- Singapore

- /

- Real Estate

- /

- SGX:T24

Tuan Sing Holdings Full Year 2024 Earnings: EPS: S$0.002 (vs S$0.004 in FY 2023)

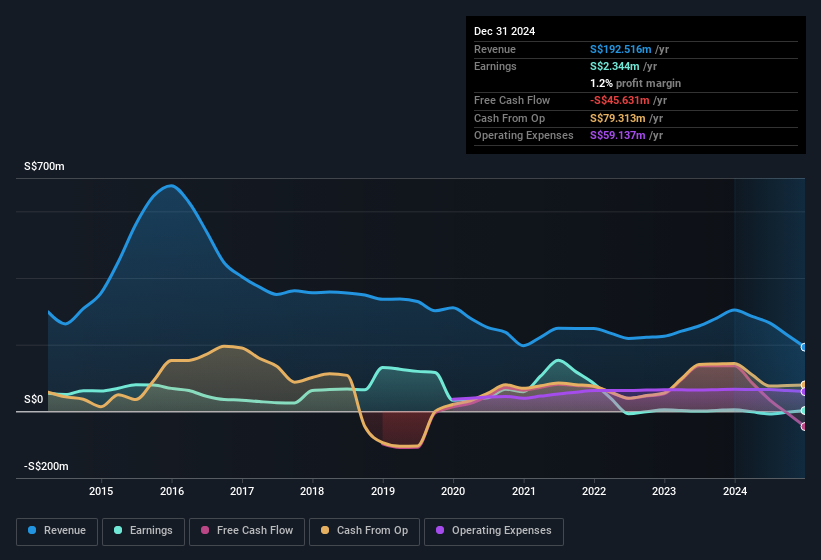

Tuan Sing Holdings (SGX:T24) Full Year 2024 Results

Key Financial Results

- Revenue: S$192.5m (down 37% from FY 2023).

- Net income: S$2.34m (down 52% from FY 2023).

- Profit margin: 1.2% (down from 1.6% in FY 2023).

- EPS: S$0.002 (down from S$0.004 in FY 2023).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Tuan Sing Holdings shares are down 5.1% from a week ago.

Risk Analysis

Before you take the next step you should know about the 3 warning signs for Tuan Sing Holdings (2 make us uncomfortable!) that we have uncovered.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tuan Sing Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:T24

Tuan Sing Holdings

An investment holding company, engages in the real estate investment and development, hospitality, and other businesses in Singapore, Australia, China, Malaysia, and Indonesia.

Average dividend payer with slight risk.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion