- Singapore

- /

- Trade Distributors

- /

- SGX:P52

Is Pan-United Corporation Ltd's (SGX:P52) Recent Stock Performance Influenced By Its Fundamentals In Any Way?

Pan-United (SGX:P52) has had a great run on the share market with its stock up by a significant 23% over the last three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. Particularly, we will be paying attention to Pan-United's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Pan-United

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Pan-United is:

8.8% = S$19m ÷ S$213m (Based on the trailing twelve months to December 2021).

The 'return' is the yearly profit. So, this means that for every SGD1 of its shareholder's investments, the company generates a profit of SGD0.09.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

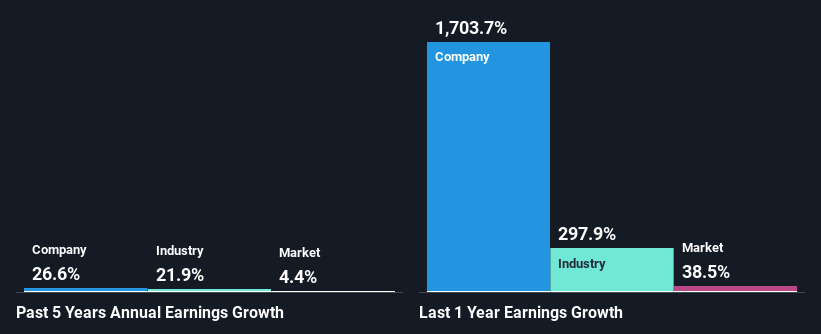

Pan-United's Earnings Growth And 8.8% ROE

At first glance, Pan-United's ROE doesn't look very promising. However, the fact that the its ROE is quite higher to the industry average of 6.7% doesn't go unnoticed by us. Particularly, the substantial 27% net income growth seen by Pan-United over the past five years is impressive . That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. Therefore, the growth in earnings could also be the result of other factors. Such as- high earnings retention or the company belonging to a high growth industry.

We then compared Pan-United's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 22% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is Pan-United fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Pan-United Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 66% (implying that it keeps only 34% of profits) for Pan-United suggests that the company's growth wasn't really hampered despite it returning most of the earnings to its shareholders.

Additionally, Pan-United has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders.

Conclusion

Overall, we feel that Pan-United certainly does have some positive factors to consider. Specifically, its respectable ROE which likely led to the considerable growth in earnings. Yet, the company is retaining a small portion of its profits. Which means that the company has been able to grow its earnings in spite of it, so that's not too bad. That being so, a study of the latest analyst forecasts show that the company is expected to see a slowdown in its future earnings growth. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you're looking to trade Pan-United, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:P52

Pan-United

An investment holding company, engages in the concrete and logistics businesses in Singapore and internationally.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives