Advertisement

- Singapore

- /

- Professional Services

- /

- SGX:TCU

Credit Bureau Asia's (SGX:TCU) Upcoming Dividend Will Be Larger Than Last Year's

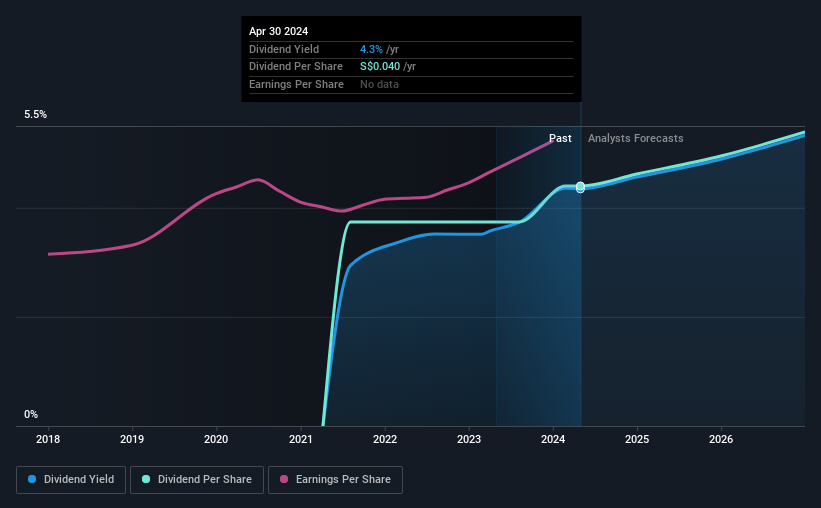

Credit Bureau Asia Limited (SGX:TCU) has announced that it will be increasing its dividend from last year's comparable payment on the 24th of May to SGD0.02. Based on this payment, the dividend yield for the company will be 4.3%, which is fairly typical for the industry.

Check out our latest analysis for Credit Bureau Asia

Credit Bureau Asia's Dividend Is Well Covered By Earnings

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Before this announcement, Credit Bureau Asia was paying out 87% of earnings, but a comparatively small 37% of free cash flows. This leaves plenty of cash for reinvestment into the business.

Over the next year, EPS is forecast to expand by 28.8%. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 66% which brings it into quite a comfortable range.

Credit Bureau Asia Is Still Building Its Track Record

Looking back, the dividend has been stable, but the company hasn't been paying a dividend for very long so we can't be confident that the dividend will remain stable through all economic environments. The annual payment during the last 3 years was SGD0.034 in 2021, and the most recent fiscal year payment was SGD0.04. This works out to be a compound annual growth rate (CAGR) of approximately 5.6% a year over that time. Investors will likely want to see a longer track record of growth before making decision to add this to their income portfolio.

Credit Bureau Asia Could Grow Its Dividend

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. We are encouraged to see that Credit Bureau Asia has grown earnings per share at 9.5% per year over the past five years. Past earnings growth has been decent, but unless this is one of those rare businesses that can grow without additional capital investment or marketing spend, we'd generally expect the higher payout ratio to limit its future growth prospects.

Our Thoughts On Credit Bureau Asia's Dividend

In summary, while it's always good to see the dividend being raised, we don't think Credit Bureau Asia's payments are rock solid. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We don't think Credit Bureau Asia is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 1 warning sign for Credit Bureau Asia that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:TCU

Credit Bureau Asia

An investment holding company, provides credit and risk information solutions in Singapore, Malaysia, Cambodia, and Myanmar.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor