Advertisement

- Taiwan

- /

- Metals and Mining

- /

- TWSE:2031

Investors Don't See Light At End Of Hsin Kuang Steel Company Limited's (TWSE:2031) Tunnel

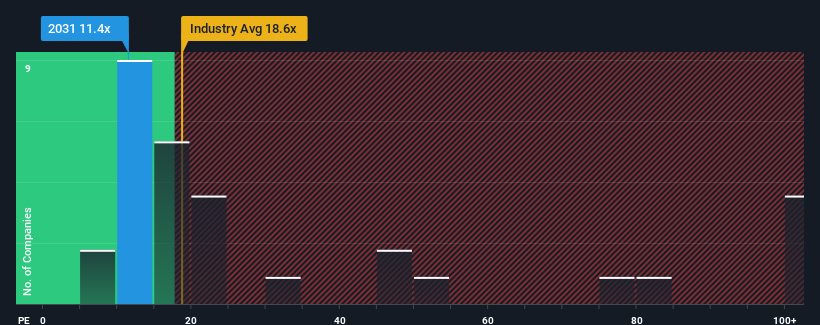

With a price-to-earnings (or "P/E") ratio of 11.4x Hsin Kuang Steel Company Limited (TWSE:2031) may be sending very bullish signals at the moment, given that almost half of all companies in Taiwan have P/E ratios greater than 23x and even P/E's higher than 41x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Recent times have been pleasing for Hsin Kuang Steel as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Hsin Kuang Steel

Is There Any Growth For Hsin Kuang Steel?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Hsin Kuang Steel's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 247%. The latest three year period has also seen a 20% overall rise in EPS, aided extensively by its short-term performance. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Turning to the outlook, the next year should bring diminished returns, with earnings decreasing 3.8% as estimated by the two analysts watching the company. Meanwhile, the broader market is forecast to expand by 23%, which paints a poor picture.

In light of this, it's understandable that Hsin Kuang Steel's P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Hsin Kuang Steel's P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Hsin Kuang Steel's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

You need to take note of risks, for example - Hsin Kuang Steel has 3 warning signs (and 2 which are potentially serious) we think you should know about.

You might be able to find a better investment than Hsin Kuang Steel. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Hsin Kuang Steel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2031

Hsin Kuang Steel

Engages in the cutting, stamping, and sale of various steel products in Taiwan.

Good value average dividend payer.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor