Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Taiwan Semiconductor Manufacturing Company Limited (TPE:2330) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Taiwan Semiconductor Manufacturing

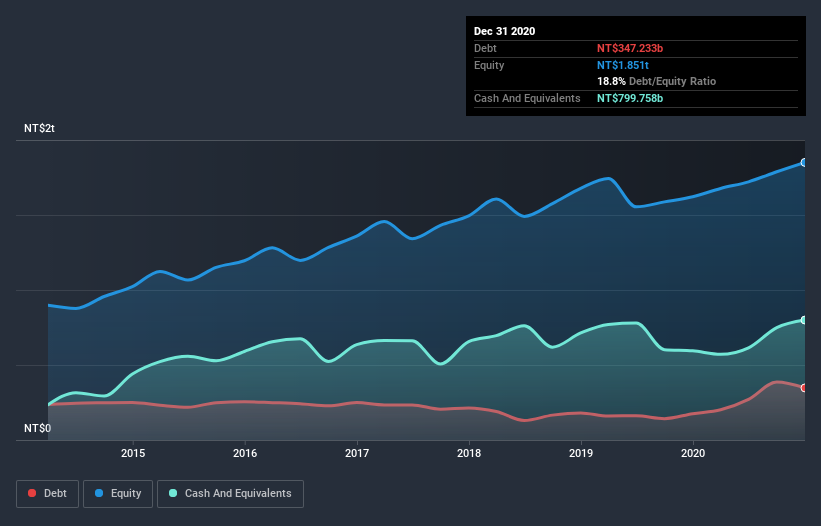

How Much Debt Does Taiwan Semiconductor Manufacturing Carry?

As you can see below, at the end of December 2020, Taiwan Semiconductor Manufacturing had NT$347.2b of debt, up from NT$175.4b a year ago. Click the image for more detail. But it also has NT$799.8b in cash to offset that, meaning it has NT$452.5b net cash.

How Strong Is Taiwan Semiconductor Manufacturing's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Taiwan Semiconductor Manufacturing had liabilities of NT$617.2b due within 12 months and liabilities of NT$292.9b due beyond that. Offsetting these obligations, it had cash of NT$799.8b as well as receivables valued at NT$146.1b due within 12 months. So it actually has NT$35.8b more liquid assets than total liabilities.

This state of affairs indicates that Taiwan Semiconductor Manufacturing's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the NT$16t company is short on cash, but still worth keeping an eye on the balance sheet. Simply put, the fact that Taiwan Semiconductor Manufacturing has more cash than debt is arguably a good indication that it can manage its debt safely.

On top of that, Taiwan Semiconductor Manufacturing grew its EBIT by 51% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Taiwan Semiconductor Manufacturing's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Taiwan Semiconductor Manufacturing may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Taiwan Semiconductor Manufacturing produced sturdy free cash flow equating to 53% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While it is always sensible to investigate a company's debt, in this case Taiwan Semiconductor Manufacturing has NT$452.5b in net cash and a decent-looking balance sheet. And it impressed us with its EBIT growth of 51% over the last year. So is Taiwan Semiconductor Manufacturing's debt a risk? It doesn't seem so to us. Over time, share prices tend to follow earnings per share, so if you're interested in Taiwan Semiconductor Manufacturing, you may well want to click here to check an interactive graph of its earnings per share history.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you’re looking to trade Taiwan Semiconductor Manufacturing, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Taiwan Semiconductor Manufacturing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:2330

Taiwan Semiconductor Manufacturing

Manufactures, packages, tests, and sells integrated circuits and other semiconductor devices in Taiwan, China, Europe, the Middle East, Africa, Japan, the United States, and internationally.

Outstanding track record, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|13.7% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|69.6% undervalued

OI

Community Contributor