- Taiwan

- /

- Trade Distributors

- /

- TPEX:6728

Is There More To The Story Than Up Young Cornerstone's (GTSM:6728) Earnings Growth?

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. In this article, we'll look at how useful this year's statutory profit is, when analysing Up Young Cornerstone (GTSM:6728).

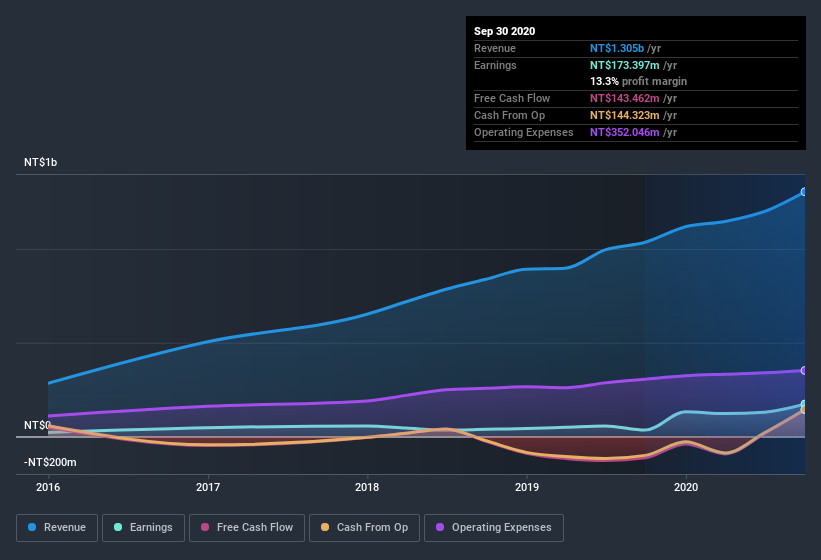

It's good to see that over the last twelve months Up Young Cornerstone made a profit of NT$173.4m on revenue of NT$1.31b. In the chart below, you can see that its profit and revenue have both grown over the last three years.

View our latest analysis for Up Young Cornerstone

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. Therefore, today we will consider the nature of Up Young Cornerstone's statutory earnings with reference to its dilution of shareholders and the impact of unusual items. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Up Young Cornerstone.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, Up Young Cornerstone increased the number of shares on issue by 10.0% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out Up Young Cornerstone's historical EPS growth by clicking on this link.

A Look At The Impact Of Up Young Cornerstone's Dilution on Its Earnings Per Share (EPS).

As you can see above, Up Young Cornerstone has been growing its net income over the last few years, with an annualized gain of 223% over three years. In comparison, earnings per share only gained 204% over the same period. And at a glance the 392% gain in profit over the last year impresses. On the other hand, earnings per share are only up 362% in that time. So you can see that the dilution has had a bit of an impact on shareholders. Therefore, the dilution is having a noteworthy influence on shareholder returns. And so, you can see quite clearly that dilution is influencing shareholder earnings.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So Up Young Cornerstone shareholders will want to see that EPS figure continue to increase. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

The Impact Of Unusual Items On Profit

Finally, we should also consider the fact that unusual items boosted Up Young Cornerstone's net profit by NT$90m over the last year. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. We can see that Up Young Cornerstone's positive unusual items were quite significant relative to its profit in the year to September 2020. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Up Young Cornerstone's Profit Performance

In its last report Up Young Cornerstone benefitted from unusual items which boosted its profit, which could make the profit seem better than it really is on a sustainable basis. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. Considering all this we'd argue Up Young Cornerstone's profits probably give an overly generous impression of its sustainable level of profitability. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example, we've discovered 6 warning signs that you should run your eye over to get a better picture of Up Young Cornerstone.

Our examination of Up Young Cornerstone has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade Up Young Cornerstone, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:6728

Up Young Cornerstone

Engages in the sale of commercial washing and drying machines.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives