Advertisement

As the global markets navigate a mixed start to the new year, with U.S. stocks closing another strong year despite some recent setbacks, investors are seeking opportunities amid fluctuating economic indicators. Penny stocks, though an older term, continue to represent a compelling area for potential growth primarily in smaller or newer companies. When these stocks are supported by robust financial health and sound fundamentals, they can offer significant upside potential while mitigating some of the associated risks.

Top 10 Penny Stocks

| Name | Share Price | Market Cap | Financial Health Rating |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.53 | MYR2.64B | ★★★★★★ |

| Embark Early Education (ASX:EVO) | A$0.775 | A$142.2M | ★★★★☆☆ |

| LaserBond (ASX:LBL) | A$0.565 | A$66.23M | ★★★★★★ |

| Datasonic Group Berhad (KLSE:DSONIC) | MYR0.41 | MYR1.14B | ★★★★★★ |

| Foresight Group Holdings (LSE:FSG) | £3.71 | £425.03M | ★★★★★★ |

| ME Group International (LSE:MEGP) | £2.01 | £757.4M | ★★★★★★ |

| Bosideng International Holdings (SEHK:3998) | HK$3.64 | HK$40.08B | ★★★★★★ |

| Polar Capital Holdings (AIM:POLR) | £4.87 | £469.45M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.966 | £152.38M | ★★★★★★ |

| Secure Trust Bank (LSE:STB) | £3.52 | £67.13M | ★★★★☆☆ |

Click here to see the full list of 5,820 stocks from our Penny Stocks screener.

Let's review some notable picks from our screened stocks.

