Advertisement

- Taiwan

- /

- Electrical

- /

- TWSE:3296

Here's Why Powertech Industrial (TPE:3296) Can Manage Its Debt Responsibly

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Powertech Industrial Co., Ltd. (TPE:3296) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Powertech Industrial

What Is Powertech Industrial's Net Debt?

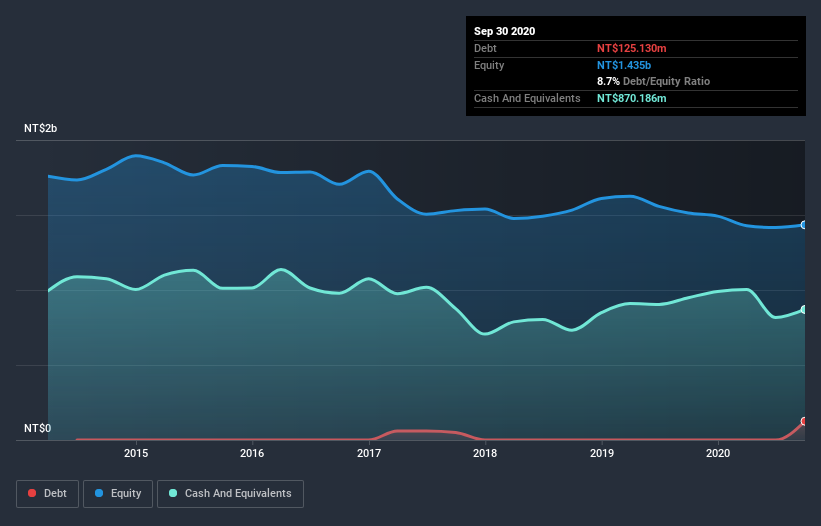

The image below, which you can click on for greater detail, shows that at September 2020 Powertech Industrial had debt of NT$125.1m, up from none in one year. However, it does have NT$870.2m in cash offsetting this, leading to net cash of NT$745.1m.

A Look At Powertech Industrial's Liabilities

We can see from the most recent balance sheet that Powertech Industrial had liabilities of NT$813.9m falling due within a year, and liabilities of NT$77.7m due beyond that. Offsetting these obligations, it had cash of NT$870.2m as well as receivables valued at NT$750.2m due within 12 months. So it actually has NT$728.7m more liquid assets than total liabilities.

This excess liquidity is a great indication that Powertech Industrial's balance sheet is almost as strong as Fort Knox. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that Powertech Industrial has more cash than debt is arguably a good indication that it can manage its debt safely.

The modesty of its debt load may become crucial for Powertech Industrial if management cannot prevent a repeat of the 80% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Powertech Industrial will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Powertech Industrial has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Powertech Industrial produced sturdy free cash flow equating to 79% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While it is always sensible to investigate a company's debt, in this case Powertech Industrial has NT$745.1m in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of -NT$149m, being 79% of its EBIT. So is Powertech Industrial's debt a risk? It doesn't seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 5 warning signs for Powertech Industrial (2 can't be ignored) you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Powertech Industrial or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:3296

Powertech Industrial

Powertech Industrial Co., Ltd., together with its subsidiaries, manufacture and sell electronic circuit power protection and smart home wireless remote control devices, wired and wireless communication equipment, and electronic modules and parts.

Excellent balance sheet low.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor