Analysts Are Updating Their Lime Technologies AB (publ) (STO:LIME) Estimates After Its First-Quarter Results

As you might know, Lime Technologies AB (publ) (STO:LIME) last week released its latest quarterly, and things did not turn out so great for shareholders. Lime Technologies missed analyst forecasts, with revenues of kr169m and statutory earnings per share (EPS) of kr1.75, falling short by 3.0% and 4.9% respectively. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

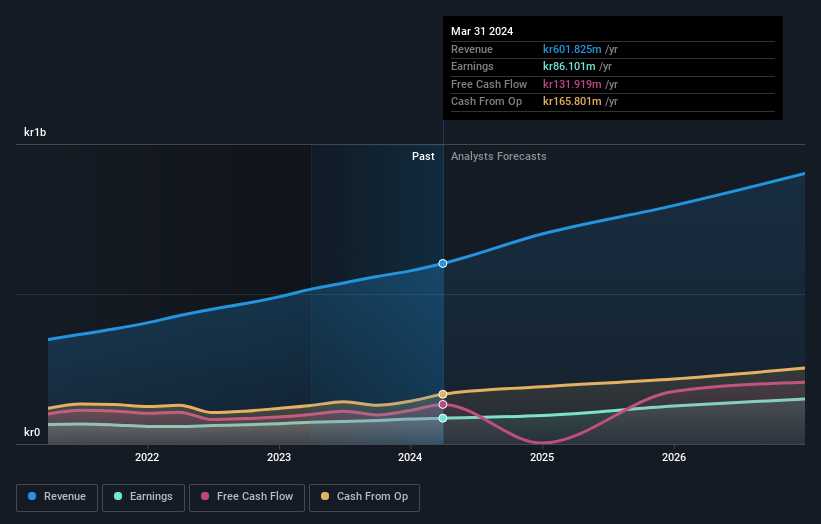

See our latest analysis for Lime Technologies

Taking into account the latest results, the consensus forecast from Lime Technologies' twin analysts is for revenues of kr699.9m in 2024. This reflects a solid 16% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to climb 10% to kr7.16. Before this earnings report, the analysts had been forecasting revenues of kr704.3m and earnings per share (EPS) of kr8.02 in 2024. So there's definitely been a decline in sentiment after the latest results, noting the real cut to new EPS forecasts.

The consensus price target held steady at kr341, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Lime Technologies' past performance and to peers in the same industry. It's clear from the latest estimates that Lime Technologies' rate of growth is expected to accelerate meaningfully, with the forecast 22% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 17% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 15% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Lime Technologies to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at kr341, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Lime Technologies. Long-term earnings power is much more important than next year's profits. We have analyst estimates for Lime Technologies going out as far as 2026, and you can see them free on our platform here.

Even so, be aware that Lime Technologies is showing 1 warning sign in our investment analysis , you should know about...

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:LIME

Lime Technologies

Provides software as a service (SaaS) based customer relationship management (CRM) solutions in the Nordic region.

Outstanding track record with high growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)