Advertisement

- Taiwan

- /

- Real Estate

- /

- TWSE:1437

GTM Holdings' (TWSE:1437) Shareholders Will Receive A Bigger Dividend Than Last Year

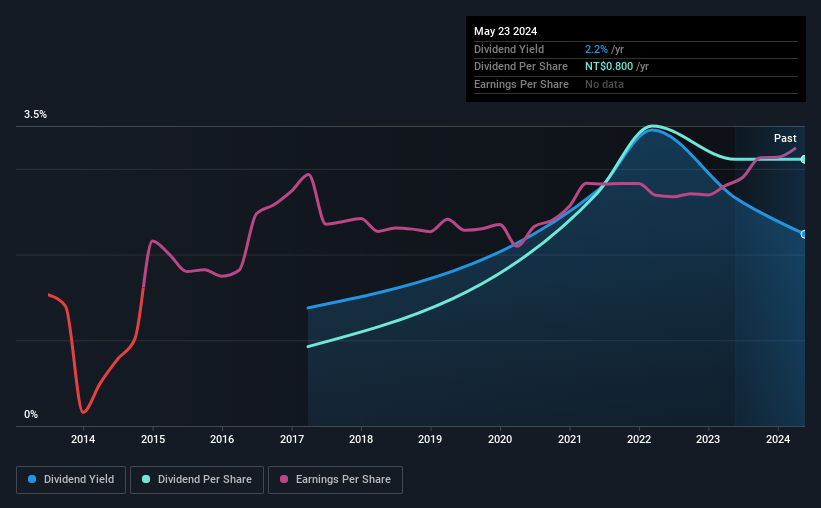

The board of GTM Holdings Corporation (TWSE:1437) has announced that the dividend on 31st of July will be increased to NT$1.13, which will be 41% higher than last year's payment of NT$0.80 which covered the same period. This takes the annual payment to 2.2% of the current stock price, which unfortunately is below what the industry is paying.

View our latest analysis for GTM Holdings

GTM Holdings' Dividend Is Well Covered By Earnings

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. However, GTM Holdings' earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS could expand by 15.3% if recent trends continue. If the dividend continues along recent trends, we estimate the payout ratio will be 46%, which is in the range that makes us comfortable with the sustainability of the dividend.

GTM Holdings Doesn't Have A Long Payment History

The dividend's track record has been pretty solid, but with only 7 years of history we want to see a few more years of history before making any solid conclusions. Since 2017, the dividend has gone from NT$0.238 total annually to NT$0.80. This implies that the company grew its distributions at a yearly rate of about 19% over that duration. The dividend has been growing rapidly, however with such a short payment history we can't know for sure if payment can continue to grow over the long term, so caution may be warranted.

The Dividend Looks Likely To Grow

The company's investors will be pleased to have been receiving dividend income for some time. It's encouraging to see that GTM Holdings has been growing its earnings per share at 15% a year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for GTM Holdings' prospects of growing its dividend payments in the future.

We Really Like GTM Holdings' Dividend

Overall, a dividend increase is always good, and we think that GTM Holdings is a strong income stock thanks to its track record and growing earnings. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 1 warning sign for GTM Holdings that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1437

GTM Holdings

Engages in the real estate, textile, electronic, solar, and investment businesses in Taiwan.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor