Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Lotus Pharmaceutical Co., Ltd. (TWSE:1795) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Lotus Pharmaceutical

What Is Lotus Pharmaceutical's Net Debt?

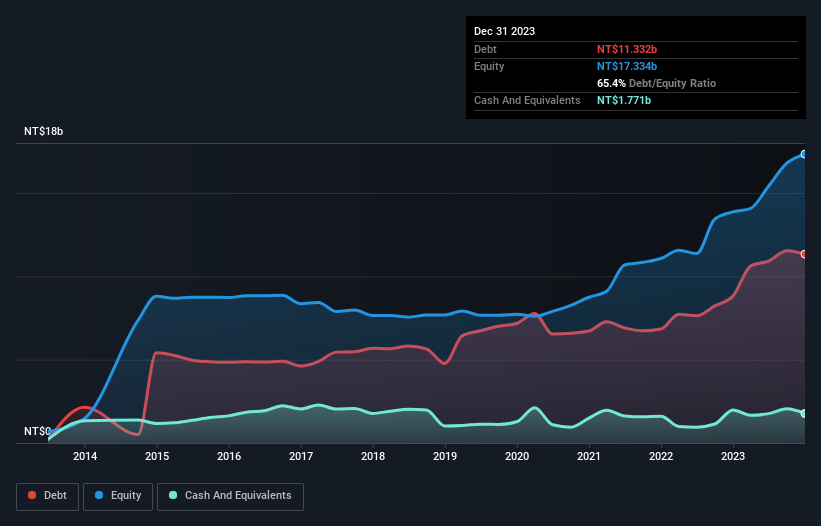

You can click the graphic below for the historical numbers, but it shows that as of December 2023 Lotus Pharmaceutical had NT$11.3b of debt, an increase on NT$8.81b, over one year. However, it also had NT$1.77b in cash, and so its net debt is NT$9.56b.

How Strong Is Lotus Pharmaceutical's Balance Sheet?

The latest balance sheet data shows that Lotus Pharmaceutical had liabilities of NT$4.52b due within a year, and liabilities of NT$11.1b falling due after that. Offsetting these obligations, it had cash of NT$1.77b as well as receivables valued at NT$6.62b due within 12 months. So it has liabilities totalling NT$7.27b more than its cash and near-term receivables, combined.

Given Lotus Pharmaceutical has a market capitalization of NT$84.8b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Lotus Pharmaceutical's net debt to EBITDA ratio of about 1.5 suggests only moderate use of debt. And its strong interest cover of 10.1 times, makes us even more comfortable. Also good is that Lotus Pharmaceutical grew its EBIT at 20% over the last year, further increasing its ability to manage debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Lotus Pharmaceutical's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Lotus Pharmaceutical burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Lotus Pharmaceutical's conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered were considerably better. In particular, we are dazzled with its interest cover. Considering this range of data points, we think Lotus Pharmaceutical is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 2 warning signs we've spotted with Lotus Pharmaceutical .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you're looking to trade Lotus Pharmaceutical, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1795

Lotus Pharmaceutical

Engages in the research and development, manufacture, and sale of generic pharmaceutical products in Taiwan, South Korea, the United States, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives