Advertisement

Chunghwa Chemical Synthesis & Biotech Co., Ltd.'s (TWSE:1762) Business And Shares Still Trailing The Industry

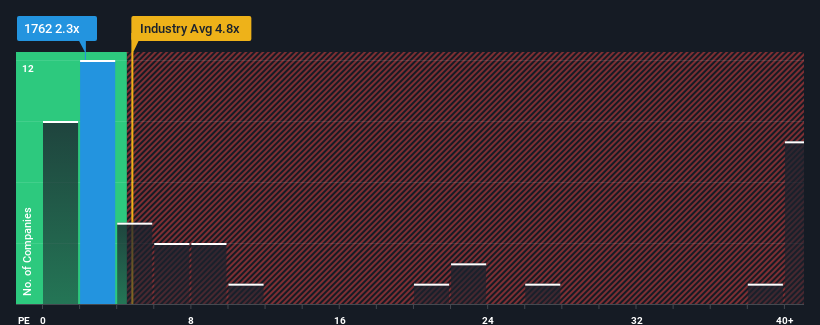

With a price-to-sales (or "P/S") ratio of 2.3x Chunghwa Chemical Synthesis & Biotech Co., Ltd. (TWSE:1762) may be sending very bullish signals at the moment, given that almost half of all the Pharmaceuticals companies in Taiwan have P/S ratios greater than 4.8x and even P/S higher than 23x are not unusual. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Chunghwa Chemical Synthesis & Biotech

How Has Chunghwa Chemical Synthesis & Biotech Performed Recently?

As an illustration, revenue has deteriorated at Chunghwa Chemical Synthesis & Biotech over the last year, which is not ideal at all. One possibility is that the P/S is low because investors think the company won't do enough to avoid underperforming the broader industry in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Chunghwa Chemical Synthesis & Biotech's earnings, revenue and cash flow.How Is Chunghwa Chemical Synthesis & Biotech's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as depressed as Chunghwa Chemical Synthesis & Biotech's is when the company's growth is on track to lag the industry decidedly.

Retrospectively, the last year delivered a frustrating 33% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 5.1% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

In contrast to the company, the rest of the industry is expected to grow by 83% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we understand why Chunghwa Chemical Synthesis & Biotech's P/S is lower than most of its industry peers. However, we think shrinking revenues are unlikely to lead to a stable P/S over the longer term, which could set up shareholders for future disappointment. Even just maintaining these prices could be difficult to achieve as recent revenue trends are already weighing down the shares.

What We Can Learn From Chunghwa Chemical Synthesis & Biotech's P/S?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Chunghwa Chemical Synthesis & Biotech confirms that the company's shrinking revenue over the past medium-term is a key factor in its low price-to-sales ratio, given the industry is projected to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

You should always think about risks. Case in point, we've spotted 1 warning sign for Chunghwa Chemical Synthesis & Biotech you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1762

Chunghwa Chemical Synthesis & Biotech

Chunghwa Chemical Synthesis & Biotech Co., Ltd.

Excellent balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor