Advertisement

- Taiwan

- /

- Semiconductors

- /

- TPEX:5245

These 4 Measures Indicate That WiseChip Semiconductor (GTSM:5245) Is Using Debt Safely

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, WiseChip Semiconductor Inc. (GTSM:5245) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for WiseChip Semiconductor

What Is WiseChip Semiconductor's Net Debt?

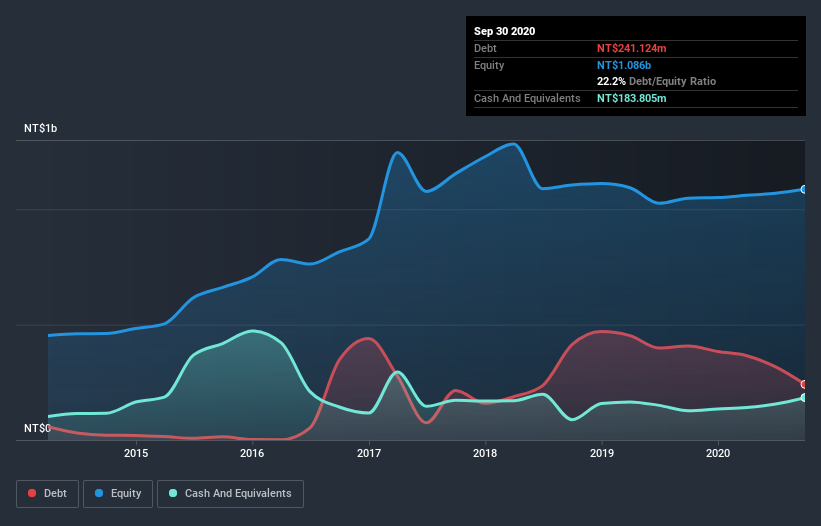

The image below, which you can click on for greater detail, shows that WiseChip Semiconductor had debt of NT$241.1m at the end of September 2020, a reduction from NT$407.0m over a year. However, because it has a cash reserve of NT$183.8m, its net debt is less, at about NT$57.3m.

How Healthy Is WiseChip Semiconductor's Balance Sheet?

The latest balance sheet data shows that WiseChip Semiconductor had liabilities of NT$459.8m due within a year, and liabilities of NT$171.1m falling due after that. On the other hand, it had cash of NT$183.8m and NT$155.9m worth of receivables due within a year. So its liabilities total NT$291.3m more than the combination of its cash and short-term receivables.

Of course, WiseChip Semiconductor has a market capitalization of NT$1.82b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

WiseChip Semiconductor has net debt of just 0.33 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 9.8 times, which is more than adequate. In addition to that, we're happy to report that WiseChip Semiconductor has boosted its EBIT by 81%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But it is WiseChip Semiconductor's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, WiseChip Semiconductor actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Happily, WiseChip Semiconductor's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And that's just the beginning of the good news since its EBIT growth rate is also very heartening. Considering this range of factors, it seems to us that WiseChip Semiconductor is quite prudent with its debt, and the risks seem well managed. So we're not worried about the use of a little leverage on the balance sheet. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that WiseChip Semiconductor is showing 2 warning signs in our investment analysis , and 1 of those is significant...

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading WiseChip Semiconductor or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if WiseChip Semiconductor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:5245

WiseChip Semiconductor

Engages in the research, design, development, manufacture, and sale of organic light emitting diodes (OLEDs) in North America, Europe, Asia, and internationally.

Low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor