Advertisement

- Thailand

- /

- Specialty Stores

- /

- SET:HMPRO

Top Asian Dividend Stocks To Consider In March 2025

Simply Wall St

Reviewed by Simply Wall St

Amid heightened uncertainty in global markets, Asian indices have shown mixed performances, with Japan's stock markets rising and China's experiencing a downturn. As investors navigate these fluctuations, dividend stocks in Asia stand out as potential opportunities for those seeking steady income streams amidst economic uncertainties.

Top 10 Dividend Stocks In Asia

| Name | Dividend Yield | Dividend Rating |

| Chongqing Rural Commercial Bank (SEHK:3618) | 7.96% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.90% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.05% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 3.96% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.92% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.13% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 3.96% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.26% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.22% | ★★★★★★ |

| E J Holdings (TSE:2153) | 4.76% | ★★★★★★ |

Click here to see the full list of 1116 stocks from our Top Asian Dividend Stocks screener.

Let's uncover some gems from our specialized screener.

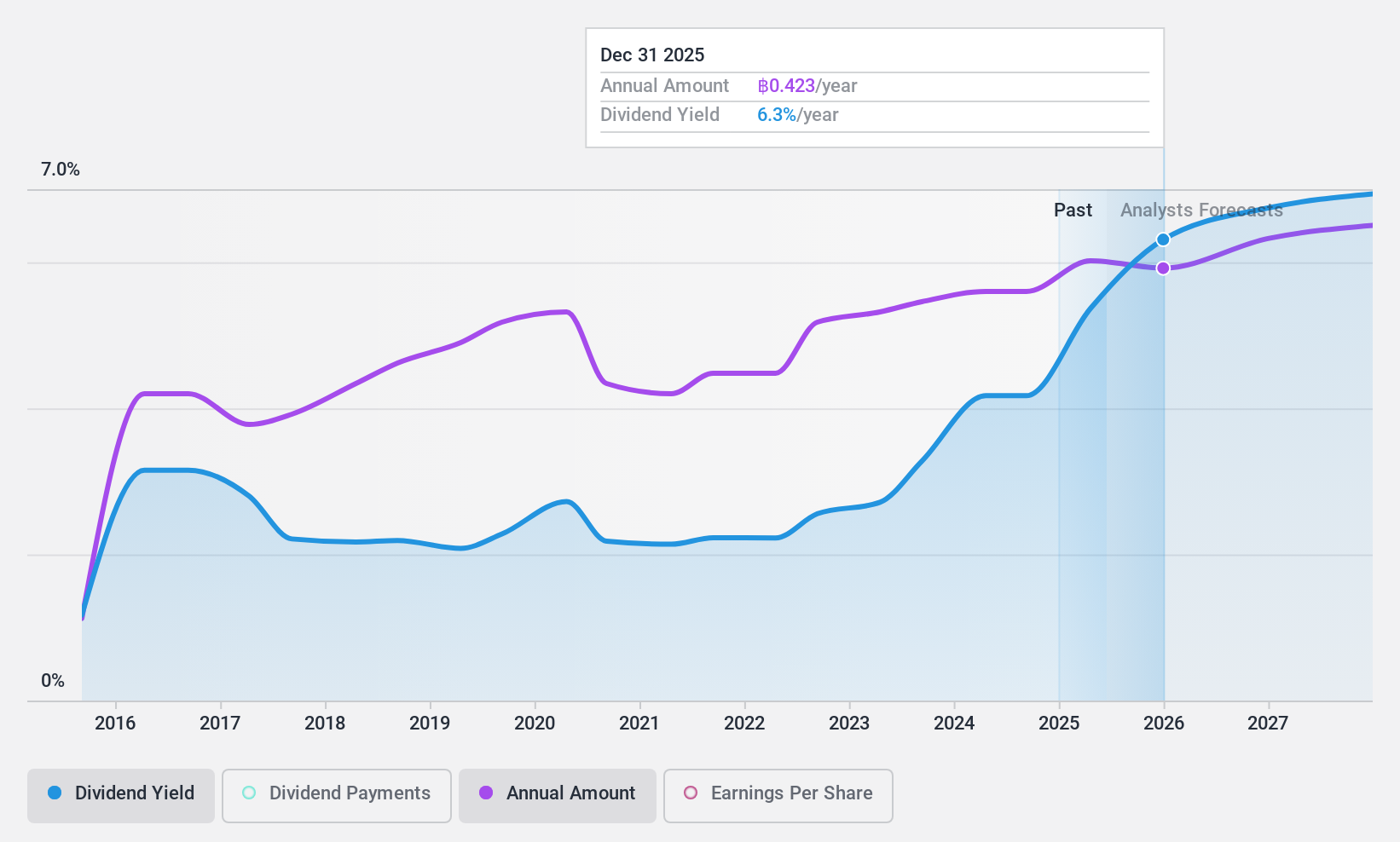

Home Product Center (SET:HMPRO)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Home Product Center Public Company Limited operates as a home improvement retailer in Thailand, Malaysia, and Vietnam with a market cap of THB101.26 billion.

Operations: Home Product Center's revenue from retail building products amounts to THB72.58 billion.

Dividend Yield: 5.1%

Home Product Center's dividend yield of 5.12% is below the top quartile in Thailand, and its dividends have been volatile over the past decade despite some growth. The company recently announced a THB 7 billion share repurchase program to optimize liquidity and improve financial metrics. While dividends are covered by earnings (87%) and cash flows (83.7%), the company's high debt level may impact future stability. A recent dividend increase suggests ongoing commitment to shareholder returns.

- Unlock comprehensive insights into our analysis of Home Product Center stock in this dividend report.

- The analysis detailed in our Home Product Center valuation report hints at an inflated share price compared to its estimated value.

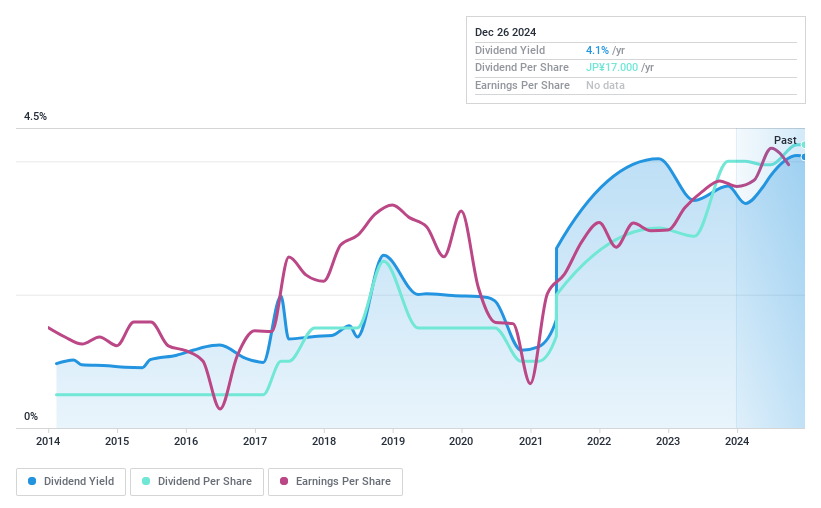

TYK (TSE:5363)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: TYK Corporation manufactures and sells functional refractories and ceramics globally, with a market cap of ¥22.70 billion.

Operations: TYK Corporation's revenue segments include Functional Refractories at ¥18,500 million and Ceramics at ¥6,200 million.

Dividend Yield: 3.3%

TYK's dividend payments are well-supported by a low payout ratio of 13% and a cash payout ratio of 23.4%, indicating strong coverage by earnings and cash flows. Despite earnings growth of 20.7% over the past year, TYK's dividends have been volatile, with an unreliable track record over the last decade. The current dividend yield is lower than the top quartile in Japan, suggesting room for improvement in yield competitiveness despite its trading at a significant discount to fair value estimates.

- Click here to discover the nuances of TYK with our detailed analytical dividend report.

- The valuation report we've compiled suggests that TYK's current price could be quite moderate.

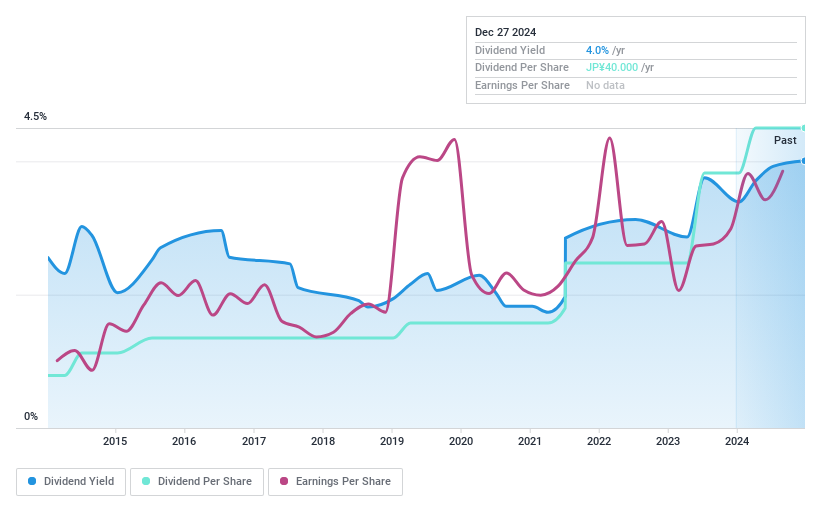

Ohba (TSE:9765)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Ohba Co., Ltd. offers consulting services for city planning projects in Japan and has a market cap of ¥17.32 billion.

Operations: Ohba Co., Ltd.'s revenue primarily comes from its consulting services related to urban development initiatives in Japan.

Dividend Yield: 3.6%

Ohba's dividend payments have been stable and growing over the past decade, though its 3.65% yield is slightly below the top quartile in Japan. Despite a low payout ratio of 42.2%, dividends are not covered by free cash flows, raising sustainability concerns. Recent earnings growth of 29.5% is promising, yet the lack of free cash flow coverage persists as a challenge. The company recently increased its year-end dividend forecast to ¥22 per share from ¥20 per share for May 2025, reflecting confidence in future performance despite current constraints.

- Get an in-depth perspective on Ohba's performance by reading our dividend report here.

- Our expertly prepared valuation report Ohba implies its share price may be too high.

Next Steps

- Take a closer look at our Top Asian Dividend Stocks list of 1116 companies by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Home Product Center might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SET:HMPRO

Home Product Center

Operates as a home improvement retailer in Thailand, Malaysia, and Vietnam.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|5.0% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|63.8% undervalued

OI

Community Contributor