- Taiwan

- /

- Electrical

- /

- TWSE:1519

Fortune Electric Co., Ltd.'s (TWSE:1519) Share Price Is Still Matching Investor Opinion Despite 29% Slump

Fortune Electric Co., Ltd. (TWSE:1519) shares have had a horrible month, losing 29% after a relatively good period beforehand. The good news is that in the last year, the stock has shone bright like a diamond, gaining 216%.

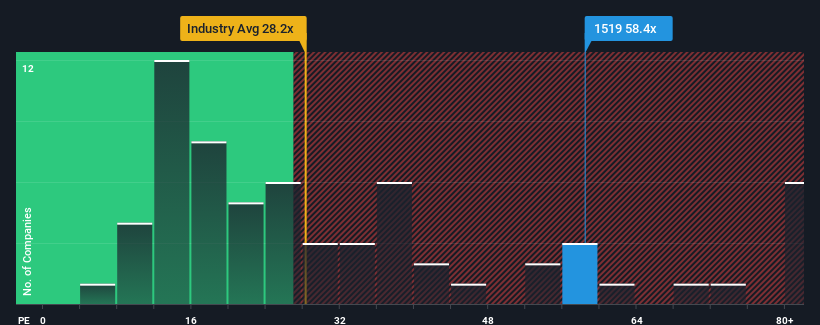

Even after such a large drop in price, Fortune Electric may still be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 58.4x, since almost half of all companies in Taiwan have P/E ratios under 22x and even P/E's lower than 15x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Fortune Electric has been doing quite well of late. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

Check out our latest analysis for Fortune Electric

How Is Fortune Electric's Growth Trending?

In order to justify its P/E ratio, Fortune Electric would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings growth, the company posted a terrific increase of 182%. The strong recent performance means it was also able to grow EPS by 542% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 65% over the next year. With the market only predicted to deliver 23%, the company is positioned for a stronger earnings result.

With this information, we can see why Fortune Electric is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Fortune Electric's P/E

Fortune Electric's shares may have retreated, but its P/E is still flying high. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Fortune Electric maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 1 warning sign for Fortune Electric that you should be aware of.

If these risks are making you reconsider your opinion on Fortune Electric, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1519

Fortune Electric

Manufactures, processes, and sells transformers, inverters, power distribution boards, and high-low voltage switches in Taiwan and internationally.

Exceptional growth potential with outstanding track record.

Similar Companies

Market Insights

Community Narratives