Advertisement

Oversea-Chinese Banking's (SGX:O39) Shareholders Will Receive A Bigger Dividend Than Last Year

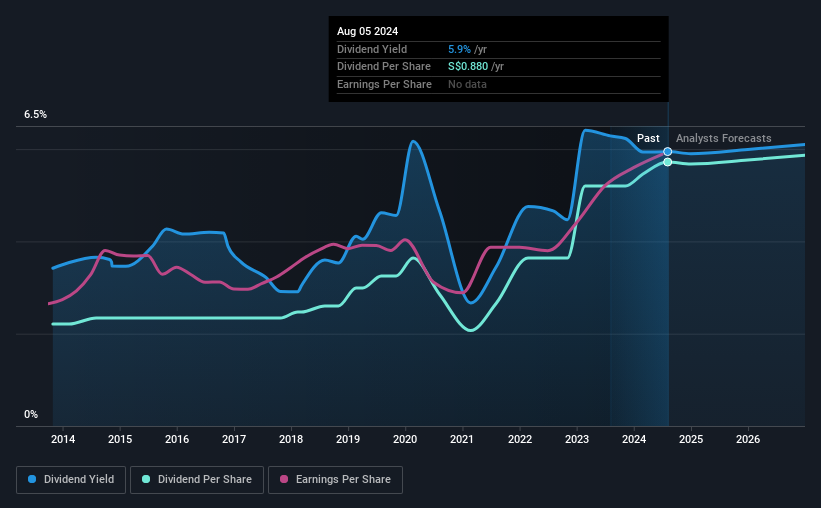

Oversea-Chinese Banking Corporation Limited (SGX:O39) has announced that it will be increasing its dividend from last year's comparable payment on the 23rd of August to SGD0.44. This takes the dividend yield to 5.9%, which shareholders will be pleased with.

View our latest analysis for Oversea-Chinese Banking

Oversea-Chinese Banking's Dividend Forecasted To Be Well Covered By Earnings

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained.

Having distributed dividends for at least 10 years, Oversea-Chinese Banking has a long history of paying out a part of its earnings to shareholders. Based on Oversea-Chinese Banking's last earnings report, the payout ratio is at a decent 53%, meaning that the company is able to pay out its dividend with a bit of room to spare.

Over the next 3 years, EPS is forecast to expand by 3.4%. The future payout ratio could be 54% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. The dividend has gone from an annual total of SGD0.34 in 2014 to the most recent total annual payment of SGD0.88. This means that it has been growing its distributions at 10.0% per annum over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

We Could See Oversea-Chinese Banking's Dividend Growing

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. We are encouraged to see that Oversea-Chinese Banking has grown earnings per share at 8.6% per year over the past five years. Since earnings per share is growing at an acceptable rate, and the payout policy is balanced, we think the company is positioning itself well to grow earnings and dividends in the future.

Oversea-Chinese Banking Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All in all, this checks a lot of the boxes we look for when choosing an income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 1 warning sign for Oversea-Chinese Banking that investors should take into consideration. Is Oversea-Chinese Banking not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:O39

Oversea-Chinese Banking

Provides financial services in Singapore, Malaysia, Indonesia, Greater China, rest of the Asia Pacific, and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor