Advertisement

Is Cathay Chemical Works Inc. (TPE:1713) A Good Dividend Stock?

Could Cathay Chemical Works Inc. (TPE:1713) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. If you are hoping to live on the income from dividends, it's important to be a lot more stringent with your investments than the average punter.

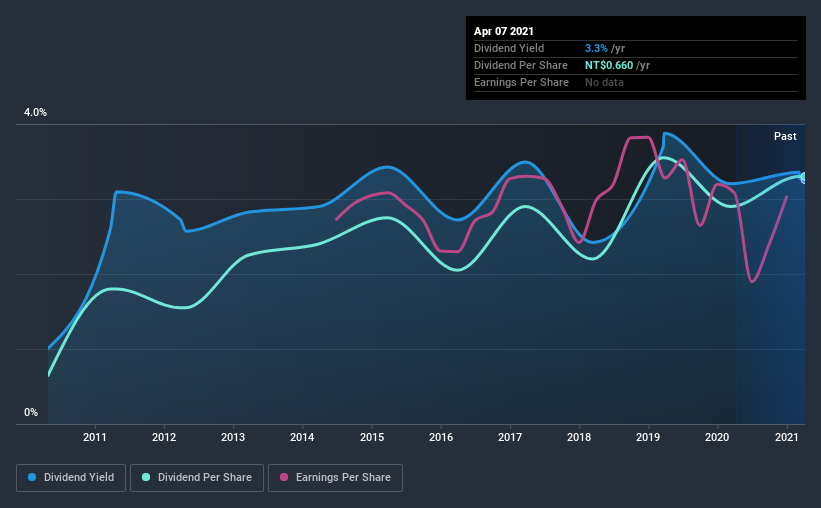

With Cathay Chemical Works yielding 3.3% and having paid a dividend for over 10 years, many investors likely find the company quite interesting. It would not be a surprise to discover that many investors buy it for the dividends. Some simple analysis can offer a lot of insights when buying a company for its dividend, and we'll go through this below.

Explore this interactive chart for our latest analysis on Cathay Chemical Works!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. In the last year, Cathay Chemical Works paid out 109% of its profit as dividends. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. With a cash payout ratio of 192%, Cathay Chemical Works' dividend payments are poorly covered by cash flow. Paying out such a high percentage of cash flow suggests that the dividend was funded from either cash at bank or by borrowing, neither of which is desirable over the long term. As Cathay Chemical Works' dividend was not well covered by either earnings or cash flow, we would be concerned that this dividend could be at risk over the long term.

With a strong net cash balance, Cathay Chemical Works investors may not have much to worry about in the near term from a dividend perspective.

Remember, you can always get a snapshot of Cathay Chemical Works' latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

One of the major risks of relying on dividend income, is the potential for a company to struggle financially and cut its dividend. Not only is your income cut, but the value of your investment declines as well - nasty. Cathay Chemical Works has been paying dividends for a long time, but for the purpose of this analysis, we only examine the past 10 years of payments. Its dividend payments have declined on at least one occasion over the past 10 years. During the past 10-year period, the first annual payment was NT$0.1 in 2011, compared to NT$0.7 last year. This works out to be a compound annual growth rate (CAGR) of approximately 18% a year over that time. The growth in dividends has not been linear, but the CAGR is a decent approximation of the rate of change over this time frame.

It's not great to see that the payment has been cut in the past. We're generally more wary of companies that have cut their dividend before, as they tend to perform worse in an economic downturn.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share (EPS) are growing. Why take the risk of a dividend getting cut, unless there's a good chance of bigger dividends in future? Earnings have grown at around 5.6% a year for the past five years, which is better than seeing them shrink! Although per-share earnings are growing at a credible rate, virtually all of the income is being paid out as dividends to shareholders. This is okay, but may limit growth in the company's future dividend payments.

Conclusion

To summarise, shareholders should always check that Cathay Chemical Works' dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. It's a concern to see that the company paid out such a high percentage of its earnings and cashflow as dividends. Second, earnings growth has been ordinary, and its history of dividend payments is chequered - having cut its dividend at least once in the past. There are a few too many issues for us to get comfortable with Cathay Chemical Works from a dividend perspective. Businesses can change, but we would struggle to identify why an investor should rely on this stock for their income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 1 warning sign for Cathay Chemical Works that you should be aware of before investing.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

When trading Cathay Chemical Works or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1713

Cathay Chemical Works

Manufactures and sells specialty and fine chemicals under the CATHAY brand in Taiwan.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|35.6% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|35.2% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|30.0% undervalued

EV

Community Contributor