Further Upside For Sunspring Metal Corporation (TWSE:2062) Shares Could Introduce Price Risks After 35% Bounce

Sunspring Metal Corporation (TWSE:2062) shareholders would be excited to see that the share price has had a great month, posting a 35% gain and recovering from prior weakness. Looking back a bit further, it's encouraging to see the stock is up 75% in the last year.

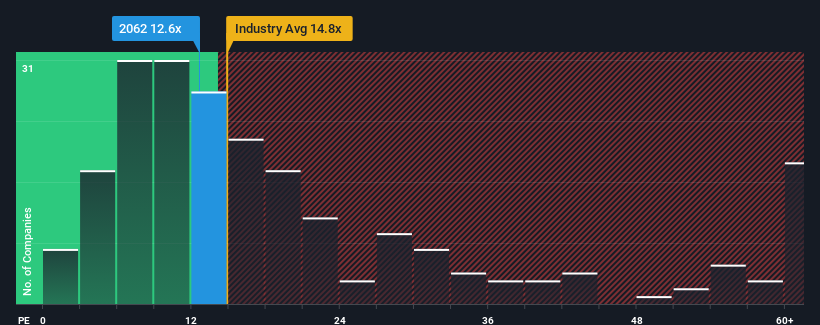

Although its price has surged higher, Sunspring Metal may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 12.6x, since almost half of all companies in Taiwan have P/E ratios greater than 22x and even P/E's higher than 40x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Sunspring Metal certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Sunspring Metal

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Sunspring Metal's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 92% gain to the company's bottom line. The latest three year period has also seen an excellent 78% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

It's interesting to note that the rest of the market is similarly expected to grow by 23% over the next year, which is fairly even with the company's recent medium-term annualised growth rates.

In light of this, it's peculiar that Sunspring Metal's P/E sits below the majority of other companies. Apparently some shareholders are more bearish than recent times would indicate and have been accepting lower selling prices.

The Key Takeaway

The latest share price surge wasn't enough to lift Sunspring Metal's P/E close to the market median. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Sunspring Metal revealed its three-year earnings trends aren't contributing to its P/E as much as we would have predicted, given they look similar to current market expectations. When we see average earnings with market-like growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions should normally provide more support to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Sunspring Metal that you need to be mindful of.

Of course, you might also be able to find a better stock than Sunspring Metal. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2062

Sunspring Metal

Manufactures, processes, and trades water pipe switch accessories, gate valves, corks, copper pipe fittings, and waterway sanitary equipment in Taiwan and internationally.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Community Narratives