly at 20.95% per year, outpacing the AE market's average. Recent earnings showed substantial improvement with net income rising to AED 1.71 billion from AED 964.66 million last year, indicating strong profitability momentum.

- Insights from our recent growth report point to a promising forecast for Pure Health Holding PJSC's business outlook.

- Click to explore a detailed breakdown of our findings in Pure Health Holding PJSC's balance sheet health report.

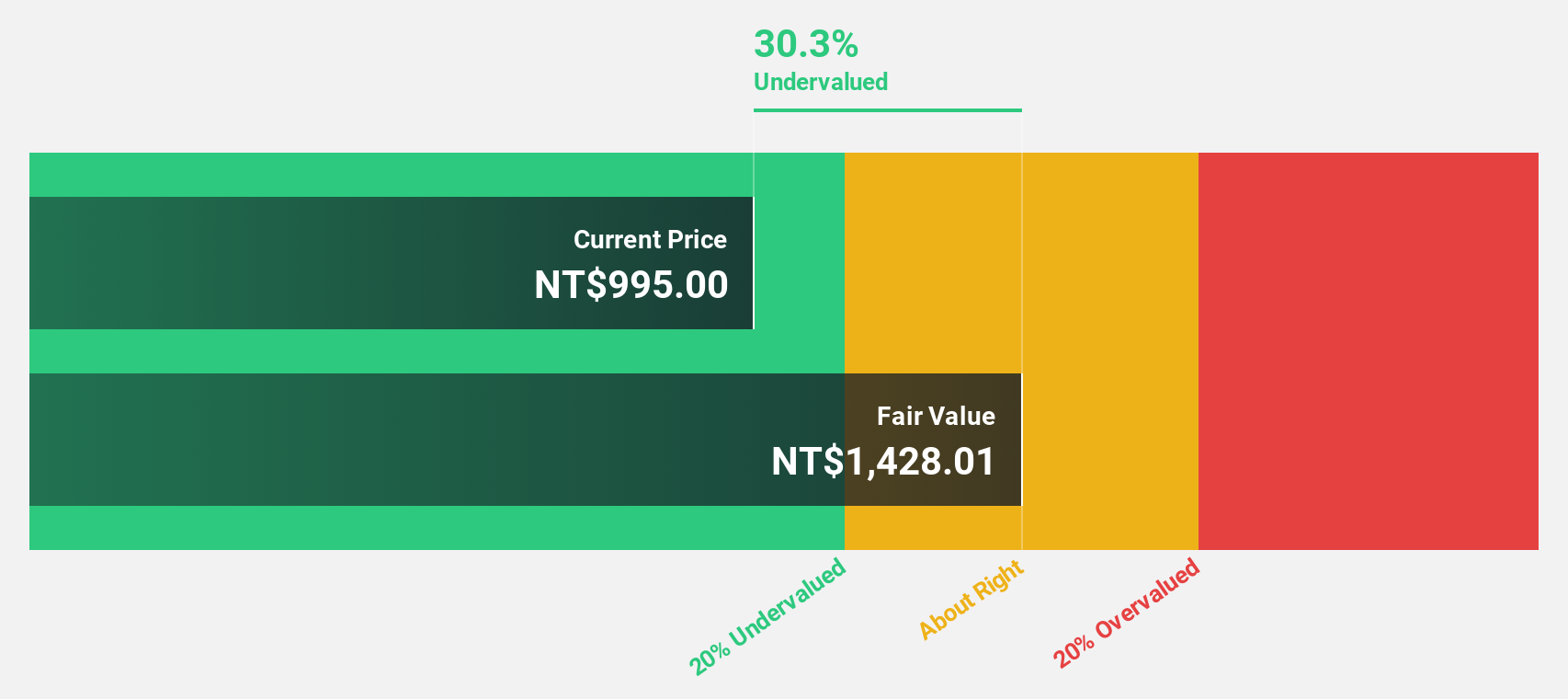

Taiwan Semiconductor Manufacturing (TWSE:2330)

Overview: Taiwan Semiconductor Manufacturing Company Limited, with a market cap of NT$24.69 trillion, operates globally by manufacturing, packaging, testing, and selling integrated circuits and other semiconductor devices.

Operations: The company's revenue segment primarily consists of its Foundry operations, which generated NT$2.89 billion.

Estimated Discount To Fair Value: 40.9%

Taiwan Semiconductor Manufacturing is trading at NT$982, significantly below its fair value estimate of NT$1662.74, highlighting potential undervaluation based on cash flows. The company's earnings are projected to grow at 16.6% annually, surpassing the Taiwan market average growth rate of 15.7%. Recent revenue reports show a robust increase with February's net revenue reaching TWD 260 billion compared to TWD 181.65 billion last year, supporting strong cash flow generation capabilities.

- According our earnings growth report, there's an indication that Taiwan Semiconductor Manufacturing might be ready to expand.

