- Taiwan

- /

- Electrical

- /

- TWSE:3003

Can Mixed Fundamentals Have A Negative Impact on K.S. Terminals Inc. (TPE:3003) Current Share Price Momentum?

Most readers would already be aware that K.S. Terminals' (TPE:3003) stock increased significantly by 23% over the past three months. But the company's key financial indicators appear to be differing across the board and that makes us question whether or not the company's current share price momentum can be maintained. In this article, we decided to focus on K.S. Terminals' ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for K.S. Terminals

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for K.S. Terminals is:

7.7% = NT$366m ÷ NT$4.7b (Based on the trailing twelve months to September 2020).

The 'return' is the income the business earned over the last year. That means that for every NT$1 worth of shareholders' equity, the company generated NT$0.08 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

K.S. Terminals' Earnings Growth And 7.7% ROE

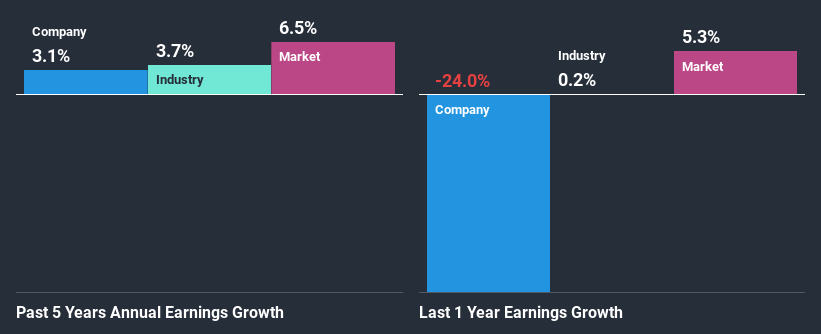

On the face of it, K.S. Terminals' ROE is not much to talk about. However, given that the company's ROE is similar to the average industry ROE of 8.1%, we may spare it some thought. Having said that, K.S. Terminals has shown a meagre net income growth of 3.1% over the past five years. Bear in mind, the company's ROE is not very high . So this could also be one of the reasons behind the company's low growth in earnings.

As a next step, we compared K.S. Terminals' net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 3.7% in the same period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is K.S. Terminals fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is K.S. Terminals Using Its Retained Earnings Effectively?

With a high three-year median payout ratio of 56% (or a retention ratio of 44%), most of K.S. Terminals' profits are being paid to shareholders. This definitely contributes to the low earnings growth seen by the company.

Additionally, K.S. Terminals has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to drop to 42% over the next three years. As a result, the expected drop in K.S. Terminals' payout ratio explains the anticipated rise in the company's future ROE to 12%, over the same period.

Conclusion

Overall, we have mixed feelings about K.S. Terminals. While no doubt its earnings growth is pretty respectable, the low profit retention could mean that the company's earnings growth could have been higher, had it been paying reinvesting a higher portion of its profits. An improvement in its ROE could also help future earnings growth. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

If you’re looking to trade K.S. Terminals, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if K.S. Terminals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:3003

K.S. Terminals

Manufactures and sells electrical terminals, automotive connectors, battery modular connectors, and EV charging connectors in Taiwan and internationally.

Flawless balance sheet second-rate dividend payer.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion