Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Medigen Biotechnology Corp. (GTSM:3176) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Medigen Biotechnology

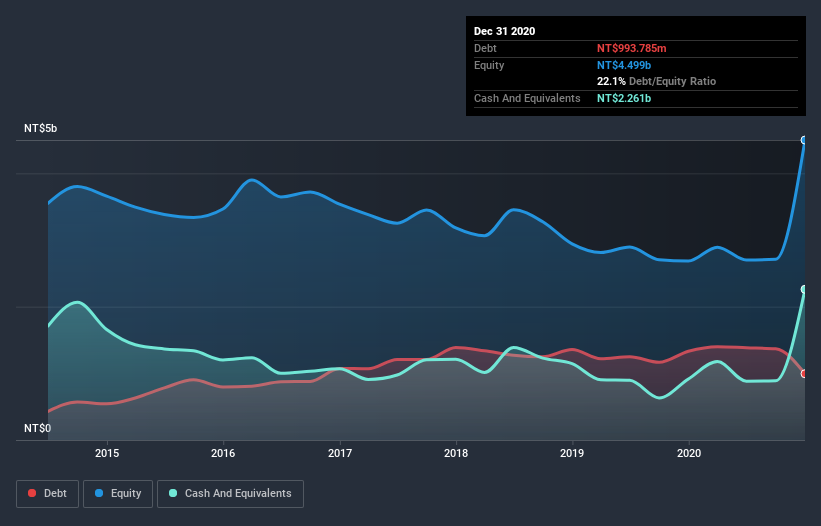

What Is Medigen Biotechnology's Net Debt?

The image below, which you can click on for greater detail, shows that Medigen Biotechnology had debt of NT$993.8m at the end of December 2020, a reduction from NT$1.33b over a year. But it also has NT$2.26b in cash to offset that, meaning it has NT$1.27b net cash.

How Strong Is Medigen Biotechnology's Balance Sheet?

According to the last reported balance sheet, Medigen Biotechnology had liabilities of NT$933.8m due within 12 months, and liabilities of NT$719.2m due beyond 12 months. Offsetting this, it had NT$2.26b in cash and NT$281.7m in receivables that were due within 12 months. So it actually has NT$889.5m more liquid assets than total liabilities.

This short term liquidity is a sign that Medigen Biotechnology could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Medigen Biotechnology has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Medigen Biotechnology will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Medigen Biotechnology reported revenue of NT$616m, which is a gain of 11%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Medigen Biotechnology?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Medigen Biotechnology had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of NT$828m and booked a NT$338m accounting loss. But at least it has NT$1.27b on the balance sheet to spend on growth, near-term. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Medigen Biotechnology has 1 warning sign we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Medigen Biotechnology, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:3176

Medigen Biotechnology

A biopharmaceutical company, engages in the research and development of new drugs and vaccines, cytotherapy, advanced nucleic acid testing, generic drugs, aesthetic medicine, and vaccine-related products in Taiwan.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor