In a week marked by cautious Federal Reserve commentary and political uncertainty, global markets have experienced notable volatility. Despite these challenges, the search for promising investment opportunities continues, with growth companies boasting high insider ownership often drawing attention due to their potential alignment of interests between management and shareholders. In this context, identifying stocks with substantial insider ownership can be particularly appealing as it may suggest confidence from those closest to the company's operations and long-term strategy.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Propel Holdings (TSX:PRL) | 23.9% | 37.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.4% |

| Pharma Mar (BME:PHM) | 11.8% | 56.2% |

| CD Projekt (WSE:CDR) | 29.7% | 27% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.4% | 66.3% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 111.4% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's dive into some prime choices out of the screener.

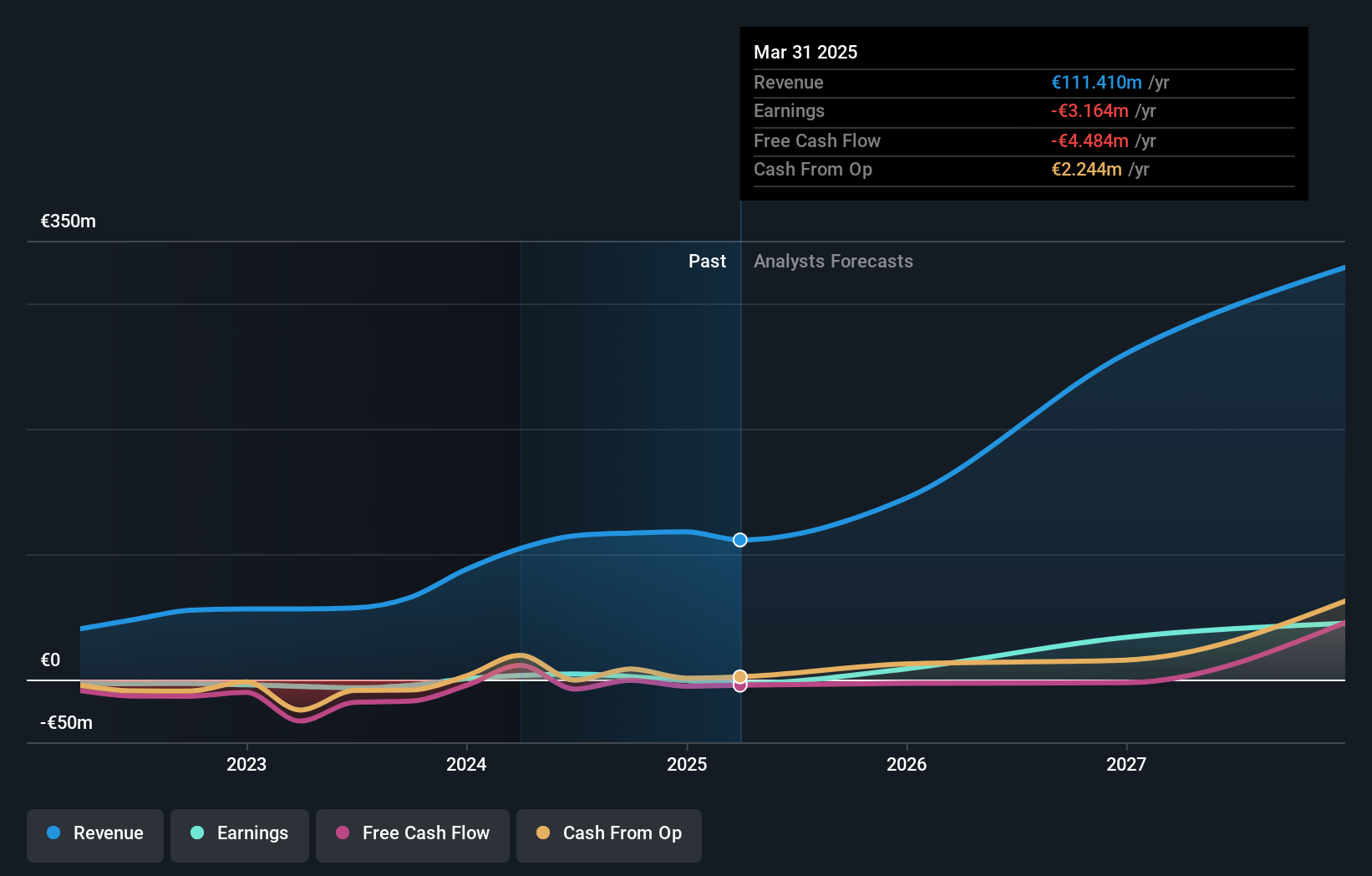

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★★

Overview: Envipco Holding N.V. is engaged in the design, development, manufacture, assembly, marketing, sale, leasing, and servicing of reverse vending machines for collecting and processing used beverage containers across the Netherlands, North America, and Europe with a market cap of €320.18 million.

Operations: Envipco Holding generates revenue through the design, development, manufacture, assembly, marketing, sale, leasing, and servicing of reverse vending machines for the collection and processing of used beverage containers in regions including the Netherlands, North America, and Europe.

Insider Ownership: 36.7%

Envipco Holding is positioned for significant growth, with earnings projected to increase by 105% annually, outpacing the Dutch market. Despite recent profitability challenges and shareholder dilution, the company trades at a substantial discount to its estimated fair value. Recent sales growth and strategic orders in Romania highlight operational momentum. The appointment of Patrick Gierman as CFO may enhance financial leadership. However, no notable insider trading activity has been reported recently.

- Navigate through the intricacies of Envipco Holding with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report Envipco Holding implies its share price may be too high.

Lime Technologies (OM:LIME)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Lime Technologies AB (publ) offers SaaS-based CRM solutions in the Nordic region and has a market cap of SEK4.72 billion.

Operations: The company's revenue primarily comes from selling and implementing CRM systems, amounting to SEK656.49 million.

Insider Ownership: 10.7%

Lime Technologies is experiencing solid growth, with earnings projected to rise significantly at 23.6% annually, surpassing the Swedish market. Despite a high debt level, it trades slightly below its estimated fair value and boasts a strong forecasted return on equity of 35.3%. Recent financial results show increased sales and revenue for Q3 2024 compared to the previous year. The newly appointed nomination committee includes substantial insider ownership representation.

- Get an in-depth perspective on Lime Technologies' performance by reading our analyst estimates report here.

- In light of our recent valuation report, it seems possible that Lime Technologies is trading beyond its estimated value.

Ficont Industry (Beijing) (SHSE:605305)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Ficont Industry (Beijing) Co., Ltd. manufactures and supplies wind turbine tower internals and safety systems for wind turbine manufacturers in China and internationally, with a market cap of CN¥5.81 billion.

Operations: The company's revenue is primarily derived from its Construction Machinery & Equipment segment, totaling CN¥1.34 billion.

Insider Ownership: 27.9%

Ficont Industry (Beijing) has demonstrated strong growth, with earnings rising by 130.5% over the past year and revenue reaching CNY 934.08 million for the nine months ended September 2024. The company trades at a substantial discount to its estimated fair value and is expected to grow revenue faster than the Chinese market at 24.8% annually, although its return on equity is forecasted to be modest at 16.5%.

- Click here to discover the nuances of Ficont Industry (Beijing) with our detailed analytical future growth report.

- Our valuation report here indicates Ficont Industry (Beijing) may be undervalued.

Turning Ideas Into Actions

- Navigate through the entire inventory of 1514 Fast Growing Companies With High Insider Ownership here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:LIME

Lime Technologies

Provides software as a service (SaaS) based customer relationship management (CRM) solutions in the Nordic region.

High growth potential with acceptable track record.

Similar Companies

Market Insights

Community Narratives