Fu Yu Corporation Limited (SGX:F13): Commentary On Fundamentals

I've been keeping an eye on Fu Yu Corporation Limited (SGX:F13) because I'm attracted to its fundamentals. Looking at the company as a whole, as a potential stock investment, I believe F13 has a lot to offer. Basically, it is a company with great financial health as well as a an impressive track record of performance. Below is a brief commentary on these key aspects. If you're interested in understanding beyond my broad commentary, take a look at the report on Fu Yu here.

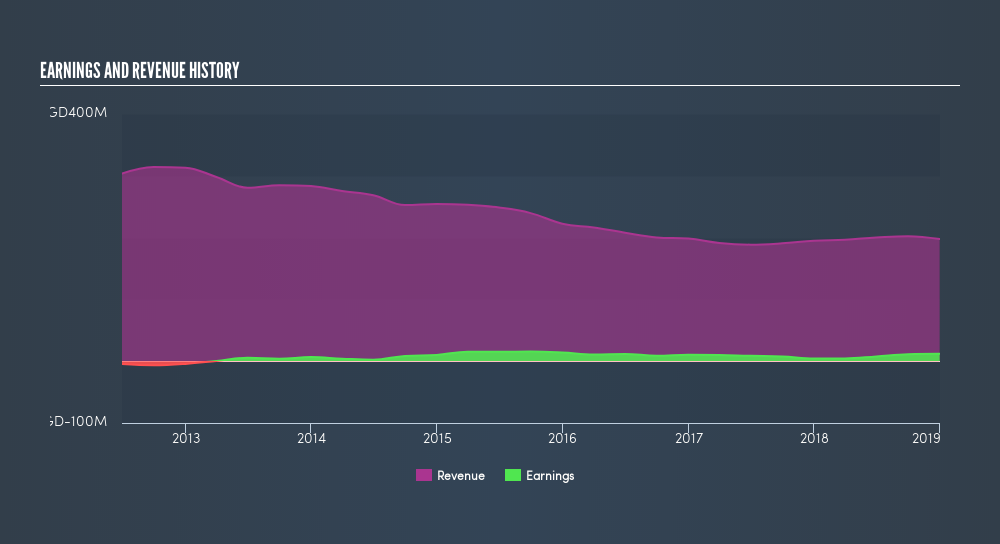

Flawless balance sheet with proven track record

F13 delivered a triple-digit bottom-line expansion over the past couple of years, with its most recent earnings level surpassing its average level over the last five years. Not only did F13 outperformed its past performance, its growth also surpassed the Machinery industry expansion, which generated a 23% earnings growth. This paints a buoyant picture for the company. F13's strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This implies that F13 manages its cash and cost levels well, which is an important determinant of the company’s health. Investors should not worry about F13’s debt levels because the company has none! It has only utilized funding from its equity capital to run the business, which is typically normal for a small-cap company. F13 has plenty of financial flexibility, without debt obligations to meet in the short term, as well as the headroom to raise debt should it need to in the future.

Next Steps:

For Fu Yu, I've compiled three relevant factors you should further research:

- Future Outlook: What are well-informed industry analysts predicting for F13’s future growth? Take a look at our free research report of analyst consensus for F13’s outlook.

- Valuation: What is F13 worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether F13 is currently mispriced by the market.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of F13? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SGX:F13

Fu Yu

An investment holding company, engages in the manufacture and sub-assembly of precision plastic parts and components in Singapore, Malaysia, and China.

Flawless balance sheet and slightly overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion