- Canada

- /

- Oil and Gas

- /

- TSX:TOU

Discover 3 Stocks Including Enerjisa Enerji That Investors May Be Undervaluing

Reviewed by Simply Wall St

In recent weeks, global markets have been influenced by rising U.S. Treasury yields, which have exerted pressure on equities and adjusted expectations for monetary policy easing. As investors navigate these shifting conditions, identifying undervalued stocks can offer potential opportunities for growth amidst broader market volatility. Understanding the intrinsic value of a stock compared to its current market price is crucial in this environment, as it may reveal investment potentials that are not immediately apparent in more stable periods.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Beyout Investment Group Holding Company - K.S.C. (Holding) (KWSE:BEYOUT) | KWD0.395 | KWD0.79 | 49.9% |

| Acerinox (BME:ACX) | €8.52 | €16.98 | 49.8% |

| Enento Group Oyj (HLSE:ENENTO) | €18.40 | €36.57 | 49.7% |

| North Electro-OpticLtd (SHSE:600184) | CN¥11.52 | CN¥22.89 | 49.7% |

| WEX (NYSE:WEX) | US$172.60 | US$343.98 | 49.8% |

| Semiconductor Manufacturing International (SEHK:981) | HK$27.05 | HK$53.78 | 49.7% |

| SBI Sumishin Net Bank (TSE:7163) | ¥2706.00 | ¥5411.18 | 50% |

| Energy One (ASX:EOL) | A$5.53 | A$11.06 | 50% |

| Fine Foods & Pharmaceuticals N.T.M (BIT:FF) | €8.36 | €16.70 | 49.9% |

| Sinch (OM:SINCH) | SEK31.45 | SEK62.48 | 49.7% |

Let's review some notable picks from our screened stocks.

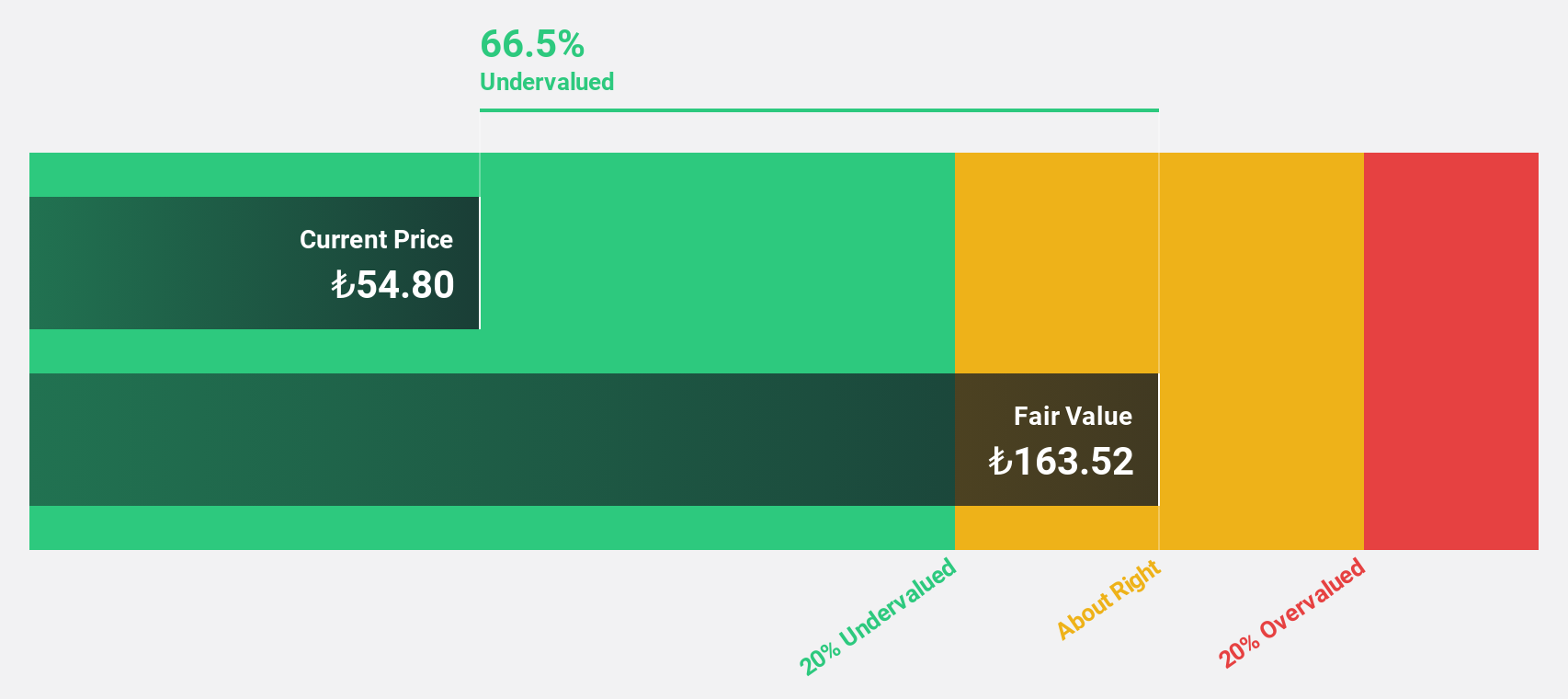

Enerjisa Enerji (IBSE:ENJSA)

Overview: Enerjisa Enerji A.S. operates in Turkey through its subsidiaries, focusing on electricity distribution, retail sales, and customer solutions, with a market cap of TRY67.32 billion.

Operations: The company's revenue segments include Retail at TRY72.31 billion, Customer Solutions at TRY4.72 billion, and Distribution/Retail at TRY60.21 billion.

Estimated Discount To Fair Value: 36.8%

Enerjisa Enerji is trading at TRY57, significantly below its estimated fair value of TRY90.22, highlighting potential undervaluation based on discounted cash flow analysis. Despite a forecasted significant earnings growth of 91.9% annually over the next three years, recent financials show a decline in net income and sales compared to last year. Interest payments are not well covered by earnings, and its dividend yield of 4.89% is unsustainable with current cash flows.

- Our growth report here indicates Enerjisa Enerji may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of Enerjisa Enerji.

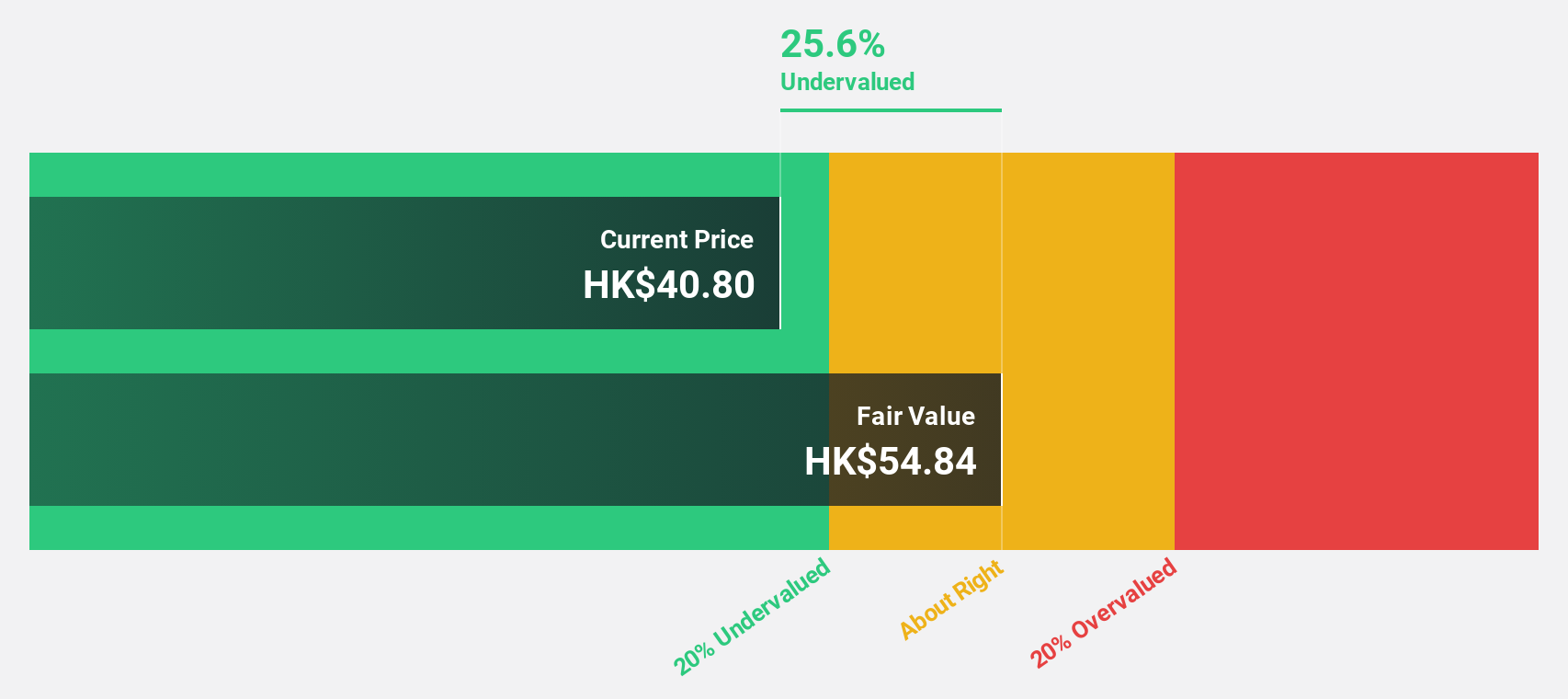

AAC Technologies Holdings (SEHK:2018)

Overview: AAC Technologies Holdings Inc. is an investment holding company that offers solutions for smart devices across various regions including Mainland China, Hong Kong SAR, Taiwan, other Asian countries, the United States, and Europe, with a market cap of approximately HK$37.99 billion.

Operations: The company generates revenue from several segments, including CN¥4.07 billion from Optics Products, CN¥7.64 billion from Acoustics Products, CN¥0.92 billion from Sensor and Semiconductor Products, and CN¥8.28 billion from Electromagnetic Drives and Precision Mechanics.

Estimated Discount To Fair Value: 10.7%

AAC Technologies Holdings is trading at HK$31.45, below its estimated fair value of HK$35.21, indicating potential undervaluation based on cash flows. Earnings grew 81.3% last year and are expected to grow significantly at 20.98% annually over the next three years, outpacing Hong Kong market averages. Recent financials show a strong performance with net income rising to CNY 537 million from CNY 150 million year-on-year for H1 2024, supporting robust cash flow prospects.

- In light of our recent growth report, it seems possible that AAC Technologies Holdings' financial performance will exceed current levels.

- Take a closer look at AAC Technologies Holdings' balance sheet health here in our report.

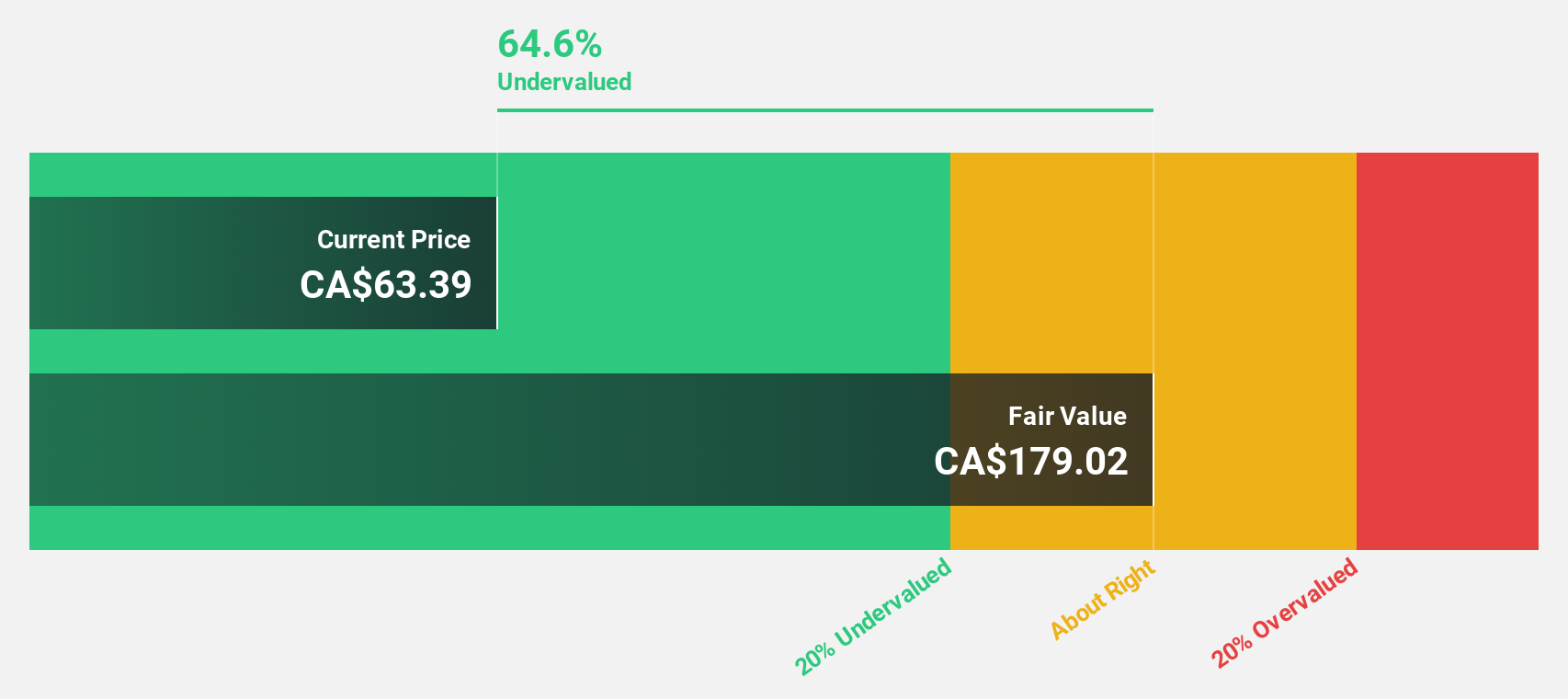

Tourmaline Oil (TSX:TOU)

Overview: Tourmaline Oil Corp. engages in the exploration and development of oil and natural gas properties in the Western Canadian Sedimentary Basin, with a market cap of CA$23.93 billion.

Operations: The company's revenue is primarily derived from petroleum and natural gas properties, totaling CA$4.80 billion.

Estimated Discount To Fair Value: 45.6%

Tourmaline Oil, trading at CA$65.78, is significantly undervalued compared to its fair value estimate of CA$120.95. Earnings are projected to grow 42.3% annually, outpacing the Canadian market's 16.1%. Despite recent insider selling and shareholder dilution, strategic expansions into compressed natural gas infrastructure support long-term growth prospects. However, profit margins have decreased from last year and dividends remain inadequately covered by free cash flows, highlighting potential financial constraints amidst expansion efforts.

- Our expertly prepared growth report on Tourmaline Oil implies its future financial outlook may be stronger than recent results.

- Click here and access our complete balance sheet health report to understand the dynamics of Tourmaline Oil.

Summing It All Up

- Explore the 958 names from our Undervalued Stocks Based On Cash Flows screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tourmaline Oil might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TOU

Tourmaline Oil

Explores for and develops oil and natural gas properties in the Western Canadian Sedimentary Basin.

High growth potential with solid track record.