- Click here to discover the nuances of Taiwan Semiconductor Manufacturing with our detailed financial health report.

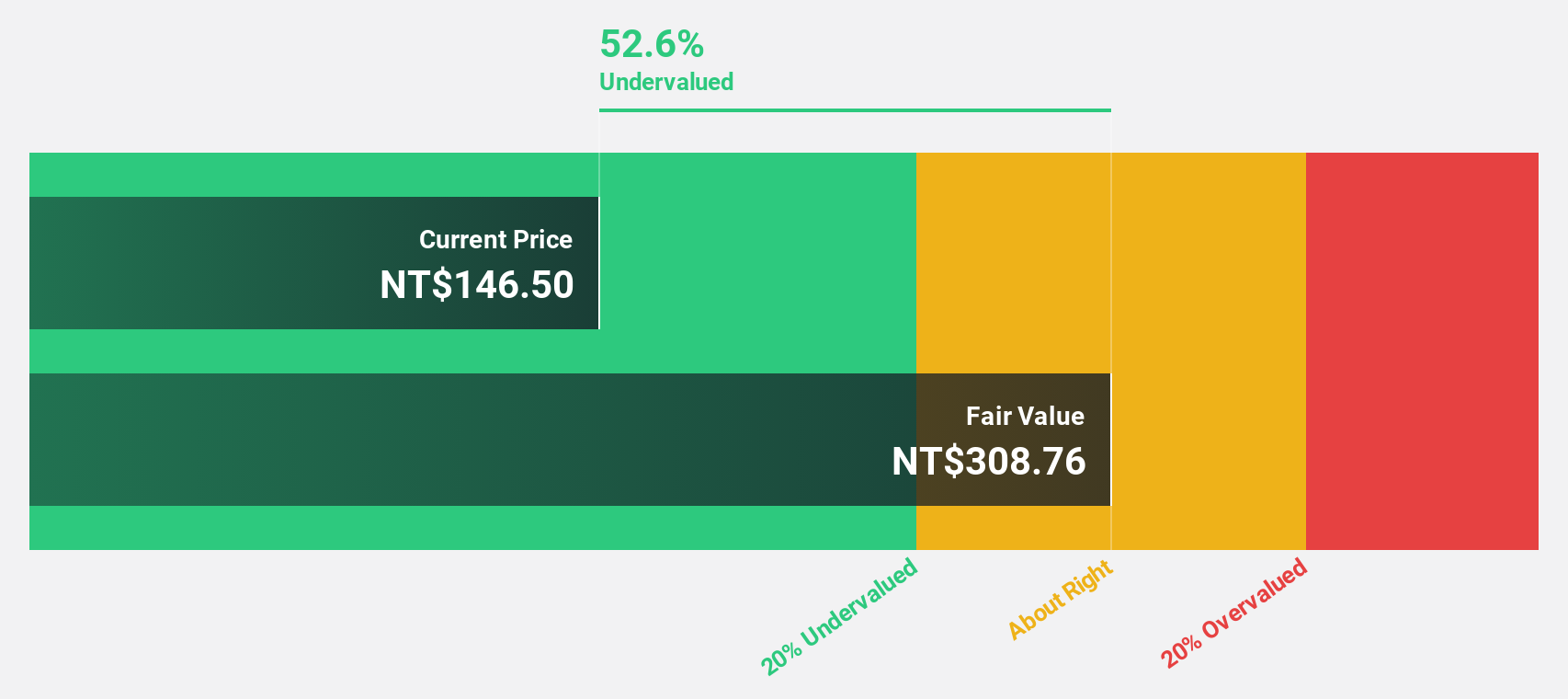

Micro-Star International (TWSE:2377)

Overview: Micro-Star International Co., Ltd. is a company that manufactures and sells motherboards, interface cards, notebook computers, and other electronic products globally, with a market cap of NT$144.47 billion.

Operations: The company's revenue from the Computer and Peripherals segment amounts to NT$197.83 billion.

Estimated Discount To Fair Value: 38.4%

Micro-Star International is trading at NT$171.5, significantly below its estimated fair value of NT$278.44, suggesting undervaluation based on cash flows. Despite a decrease in net income to TWD 6.79 billion from TWD 7.53 billion the previous year, the company's earnings are expected to grow significantly at 30.69% annually, outpacing both revenue growth and the Taiwan market average. However, its dividend yield of 2.92% is not fully supported by free cash flows.

- Upon reviewing our latest growth report, Micro-Star International's projected financial performance appears quite optimistic.

- Take a closer look at Micro-Star International's balance sheet health here in our report.

Summing It All Up

- Discover the full array of 505 Undervalued Global Stocks Based On Cash Flows right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2377

Micro-Star International

Manufactures and sells motherboards, interface cards, notebook computers, and other electronic products in Asia, Europe, the United States, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|17.0% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|11.8% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|81.8% undervalued

NO

Community Contributor