Advertisement

- Singapore

- /

- Electrical

- /

- SGX:500

Increases to CEO Compensation Might Be Put On Hold For Now at Tai Sin Electric Limited (SGX:500)

Key Insights

- Tai Sin Electric to hold its Annual General Meeting on 25th of October

- Salary of S$494.0k is part of CEO Bernard Lim's total remuneration

- The total compensation is 679% higher than the average for the industry

- Tai Sin Electric's EPS grew by 19% over the past three years while total shareholder return over the past three years was 52%

Performance at Tai Sin Electric Limited (SGX:500) has been reasonably good and CEO Bernard Lim has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 25th of October. However, some shareholders will still be cautious of paying the CEO excessively.

Check out our latest analysis for Tai Sin Electric

Comparing Tai Sin Electric Limited's CEO Compensation With The Industry

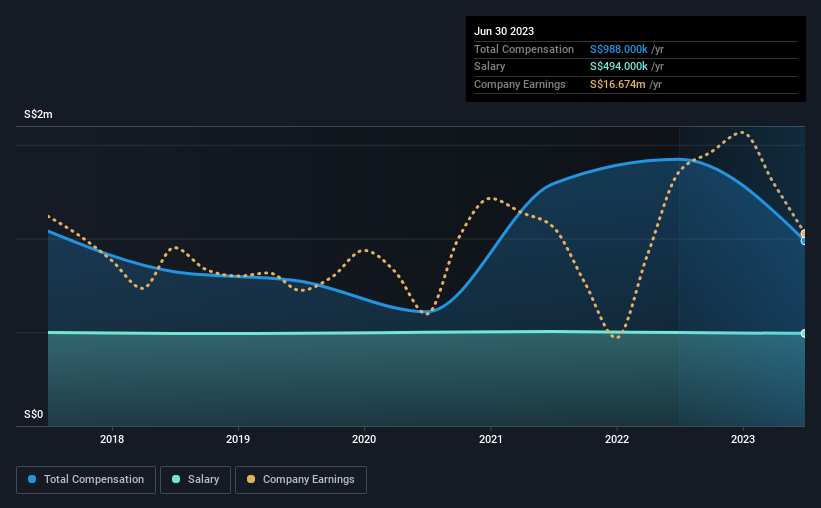

Our data indicates that Tai Sin Electric Limited has a market capitalization of S$184m, and total annual CEO compensation was reported as S$988k for the year to June 2023. Notably, that's a decrease of 31% over the year before. Notably, the salary which is S$494.0k, represents most of the total compensation being paid.

In comparison with other companies in the Singapore Electrical industry with market capitalizations under S$274m, the reported median total CEO compensation was S$127k. Hence, we can conclude that Bernard Lim is remunerated higher than the industry median. What's more, Bernard Lim holds S$50m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | S$494k | S$498k | 50% |

| Other | S$494k | S$925k | 50% |

| Total Compensation | S$988k | S$1.4m | 100% |

On an industry level, roughly 83% of total compensation represents salary and 17% is other remuneration. Tai Sin Electric sets aside a smaller share of compensation for salary, in comparison to the overall industry.

Tai Sin Electric Limited's Growth

Tai Sin Electric Limited has seen its earnings per share (EPS) increase by 19% a year over the past three years. Its revenue is up 11% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Tai Sin Electric Limited Been A Good Investment?

Most shareholders would probably be pleased with Tai Sin Electric Limited for providing a total return of 52% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 2 warning signs for Tai Sin Electric that investors should think about before committing capital to this stock.

Important note: Tai Sin Electric is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Tai Sin Electric might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:500

Tai Sin Electric

Manufactures and deals in cable and wire products in Singapore, Malaysia, Brunei, Vietnam, Indonesia, Myanmar, Cambodia, Thailand, and internationally.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor