Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Tele2 AB (publ) (STO:TEL2 B) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Tele2

What Is Tele2's Debt?

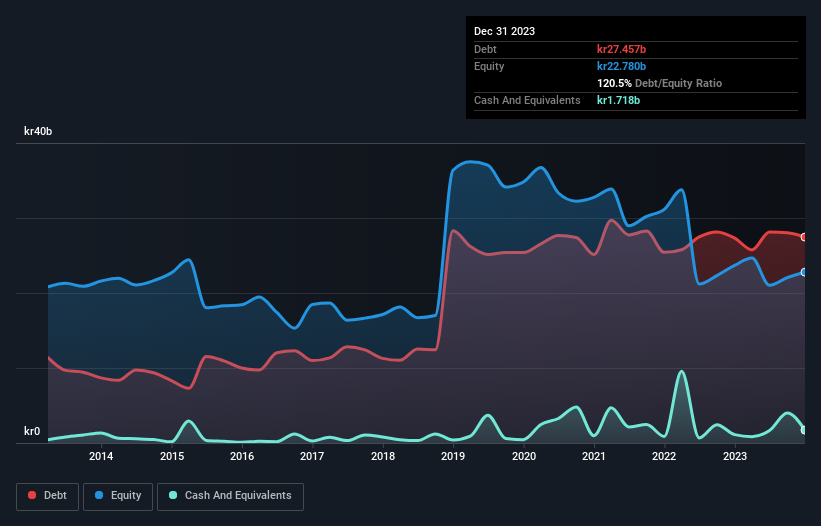

As you can see below, Tele2 had kr27.5b of debt, at December 2023, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of kr1.72b, its net debt is less, at about kr25.7b.

A Look At Tele2's Liabilities

Zooming in on the latest balance sheet data, we can see that Tele2 had liabilities of kr12.9b due within 12 months and liabilities of kr30.4b due beyond that. Offsetting this, it had kr1.72b in cash and kr5.77b in receivables that were due within 12 months. So it has liabilities totalling kr35.8b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of kr57.9b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Tele2's net debt is sitting at a very reasonable 2.4 times its EBITDA, while its EBIT covered its interest expense just 5.9 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. One way Tele2 could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 10%, as it did over the last year. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Tele2's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Tele2 actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

On our analysis Tele2's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. But the other factors we noted above weren't so encouraging. For instance it seems like it has to struggle a bit to handle its total liabilities. Considering this range of data points, we think Tele2 is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Tele2 is showing 3 warning signs in our investment analysis , you should know about...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Tele2 might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:TEL2 B

Tele2

Provides fixed and mobile connectivity, handset related data services, and entertainment services in Sweden, Lithuania, Latvia, and Estonia.

Proven track record average dividend payer.

Similar Companies

Market Insights

Community Narratives