Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Chia Her Industrial Co., Ltd. (TWSE:1449) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Chia Her Industrial

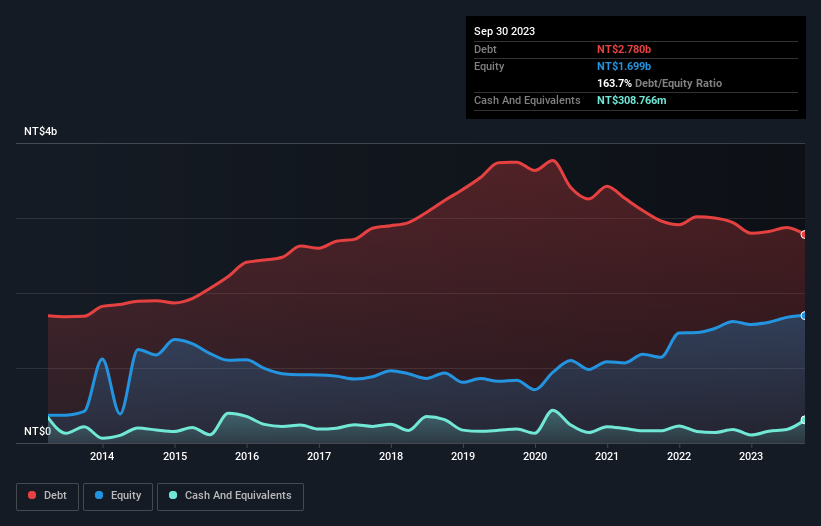

What Is Chia Her Industrial's Net Debt?

You can click the graphic below for the historical numbers, but it shows that Chia Her Industrial had NT$2.78b of debt in September 2023, down from NT$2.94b, one year before. On the flip side, it has NT$308.8m in cash leading to net debt of about NT$2.47b.

A Look At Chia Her Industrial's Liabilities

According to the last reported balance sheet, Chia Her Industrial had liabilities of NT$2.03b due within 12 months, and liabilities of NT$2.34b due beyond 12 months. On the other hand, it had cash of NT$308.8m and NT$186.8m worth of receivables due within a year. So its liabilities total NT$3.88b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the NT$1.65b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Chia Her Industrial would probably need a major re-capitalization if its creditors were to demand repayment. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Chia Her Industrial will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Chia Her Industrial had a loss before interest and tax, and actually shrunk its revenue by 2.3%, to NT$2.5b. We would much prefer see growth.

Caveat Emptor

Importantly, Chia Her Industrial had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost NT$13m at the EBIT level. When we look at that alongside the significant liabilities, we're not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. But on the bright side the company actually produced a statutory profit of NT$44m and free cash flow of NT$182m. So there is definitely a chance that it can improve things in the next few years. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Chia Her Industrial is showing 6 warning signs in our investment analysis , and 1 of those is significant...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1449

Proven track record slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor