- Sweden

- /

- Electronic Equipment and Components

- /

- OM:PRIC B

Results: Pricer AB (publ) Beat Earnings Expectations And Analysts Now Have New Forecasts

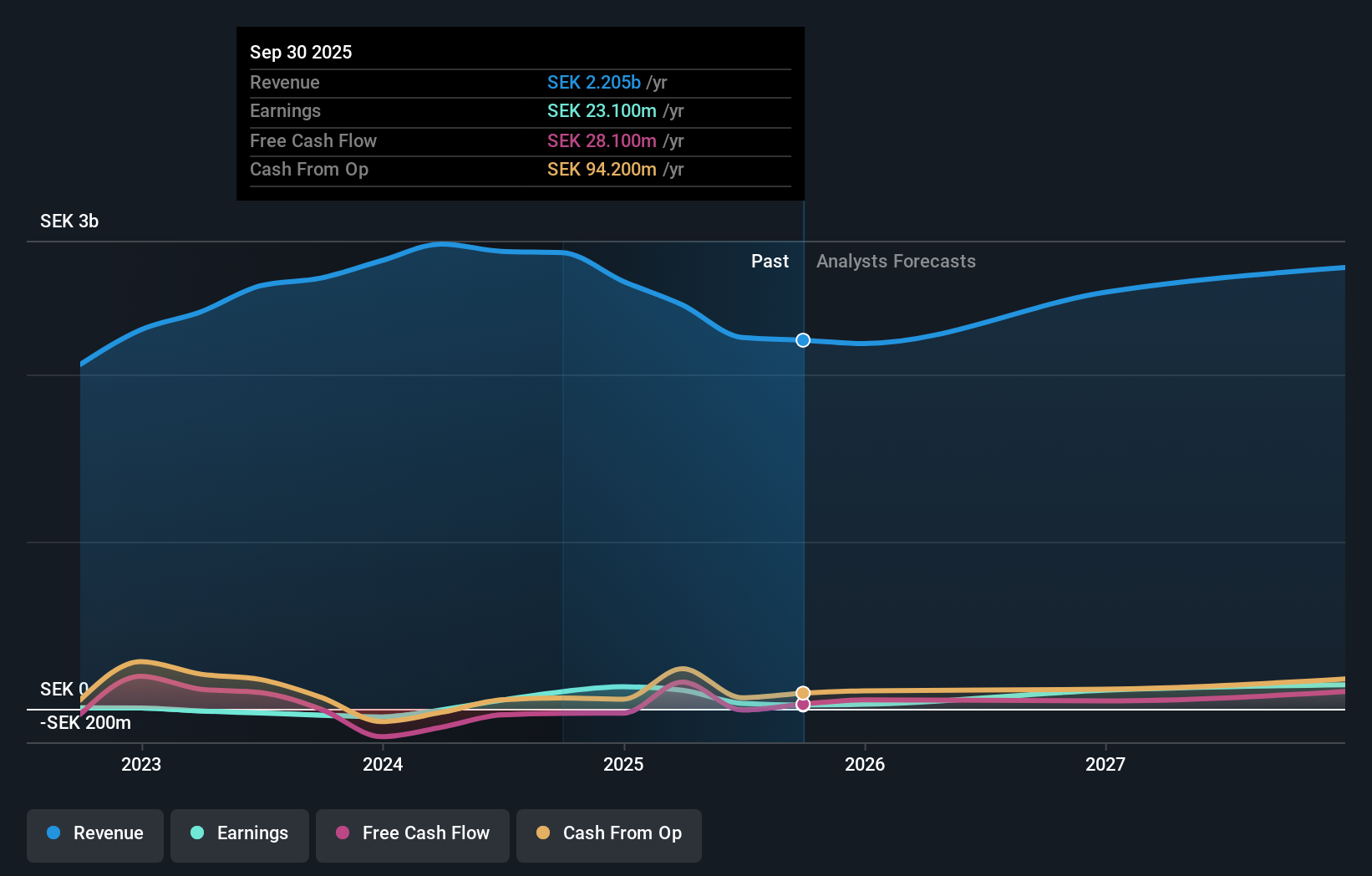

Pricer AB (publ) (STO:PRIC B) defied analyst predictions to release its quarterly results, which were ahead of market expectations. Pricer beat earnings, with revenues hitting kr598m, ahead of expectations, and statutory earnings per share outperforming analyst reckonings by a solid 11%. This is an important time for investors, as they can track a company's performance in its report, look at what expert is forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimate to see what could be in store for next year.

Following the latest results, Pricer's sole analyst are now forecasting revenues of kr2.49b in 2026. This would be a solid 13% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to bounce 441% to kr0.76. In the lead-up to this report, the analyst had been modelling revenues of kr2.58b and earnings per share (EPS) of kr1.12 in 2026. The analyst seem less optimistic after the recent results, reducing their revenue forecasts and making a large cut to earnings per share numbers.

View our latest analysis for Pricer

The consensus price target fell 18% to kr7.73, with the weaker earnings outlook clearly leading valuation estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Pricer's past performance and to peers in the same industry. We can infer from the latest estimates that forecasts expect a continuation of Pricer'shistorical trends, as the 10% annualised revenue growth to the end of 2026 is roughly in line with the 8.7% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 6.6% annually. So although Pricer is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analyst downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. They also downgraded Pricer's revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. The consensus price target fell measurably, with the analyst seemingly not reassured by the latest results, leading to a lower estimate of Pricer's future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Pricer going out as far as 2027, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 2 warning signs for Pricer that you should be aware of.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:PRIC B

Pricer

Provides in-store digital solutions in Europe, the Middle East and Africa, the Americas, and Asia and Pacific.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion