Need To Know: Analysts Just Made A Substantial Cut To Their Nan Ya Plastics Corporation (TWSE:1303) Estimates

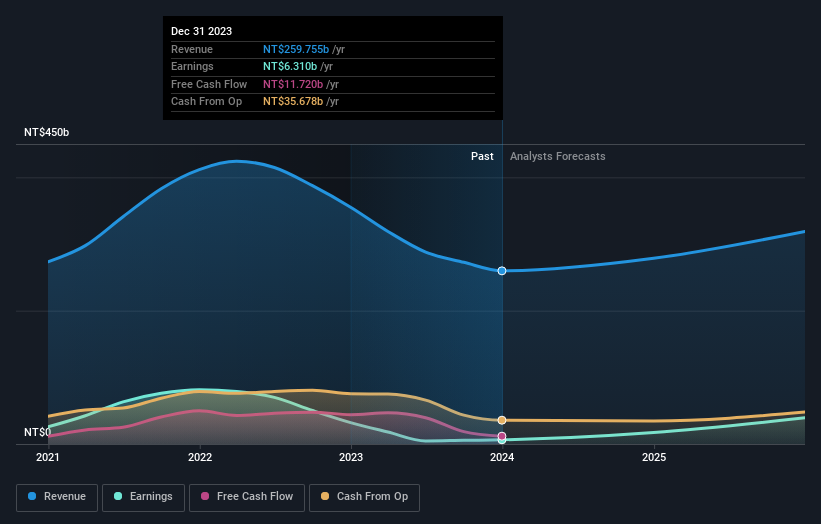

The latest analyst coverage could presage a bad day for Nan Ya Plastics Corporation (TWSE:1303), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

Following the downgrade, the latest consensus from Nan Ya Plastics' seven analysts is for revenues of NT$271b in 2024, which would reflect a credible 4.5% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to surge 169% to NT$2.14. Before this latest update, the analysts had been forecasting revenues of NT$314b and earnings per share (EPS) of NT$2.50 in 2024. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a considerable drop in earnings per share numbers as well.

See our latest analysis for Nan Ya Plastics

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The analysts are definitely expecting Nan Ya Plastics' growth to accelerate, with the forecast 4.5% annualised growth to the end of 2024 ranking favourably alongside historical growth of 2.0% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 7.5% per year. So it's clear that despite the acceleration in growth, Nan Ya Plastics is expected to grow meaningfully slower than the industry average.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Nan Ya Plastics' revenues are expected to grow slower than the wider market. After a cut like that, investors could be forgiven for thinking analysts are a lot more bearish on Nan Ya Plastics, and a few readers might choose to steer clear of the stock.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with Nan Ya Plastics, including the risk of cutting its dividend. Learn more, and discover the 1 other flag we've identified, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you're looking to trade Nan Ya Plastics, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nan Ya Plastics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1303

Nan Ya Plastics

Engages in the manufacture and sale of plastic products, polyester fibers, petrochemical products, and electronic materials in Taiwan, China and Hong Kong, the United States, and internationally.

Fair value with moderate growth potential.