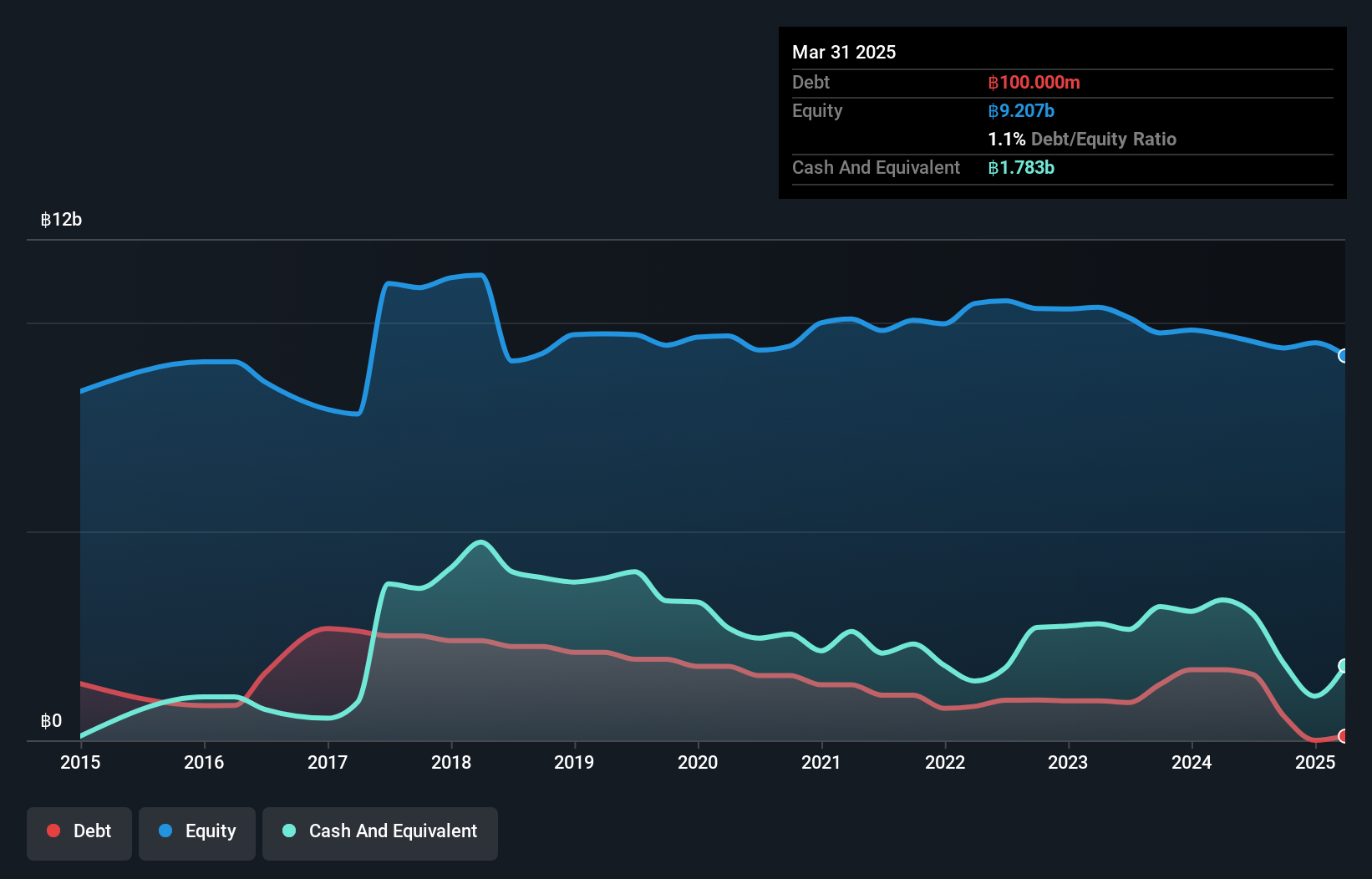

Global Green Chemicals (SET:GGC)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Global Green Chemicals Public Company Limited engages in the production, distribution, and transportation of oleochemical products across Thailand, China, India, Korea, and other international markets with a market capitalization of THB4.44 billion.

Operations: The company generates revenue primarily from Methyl Ester, contributing THB11.83 billion, and Fatty Alcohols, contributing THB5.99 billion.

Market Cap: THB4.44B

Global Green Chemicals faces challenges typical of penny stocks, with negative operating cash flow and unprofitability. Despite this, the company has a strong balance sheet, as its short-term assets exceed both short and long-term liabilities. The debt level is appropriate given it holds more cash than total debt. While trading at a significant discount to estimated fair value, the company's losses have increased annually by 24.7% over five years. Recent earnings show sales growth but continued net losses, highlighting ongoing financial hurdles despite revenue from Methyl Ester and Fatty Alcohols totaling THB17.82 billion for nine months in 2024.

- Unlock comprehensive insights into our analysis of Global Green Chemicals stock in this financial health report.

- Gain insights into Global Green Chemicals' outlook and expected performance with our report on the company's earnings estimates.

MTQ (SGX:M05)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: MTQ Corporation Limited, with a market cap of SGD50.60 million, offers engineering solutions for oilfield equipment across Singapore, the Kingdom of Bahrain, Australia, United Arab Emirates, and the United Kingdom.

Operations: The company generates revenue primarily from its Oilfield Engineering segment, which accounts for SGD77.17 million.

Market Cap: SGD50.6M

MTQ Corporation Limited, with a market cap of SGD50.60 million, primarily generates revenue from its Oilfield Engineering segment. The company recently declared an interim dividend, though its sustainability is questionable due to insufficient free cash flow coverage. Despite stable weekly volatility and no significant shareholder dilution over the past year, MTQ's profit margins have declined from 12.2% to 5.5%. Earnings growth has been negative at -59.3%, contrasting sharply with the industry average growth of 9.8%. However, MTQ maintains a strong balance sheet with short-term assets exceeding liabilities and well-covered debt by operating cash flow and EBIT.

- Dive into the specifics of MTQ here with our thorough balance sheet health report.

- Explore historical data to track MTQ's performance over time in our past results report.

