Advertisement

- Singapore

- /

- Office REITs

- /

- SGX:K71U

Earnings Miss: Keppel REIT Missed EPS And Analysts Are Revising Their Forecasts

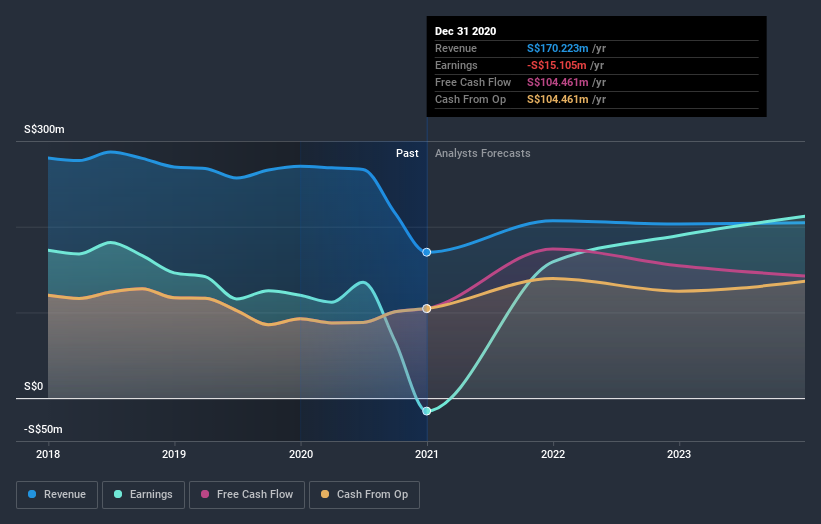

Keppel REIT (SGX:K71U) came out with its yearly results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. Revenues of S$170m beat expectations by 7.6%. Unfortunately statutory earnings per share (EPS) fell well short of the mark, turning in a loss of S$0.0045 compared to previous analyst expectations of a profit. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Keppel REIT after the latest results.

View our latest analysis for Keppel REIT

Taking into account the latest results, the consensus forecast from Keppel REIT's 15 analysts is for revenues of S$206.9m in 2021, which would reflect a substantial 22% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to grow 11% to S$0.044. Yet prior to the latest earnings, the analysts had been anticipated revenues of S$181.7m and earnings per share (EPS) of S$0.043 in 2021. The analysts seem more optimistic after the latest results, with a nice increase in revenue and a modest lift to earnings per share estimates.

Althoughthe analysts have upgraded their earnings estimates, there was no change to the consensus price target of S$1.18, suggesting that the forecast performance does not have a long term impact on the company's valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Keppel REIT analyst has a price target of S$1.45 per share, while the most pessimistic values it at S$0.90. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. One thing stands out from these estimates, which is that Keppel REIT is forecast to grow faster in the future than it has in the past, with revenues expected to grow 22%. If achieved, this would be a much better result than the 3.1% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 9.4% per year. So it looks like Keppel REIT is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Keppel REIT's earnings potential next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Keppel REIT going out to 2023, and you can see them free on our platform here..

However, before you get too enthused, we've discovered 2 warning signs for Keppel REIT that you should be aware of.

When trading Keppel REIT or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Keppel REIT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SGX:K71U

Keppel REIT

Listed by way of an introduction on 28 April 2006, Keppel REIT is one of Asia’s leading real estate investment trusts with a portfolio of prime commercial assets in Asia Pacific’s key business districts.

Solid track record and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor