Increases to CEO Compensation Might Be Put On Hold For Now at CSE Global Limited (SGX:544)

Key Insights

- CSE Global will host its Annual General Meeting on 21st of April

- Total pay for CEO Boon Kheng Lim includes S$739.0k salary

- The overall pay is 1,434% above the industry average

- CSE Global's total shareholder return over the past three years was 2.7% while its EPS grew by 8.4% over the past three years

Under the guidance of CEO Boon Kheng Lim, CSE Global Limited (SGX:544) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 21st of April. However, some shareholders may still want to keep CEO compensation within reason.

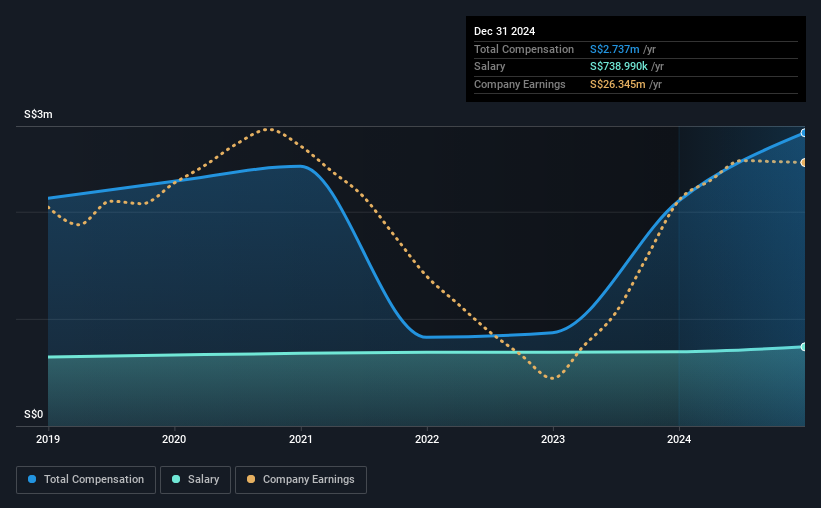

See our latest analysis for CSE Global

Comparing CSE Global Limited's CEO Compensation With The Industry

According to our data, CSE Global Limited has a market capitalization of S$282m, and paid its CEO total annual compensation worth S$2.7m over the year to December 2024. That's a notable increase of 30% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at S$739k.

On examining similar-sized companies in the Singapore IT industry with market capitalizations between S$132m and S$526m, we discovered that the median CEO total compensation of that group was S$178k. Hence, we can conclude that Boon Kheng Lim is remunerated higher than the industry median. What's more, Boon Kheng Lim holds S$10.0m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | S$739k | S$693k | 27% |

| Other | S$2.0m | S$1.4m | 73% |

| Total Compensation | S$2.7m | S$2.1m | 100% |

On an industry level, around 79% of total compensation represents salary and 21% is other remuneration. It's interesting to note that CSE Global allocates a smaller portion of compensation to salary in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

CSE Global Limited's Growth

CSE Global Limited's earnings per share (EPS) grew 8.4% per year over the last three years. In the last year, its revenue is up 19%.

We think the revenue growth is good. And, while modest, the EPS growth is noticeable. So while we'd stop just short of calling this a top performer, but we think it is well worth watching. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has CSE Global Limited Been A Good Investment?

With a total shareholder return of 2.7% over three years, CSE Global Limited has done okay by shareholders, but there's always room for improvement. In light of that, investors might probably want to see an improvement on their returns before they feel generous about increasing the CEO remuneration.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 1 warning sign for CSE Global that investors should be aware of in a dynamic business environment.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:544

CSE Global

An investment holding company, engages in the provision of integrated industrial automation, information technology, and intelligent transport solutions in the Asia Pacific, the Americas, Europe, the Middle East, and Africa.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion