Advertisement

Can Truecaller's (OM:TRUE B) Shift to Subscriptions Offset Weaker Ad Revenue Over Time?

Reviewed by Sasha Jovanovic

- Truecaller AB (publ) recently announced its third quarter 2025 results, reporting sales of SEK 476.62 million and net income of SEK 108.51 million, reflecting higher overall revenue but lower profitability compared to the previous year.

- A unique highlight was the strong 55% increase in subscription revenues and 39% growth in Truecaller for Business revenue, which helped counter a 1% fall in ad income amid regulatory and economic pressures.

- We'll examine how the surge in subscription and business revenues shapes Truecaller’s long-term investment appeal through growing recurring income streams.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Truecaller Investment Narrative Recap

For Truecaller, the big picture hinges on whether you believe in the company’s ability to transition from ad-driven growth to building sustainable recurring income through subscriptions and B2B services, especially outside its core Indian market. The latest results reinforce this narrative, with subscription and business revenue gains buffering ad softness, though the near-term catalyst of driving higher-margin recurring revenue appears intact. The company’s ongoing exposure to foreign exchange volatility against the Swedish krona remains the most unresolved risk for reported financials right now, and this quarter’s news does not materially shift that concern.

The recent launch of the Verified Business (VB) platform, announced in mid-October, stands out in the context of these results. This offering promises added value for enterprise customers and supports the surge in B2B revenue, directly aligning with Truecaller’s focus on deepening recurring, less cyclical income sources, for now, this is a key offset to the pressures on traditional ad revenues.

However, in contrast, investors should be aware that growing concentration of revenue in high-tax markets like India could pressure profit margins over time...

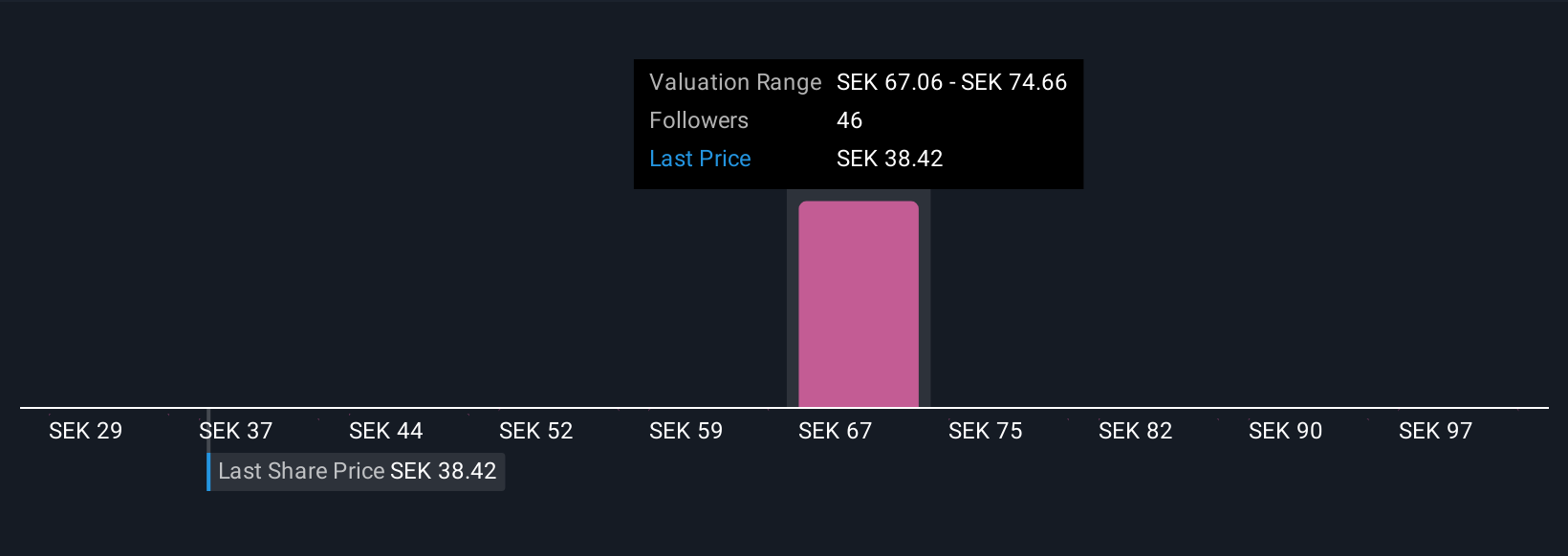

Read the full narrative on Truecaller (it's free!)

Truecaller's outlook predicts SEK 3.5 billion in revenue and SEK 1.1 billion in earnings by 2028. This scenario assumes annual revenue growth of 20.2% and an increase in earnings by SEK 612 million from the current SEK 488 million.

Uncover how Truecaller's forecasts yield a SEK64.00 fair value, a 126% upside to its current price.

Exploring Other Perspectives

Ten individual fair value estimates from the Simply Wall St Community range from SEK52.81 up to SEK105.06, with strong opinions on both ends. As many users look for recurring revenue growth, keep in mind how shifting revenue streams and regional tax rates can matter for your view.

Explore 10 other fair value estimates on Truecaller - why the stock might be worth just SEK52.81!

Build Your Own Truecaller Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Truecaller research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Truecaller research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Truecaller's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Truecaller might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:TRUE B

Truecaller

Develops and publishes mobile caller ID applications for individuals and business in India, the Middle East, Africa, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative