Advertisement

- Taiwan

- /

- Electrical

- /

- TWSE:1513

There May Be Reason For Hope In Chung-Hsin Electric and Machinery Manufacturing's (TWSE:1513) Disappointing Earnings

Shareholders appeared unconcerned with Chung-Hsin Electric and Machinery Manufacturing Corp.'s (TWSE:1513) lackluster earnings report last week. We did some digging, and we believe the earnings are stronger than they seem.

Check out our latest analysis for Chung-Hsin Electric and Machinery Manufacturing

Examining Cashflow Against Chung-Hsin Electric and Machinery Manufacturing's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

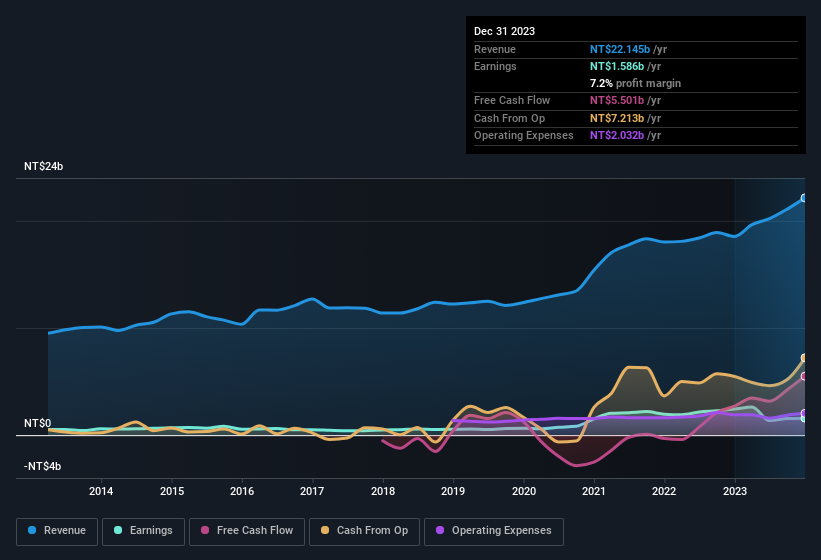

For the year to December 2023, Chung-Hsin Electric and Machinery Manufacturing had an accrual ratio of -0.17. Therefore, its statutory earnings were very significantly less than its free cashflow. Indeed, in the last twelve months it reported free cash flow of NT$5.5b, well over the NT$1.59b it reported in profit. Chung-Hsin Electric and Machinery Manufacturing shareholders are no doubt pleased that free cash flow improved over the last twelve months. Unfortunately for shareholders, the company has also been issuing new shares, diluting their share of future earnings.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. Chung-Hsin Electric and Machinery Manufacturing expanded the number of shares on issue by 8.1% over the last year. As a result, its net income is now split between a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Chung-Hsin Electric and Machinery Manufacturing's historical EPS growth by clicking on this link.

A Look At The Impact Of Chung-Hsin Electric and Machinery Manufacturing's Dilution On Its Earnings Per Share (EPS)

Chung-Hsin Electric and Machinery Manufacturing has improved its profit over the last three years, with an annualized gain of 3.8% in that time. But on the other hand, earnings per share actually fell by 9.7% per year. Net income was down 35% over the last twelve months. Unfortunately for shareholders, though, the earnings per share result was even worse, declining 38%. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, if Chung-Hsin Electric and Machinery Manufacturing's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Chung-Hsin Electric and Machinery Manufacturing's Profit Performance

In conclusion, Chung-Hsin Electric and Machinery Manufacturing has a strong cashflow relative to earnings, which indicates good quality earnings, but the dilution means its earnings per share are dropping faster than its profit. Considering all the aforementioned, we'd venture that Chung-Hsin Electric and Machinery Manufacturing's profit result is a pretty good guide to its true profitability, albeit a bit on the conservative side. If you want to do dive deeper into Chung-Hsin Electric and Machinery Manufacturing, you'd also look into what risks it is currently facing. While conducting our analysis, we found that Chung-Hsin Electric and Machinery Manufacturing has 5 warning signs and it would be unwise to ignore them.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1513

Chung-Hsin Electric and Machinery Manufacturing

Chung-Hsin Electric and Machinery Manufacturing Corp.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor