The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Taiwan Wax Company,Ltd. (GTSM:1742) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Taiwan Wax CompanyLtd

What Is Taiwan Wax CompanyLtd's Debt?

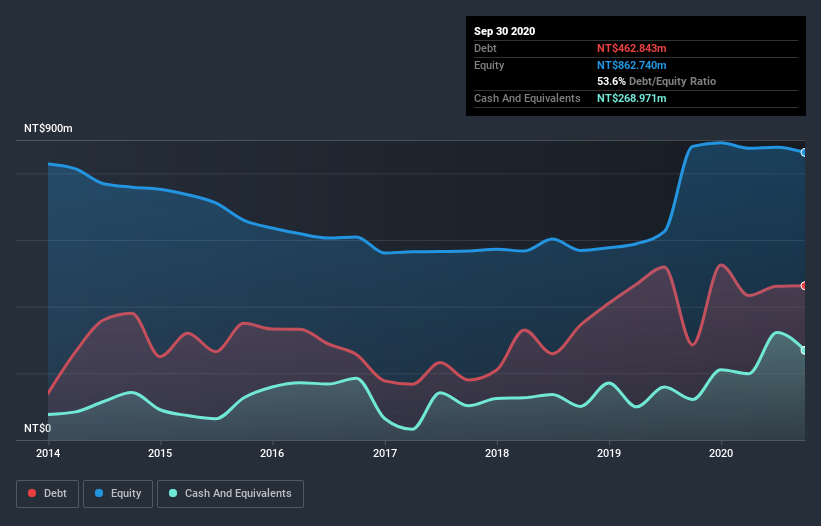

As you can see below, at the end of September 2020, Taiwan Wax CompanyLtd had NT$462.8m of debt, up from NT$285.4m a year ago. Click the image for more detail. However, it does have NT$269.0m in cash offsetting this, leading to net debt of about NT$193.9m.

How Healthy Is Taiwan Wax CompanyLtd's Balance Sheet?

The latest balance sheet data shows that Taiwan Wax CompanyLtd had liabilities of NT$400.3m due within a year, and liabilities of NT$130.2m falling due after that. On the other hand, it had cash of NT$269.0m and NT$244.2m worth of receivables due within a year. So its liabilities total NT$17.4m more than the combination of its cash and short-term receivables.

This state of affairs indicates that Taiwan Wax CompanyLtd's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the NT$1.44b company is short on cash, but still worth keeping an eye on the balance sheet.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Taiwan Wax CompanyLtd's debt to EBITDA ratio of 5.4 suggests a heavy debt load, its interest coverage of 7.9 implies it services that debt with ease. Overall we'd say it seems likely the company is carrying a fairly heavy swag of debt. Importantly, Taiwan Wax CompanyLtd's EBIT fell a jaw-dropping 33% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Taiwan Wax CompanyLtd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last two years, Taiwan Wax CompanyLtd saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Taiwan Wax CompanyLtd's conversion of EBIT to free cash flow and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But at least it's pretty decent at covering its interest expense with its EBIT; that's encouraging. Overall, we think it's fair to say that Taiwan Wax CompanyLtd has enough debt that there are some real risks around the balance sheet. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 4 warning signs we've spotted with Taiwan Wax CompanyLtd .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade Taiwan Wax CompanyLtd, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Taiwan Wax CompanyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:1742

Taiwan Wax CompanyLtd

Manufactures and sells refined wax and finished product in Taiwan and internationally.

Excellent balance sheet and slightly overvalued.