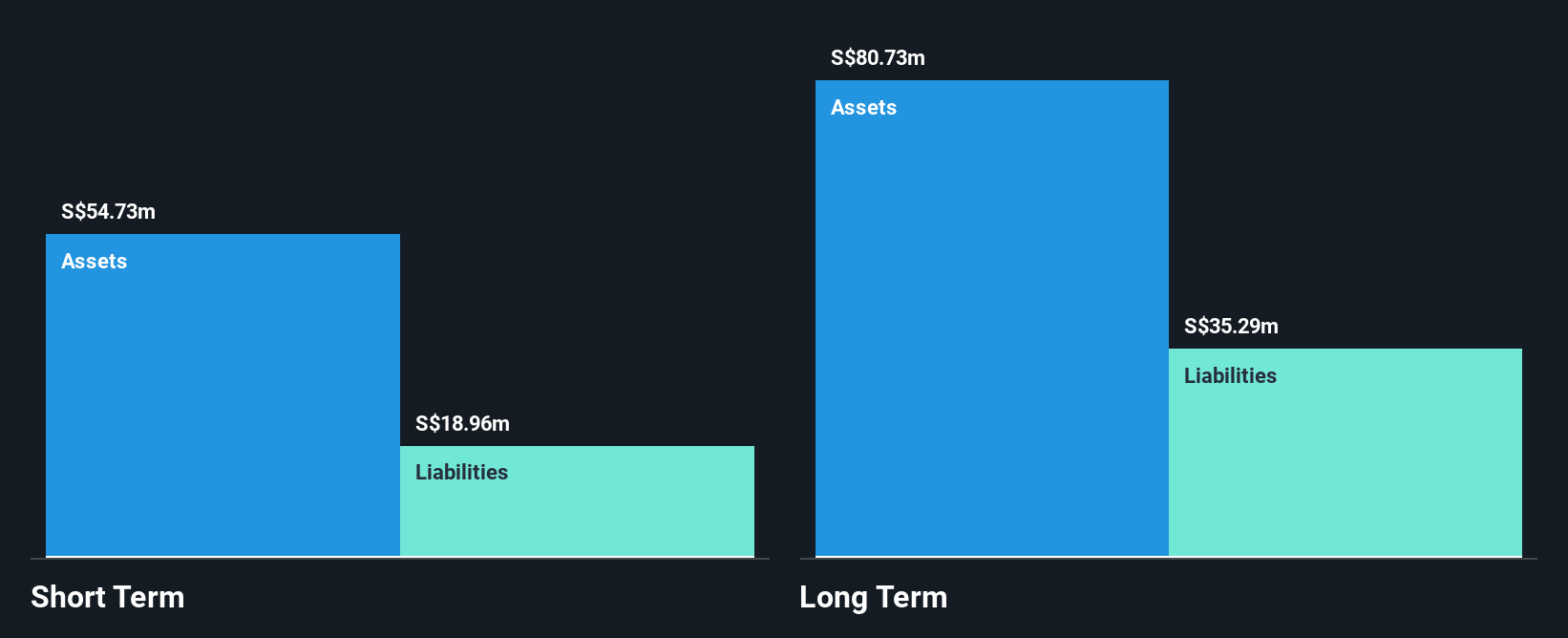

Tat Seng Packaging Group (SGX:T12)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Tat Seng Packaging Group Ltd designs, manufactures, and sells corrugated paper products and other packaging solutions in Singapore and the People's Republic of China, with a market cap of SGD126.55 million.

Operations: The company generates SGD259.78 million in revenue from its Packaging & Containers segment.

Market Cap: SGD126.55M

Tat Seng Packaging Group Ltd, with a market cap of SGD126.55 million, has demonstrated steady financial health and growth potential. The company reported revenue of SGD259.78 million from its Packaging & Containers segment and has seen earnings grow by 13% over the past year, surpassing its five-year average growth rate of 3.4%. Tat Seng's short-term assets significantly exceed both short-term and long-term liabilities, indicating strong liquidity management. The company's debt is well-covered by operating cash flow, and it holds more cash than total debt. Despite an experienced board, the Return on Equity remains low at 10.4%, while dividends have shown instability in sustainability.

- Get an in-depth perspective on Tat Seng Packaging Group's performance by reading our balance sheet health report here.

- Examine Tat Seng Packaging Group's past performance report to understand how it has performed in prior years.

Summing It All Up

- Unlock more gems! Our Penny Stocks screener has unearthed 5,817 more companies for you to explore.Click here to unveil our expertly curated list of 5,820 Penny Stocks.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SET:GGC

Global Green Chemicals

Engages in the production, distribution, and transportation of oleochemicals products in Thailand, the People’s Republic of China, India, Korea, and internationally.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor