Advertisement

- Taiwan

- /

- Semiconductors

- /

- TPEX:5315

Are Dividend Investors Getting More Than They Bargained For With United Radiant Technology Corporation's (GTSM:5315) Dividend?

Today we'll take a closer look at United Radiant Technology Corporation (GTSM:5315) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. Yet sometimes, investors buy a stock for its dividend and lose money because the share price falls by more than they earned in dividend payments.

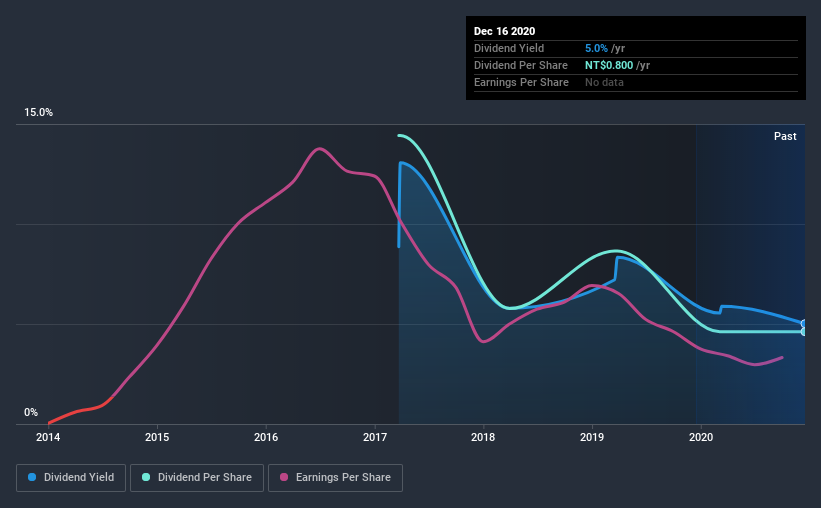

In this case, United Radiant Technology likely looks attractive to dividend investors, given its 5.0% dividend yield and four-year payment history. It sure looks interesting on these metrics - but there's always more to the story. The company also bought back stock equivalent to around 2.2% of market capitalisation this year. Some simple analysis can reduce the risk of holding United Radiant Technology for its dividend, and we'll focus on the most important aspects below.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. In the last year, United Radiant Technology paid out 111% of its profit as dividends. A payout ratio above 100% is definitely an item of concern, unless there are some other circumstances that would justify it.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. United Radiant Technology paid out 566% of its free cash last year. Cash flows can be lumpy, but this dividend was not well covered by cash flow. Paying out such a high percentage of cash flow suggests that the dividend was funded from either cash at bank or by borrowing, neither of which is desirable over the long term. Cash is slightly more important than profit from a dividend perspective, but given United Radiant Technology's payouts were not well covered by either earnings or cash flow, we would definitely be concerned about the sustainability of this dividend.

While the above analysis focuses on dividends relative to a company's earnings, we do note United Radiant Technology's strong net cash position, which will let it pay larger dividends for a time, should it choose.

Remember, you can always get a snapshot of United Radiant Technology's latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. Looking at the data, we can see that United Radiant Technology has been paying a dividend for the past four years. This company's dividend has been unstable, and with a relatively short history, we think it's a little soon to draw strong conclusions about its long term dividend potential. During the past four-year period, the first annual payment was NT$2.5 in 2016, compared to NT$0.8 last year. The dividend has fallen 68% over that period.

We struggle to make a case for buying United Radiant Technology for its dividend, given that payments have shrunk over the past four years.

Dividend Growth Potential

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS are growing. It's not great to see that United Radiant Technology's have fallen at approximately 5.1% over the past five years. If earnings continue to decline, the dividend may come under pressure. Every investor should make an assessment of whether the company is taking steps to stabilise the situation.

Conclusion

To summarise, shareholders should always check that United Radiant Technology's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. United Radiant Technology paid out almost all of its cash flow and profit as dividends, leaving little to reinvest in the business. Earnings per share have been falling, and the company has cut its dividend at least once in the past. From a dividend perspective, this is a cause for concern. There are a few too many issues for us to get comfortable with United Radiant Technology from a dividend perspective. Businesses can change, but we would struggle to identify why an investor should rely on this stock for their income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Just as an example, we've come accross 4 warning signs for United Radiant Technology you should be aware of, and 1 of them is concerning.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

When trading United Radiant Technology or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:5315

United Radiant Technology

Manufactures and sells liquid crystal display panels and modules.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|32.1% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|34.7% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|29.9% undervalued

EV

Community Contributor