Advertisement

We Think InnoPharmax (GTSM:4172) Can Afford To Drive Business Growth

Just because a business does not make any money, does not mean that the stock will go down. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for InnoPharmax (GTSM:4172) shareholders is whether they should be concerned by its rate of cash burn. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

See our latest analysis for InnoPharmax

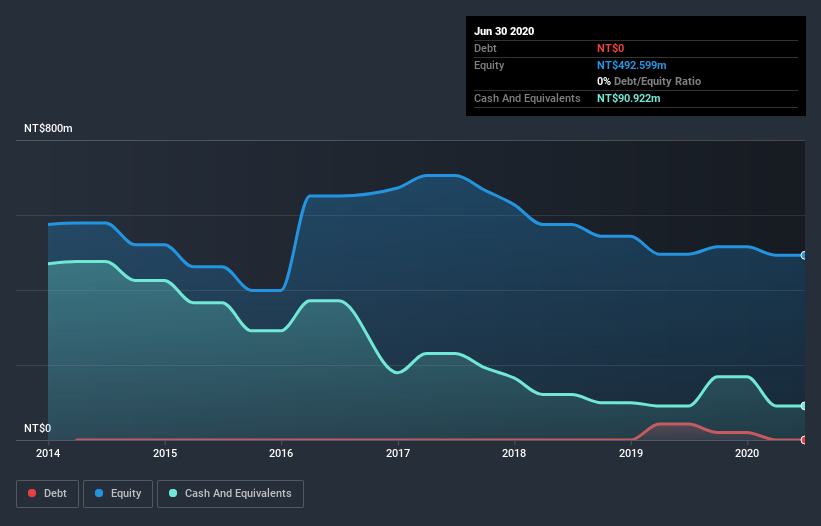

When Might InnoPharmax Run Out Of Money?

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at June 2020, InnoPharmax had cash of NT$91m and no debt. Looking at the last year, the company burnt through NT$41m. That means it had a cash runway of about 2.2 years as of June 2020. Arguably, that's a prudent and sensible length of runway to have. Depicted below, you can see how its cash holdings have changed over time.

How Well Is InnoPharmax Growing?

We reckon the fact that InnoPharmax managed to shrink its cash burn by 46% over the last year is rather encouraging. But it was the operating revenue growth of 155% that really shone. We think it is growing rather well, upon reflection. Of course, we've only taken a quick look at the stock's growth metrics, here. This graph of historic revenue growth shows how InnoPharmax is building its business over time.

How Easily Can InnoPharmax Raise Cash?

While InnoPharmax seems to be in a decent position, we reckon it is still worth thinking about how easily it could raise more cash, if that proved desirable. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

InnoPharmax has a market capitalisation of NT$1.4b and burnt through NT$41m last year, which is 2.8% of the company's market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

How Risky Is InnoPharmax's Cash Burn Situation?

As you can probably tell by now, we're not too worried about InnoPharmax's cash burn. In particular, we think its revenue growth stands out as evidence that the company is well on top of its spending. And even its cash burn reduction was very encouraging. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. Its important for readers to be cognizant of the risks that can affect the company's operations, and we've picked out 4 warning signs for InnoPharmax that investors should know when investing in the stock.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

If you decide to trade InnoPharmax, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:4172

InnoPharmax

A specialty pharmaceutical company, develops and commercializes products for the treatment of oncology and other specialties in Taiwan.

Flawless balance sheet slight.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor